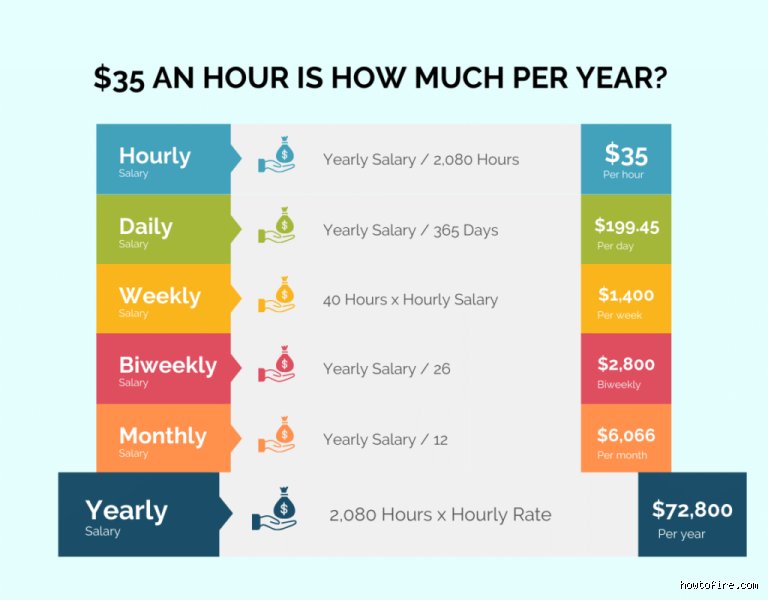

The Baseline Calculation: Deconstructing the ,000 Benchmark

To understand the foundation of what is $35 an hour annually, we have to use the standard corporate calendar which assumes a 40-hour workweek across 52 weeks. Multiply those together and you get 2,080 hours, yielding a gross total of $72,800. Except that people don't think about this enough: almost nobody works every single one of those hours without taking a breather. Whether it is unpaid sick leave, a couple of weeks of well-deserved vacation, or the occasional federal holiday, the practical reality for hourly workers usually aligns much closer to a flat 2,000 hours of paid time. That changes everything because it drops your realistic base expectation to $70,000, creating an immediate gap between paper wealth and the actual cash hitting your checking account. The thing is, this distinction matters immensely if you are planning a household budget or trying to qualify for a mortgage in a competitive market like Austin or Columbus.

The Math Behind the Hours

Let's break this down into digestible fragments. If we look at a single month, a 173.33-hour average translates to roughly $6,066 in gross earnings. Weekly, you are looking at $1,400. But because cash flow is the lifeblood of daily survival, the bi-weekly paycheck of $2,800 is the number you will actually see staring back at you on your banking app. It sounds substantial, yet that number is an illusion.

Where It Gets Tricky: The Brutal Reality of Net Take-Home Pay

Here is my hot take on modern compensation: quoting gross salary is a borderline useless metric for the average worker. Why? Because the distance between a $72,800 gross revenue and your actual disposable income is a chasm filled with mandatory withholding taxes, localized levies, and benefit deductions. If you happen to live in a state with no income tax like Texas or Florida, your paycheck retains a decent amount of its original muscle. But pack your bags for California or New York, and suddenly the local treasury bites hard. For a single filer living in Los Angeles in 2026, FICA taxes—comprising 6.2% for Social Security and 1.45% for Medicare—combine with federal and state progressive brackets to eat roughly 22% to 25% of your earnings right off the top. As a result: your shiny $70,000 annual dream shrinks down to a take-home reality of approximately $53,000, and we haven't even talked about healthcare premiums yet.

The Hidden Costs of Employer Deductions

Pre-tax contributions can quietly hollow out what remains of your purchasing power. A standard medical insurance premium for a single individual often runs around $150 per pay period, while a modest 5% contribution to a company 401k plan subtracts another $140 bi-weekly. Suddenly, that robust hourly rate yields a net bi-weekly paycheck of just under $1,850. Is that enough to live well? Honestly, it's unclear because it depends entirely on your lifestyle baseline.

The Disparity of Geographic Purchasing Power

Consider two different realities. A remote graphic designer earning $35 an hour while living in Cincinnati, Ohio, can easily secure a comfortable two-bedroom apartment, cover their Honda Civic payment, and still have enough surplus to invest in a brokerage account. But take that exact same hourly wage to Manhattan or San Francisco, where the median rent for a studio apartment routinely eclipses $3,000 a month, and you are suddenly staring down the barrel of functional poverty. We're far from it being a universal middle-class ticket anymore.

Evaluating What Is an Hour Annually Against the Broader Economy

To truly grasp where this income positions you, it helps to look at how it stacks up against the rest of the American workforce. The Bureau of Labor Statistics recently pegged the national median hourly wage for all occupations significantly lower than this mark. By earning $35 an hour, you are effectively out-earning more than 65% of the working population, positioning yourself on the upper rungs of the working class or the entry level of the true middle class. Yet, the issue remains that inflation over the past few years has dramatically shifted what this money can actually buy. A $70,000 salary today holds the same purchasing power that roughly $56,000 did a decade ago, meaning you have to run faster just to stay in the exact same economic place.

The Lifestyle Boundaries of a k Income

What does this look like when you walk into a grocery store or try to book a vacation? With a disciplined budget, this wage easily covers the necessities of shelter, food, utilities, and insurance while leaving a reasonable margin for entertainment. But—and this is a massive caveat—the margin evaporates the moment you introduce childcare expenses or heavy student loan debts into the equation. For a single parent paying $1,200 a month for daycare, a $35 hourly rate stops feeling like a milestone and starts feeling like a daily tightrope walk.

Alternative Compensation Structures: Overtime and Freelance Dynamics

Up until now, we have assumed a rigid, predictable 40-hour schedule, which is rarely how the modern labor market functions for hourly professionals. If your position qualifies for overtime under the Fair Labor Standards Act, those extra hours become incredibly lucrative. At time-and-a-half, your hourly rate skyrockets to $52.50 for every hour worked past the standard 40-hour threshold. Work just five hours of overtime each week for a year, and you will add an extra $13,650 to your annual gross, pushing your total compensation well past the $86,000 mark. Which explains why many tradespeople and healthcare workers fiercely protect their overtime privileges.

The Independent Contractor Trap

Except that the math completely breaks down if you are working as a 1099 independent contractor rather than a W-2 employee. Freelancers earning $35 an hour must personally absorb the employer’s half of the FICA tax, amounting to an extra 7.65% self-employment tax burden. Furthermore, without paid time off, every single day you spend sick or vacationing reduces your annual earnings directly. When you factor in the out-of-pocket cost of purchasing private health insurance on the open market exchange, a freelancer needs to bill closer to $50 an hour just to match the economic stability of a $35 an hour W-2 job.