Deconstructing the Baseline: What It Truly Means to Earn 75K Across the Provinces

To grasp the true weight of this percentage, we must first dissect what qualifies as total income under the microscope of Statistics Canada. We are far from dealing with a monolithic workforce; instead, this figure captures every individual who files a T1 tax return, ranging from part-time retail staff in Halifax to corporate lawyers in downtown Toronto. When you aggregate wages, salaries, investment returns, and self-employment earnings, the median individual income nationwide actually hovers much lower, around $44,000. Why does this matter? Because it proves that clearing $75,000 places a worker significantly ahead of the average citizen, yet the everyday lived experience of these earners tells a radically different story.

The Disconnection Between Statistical Wealth and Urban Reality

People don't think about this enough: a seventy-five-thousand-dollar salary in Calgary, Alberta delivers an entirely different life than the exact same paystub in Vancouver, British Columbia. Take a hypothetical software developer landing their first major contract in mid-2025; after federal and provincial payroll deductions take their hefty bite, that gross sum shrinks into a net monthly take-home pay of roughly $4,600. If that worker is trying to rent a one-bedroom apartment in Toronto—where market averages persistently threaten to consume over half of that net amount—the luxury of saving for a down payment vanishes. The issue remains that national averages flatten these regional crises into a deceptively smooth landscape.

How Post-Pandemic Inflation Distorted the Threshold

But let us look at the timeline. If we glance back a few years, hitting this specific metric meant you could comfortably secure a mortgage on a suburban semi-detached home in Southwestern Ontario. Today, after consecutive years of aggressive interest rate hikes by the Bank of Canada and structural supply deficits, that reality has cracked. Honestly, it's unclear whether an individual earning within this bracket can even qualify for a basic condominium loan anymore without a massive, intergenerational wealth transfer acting as a cushion. That changes everything, twisting a historically respectable salary into a stressful exercise in monthly budgeting.

The Structural Anatomy of High Earners in the Canadian Labor Market

Where it gets tricky is analyzing who actually occupies this upper-quarter demographic of the population. The distribution is heavily skewed by industry, age, and systemic systemic advantages that favor specific geographic hubs over others. According to exhaustive tax filer data tracking distributions into 2026, the concentration of individuals crossing the $75,000 threshold is heavily weighted toward professionals within the public utility sectors, natural resource extraction, and specialized technology fields. Yet, the vast swathes of the service-driven economy remain trapped in a compensation structure that rarely breaches the sixty-thousand-dollar ceiling.

The Demographic Divide: Age and Experience as Income Gatekeepers

Age plays an uncompromising role here. It is exceedingly rare for a worker under the age of 25 to see this kind of money, except perhaps those pulling grueling shifts on oil rigs in northern Alberta or specialized software engineers bypassing traditional corporate ladders. The bulk of the 26.8% cohort consists of Canadians aged 35 to 54, individuals who have accumulated at least a decade of institutional equity and corporate leverage. And this is precisely where conventional wisdom stumbles: we assume hard work guarantees upward mobility, but structural stagnation across multiple legacy sectors means younger generations are working longer hours for shares of wealth that are objectively shrinking relative to GDP.

Industry Silos and the Commodity Premium

Consider the stark divergence between manufacturing hubs in Quebec and the resource-dependent economies of the West. A heavy equipment operator in Fort McMurray can easily bypass the $75,000 mark by Q2 of any given fiscal year, whereas a highly educated administrative manager in Montreal might labor for years before getting anywhere near it. This geographic and sectoral volatility means that Canada’s high-earning bracket isn't just an elite club of executives—it is heavily populated by blue-collar tradespeople working in demanding, cyclical industries. As a result: when global commodity markets fluctuate, the percentage of Canadians occupying this income bracket shifts in lockstep, proving how fragile our economic prosperity truly is.

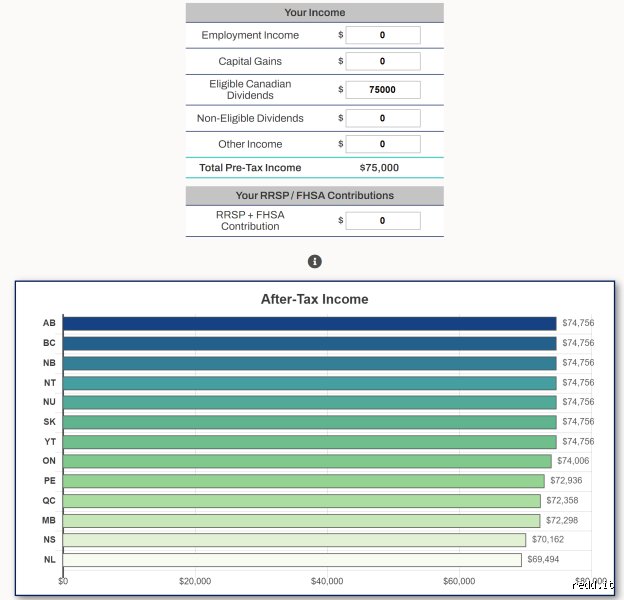

Taxes, Deductions, and the Illusion of the High-Income Take-Home Pay

Let us talk about the tax man, because gross income is ultimately a vanity metric. When a Canadian crosses the $75,000 total income mark, they firmly enter middle-tier marginal tax brackets that vary wildly depending on their province of residence. It is one thing to see that number printed at the bottom of a employment contract; it is quite another to witness the systematic dissection of your bi-weekly paycheck via Employment Insurance (EI), Canada Pension Plan (CPP) contributions, and progressive income tax rates.

The Provincial Tax Grinder: From Alberta to Quebec

The math is brutal and unyielding. In Alberta, a worker making $75,000 benefits from a relatively flat provincial tax structure, allowing them to retain a larger portion of their hard-earned dollars. Contrast that with Quebec or Nova Scotia, where provincial brackets accelerate rapidly to fund robust social safety nets. In Montreal, for example, your marginal tax rate on those top dollars climbs significantly higher, meaning that two individuals with identical gross incomes across Canada possess fundamentally unequal economic leverage. Which explains why looking solely at a national percentage of earners fails to capture the true distribution of disposable capital.

The Stealth Erosion of the Middle-Class Paycheck

Wages across the country grew by an average of 3.1% through 2025, a noticeable deceleration from the sharper spikes witnessed during the immediate post-pandemic labor shortages. This cooling labor market means that while more Canadians are technically pushed over the $75,000 line due to nominal cost-of-living adjustments, their purchasing power has actually retrograded. I argue that we are witnessing the birth of the "poor high-earner"—a psychological and economic state where an individual makes a salary that sounds impressive on paper but feels entirely inadequate at the grocery checkout counter or the gas pump. Exceptional wages have been neutralized by systemic costs.

How Individual Earnings Compare to Household Economic Realities

To understand the full scope of Canadian wealth, we have to look past the individual and examine the household unit, where the financial calculus shifts dramatically. While a single person making over $75,000 belongs to an exclusive 26.8% minority, a dual-income household where both partners make the median wage of $44,000 easily clears a combined $88,000. This reality creates an intense divergence in lifestyle and economic resilience between single tax filers and coupled census families.

The Single Tax Penalty in Modern Canadian Society

The individual earner clearing $75,000 carries the entire burden of shelter, utilities, and taxation alone. They receive no structural relief from the tax code, unlike a family unit that can strategically optimize child care benefits or balance lower-income tax brackets through common-law filings. Hence, the single professional making eighty thousand dollars often finds themselves with less disposable income at the end of the month than a dual-income couple making forty-five thousand each. It is a structural quirk of the Canadian socioeconomic fabric that people simply do not analyze with enough depth.

Household Quintiles and the Growing Wealth Disparity

Statistics Canada reports that the income gap between the top 40% and the bottom 40% of households widened to 46.7 percentage points by the close of 2025. This widening chasm is driven primarily by investment income and equity gains rather than raw labor wages. Therefore, even if you find yourself among the top quarter of individual wage earners, you are still running a race against an investor class whose wealth propagates independently of an hourly wage or an annual salary. The real divide in Canada isn't between those making $50,000 and those making $75,000; it is between those who rely entirely on a T4 slip and those who generate liquidity through capital assets.

Common mistakes and misconceptions

The problem is that our brains love simple answers, meaning we routinely conflate different metrics when discussing what percentage of Canada makes over 75K. A classic blunder involves mixing up individual tax filers with household units. When Statistics Canada publishes numbers, they often separate these groups. Yet, everyday conversations casually blur the line. Why does this matter? If you look at individual gross income across the country, making 75,000 dollars places you comfortably above the national median, which hovers closer to 46,900 dollars. But if you apply that exact same 75,000 dollars to an entire household income, you are suddenly looking at a reality where you sit in the lower end of the middle class. Let us be clear: a single person making this amount has vastly different purchasing power than a family of three surviving on the identical total sum.

The gross versus net delusion

Another profound trap is ignoring the heavy bite of the Canadian tax system. People frequently look at a 75,000 dollars salary and assume it translates to abundant disposable wealth. Except that progressive tax brackets, Canada Pension Plan contributions, and Employment Insurance premiums quickly erode that number. Your glowing 75,000 dollars sticker price quickly morphs into an after-tax reality of roughly 53,000 to 58,000 dollars depending entirely on your province. Believing that gross income equals walking-around money is a widespread delusion that warps collective debates about wealth.

The geographic equalization trap

We often treat Canada as a uniform economic monolith. It is not. An income of 75,000 dollars in rural New Brunswick grants you a highly privileged standard of living. Try navigating the housing market of Vancouver or Toronto on that exact same individual salary, and the illusion of wealth completely evaporates. Which explains why looking only at national percentages fails to tell the true story of local purchasing power.

Little-known aspect or expert advice

The conversation around what percentage of Canada makes over 75K consistently overlooks the massive influence of age demographics and career staging. Data is rarely static. An individual's earnings trajectory generally peaks between the ages of 45 and 54, meaning the macro percentages are heavily skewed by older generations who entered the workforce decades ago. If you are a 24-year-old worker feeling discouraged because you fall below the 75,000 dollars threshold, you are comparing yourself to professionals with twenty years of compounding experience.

The hidden power of indexing and benefits

As an expert looking at these structural figures, my advice is to stop focusing exclusively on the raw salary number. Total compensation, including defined-benefit pensions or comprehensive health coverage, frequently offsets a lower base wage. A public sector worker earning 70,000 dollars with an indexed pension plan is often financially safer than a contract tech worker pulling in 80,000 dollars with zero security. In short, stop letting a single number on a tax return dictate your perceived financial status in the Canadian landscape.

Frequently Asked Questions

What percentage of individual Canadian tax filers earn more than 100,000 dollars annually?

According to recent individual tax filer data compiled by Statistics Canada, approximately 11 to 14 percent of single earners surpass the 100,000 dollars threshold. This small cohort represents the upper tier of workers, meaning that crossing this six-figure mark places you well within the top 15 percent of all individual Canadian earners. The issue remains that while 100,000 dollars was once considered the ultimate benchmark of extreme wealth, inflation has eroded its status significantly. As a result: achieving this milestone no longer guarantees easy entry into the housing market in metropolitan areas like Toronto, where bungalows routinely clear seven figures.

How does the proportion of Canadians making over 75,000 dollars vary by gender?

Gender disparity continues to shape the statistical distribution of higher incomes across Canada. Men still occupy a disproportionately larger share of the income brackets above 75,000 dollars, which is largely driven by their overrepresentation in high-paying sectors like resource extraction, engineering, and specialized trades. Statistics Canada reports that within the top 1 percent of earners, women comprise roughly 26 percent of the total group. While this specific metric has steadily risen from a mere 11 percent in the early 1980s, progress across the broader 75K bracket remains slow but visible.

Is an income of 75,000 dollars considered middle class in Canada today?

An individual income of 75,000 dollars sits squarely within the modern definition of the Canadian middle class, which generally spans from 53,000 to 141,000 dollars. But let's be clear: your definition of middle class depends heavily on whether you already own real estate (a massive parenthetical aside that changes everything). If you are renting a modern apartment in a major urban center, this specific salary will feel remarkably tight. Conversely, if you reside in a region with affordable housing, this exact same income yields a highly stable, classic middle-class lifestyle with room for savings.

Engaged synthesis

Fixating blindly on what percentage of Canada makes over 75K misses the structural crisis defining the modern Canadian economy. We have become a nation obsessed with income brackets while completely ignoring the brutal reality of regional living costs and generational wealth gaps. The truth is that earning 75,000 dollars is statistically impressive on paper, yet it increasingly feels like financial survival in our major metropolitan cities. I take the firm stance that looking at income isolation is entirely obsolete; we must analyze wealth distribution and housing inflation concurrently to understand true prosperity. Stop measuring your financial health solely against national salary percentiles that fail to account for local economic realities. Our focus must shift away from arbitrary income milestones and look directly toward building sustainable purchasing power for the average citizen.