The Shock of the Takeover: What is the Pension Benefit Guaranty Corporation Anyway?

When a company goes belly up or simply cannot fund its defined benefit plan, the federal government steps into the wreckage. The PBGC acts as an insurance framework, but it does not operate like a traditional, benevolent insurer. It is a massive bureaucratic entity. It assumes control of the remaining assets, reviews thousands of employment records, and eventually pays out benefits according to strict statutory limits. The thing is, your original plan rules do not vanish entirely, but they get filtered through a complex web of federal maximums. People don't think about this enough until they receive that cold, official letter in the mail announcing their plan's termination.

The Two Different Entities: Single-Employer vs. Multiemployer Plans

Where it gets tricky is the fundamental divide in how the agency operates. If you worked for a single corporation—say, an airline or a steel manufacturer that went bankrupt—your plan falls under the single-employer program. Multiemployer plans, conversely, involve union agreements across entire industries like trucking or construction. I have watched analysts debate the stability of these programs for years, and honestly, it is unclear how certain long-term funding deficits will morph, yet the immediate rules governing your payout age remain rigidly distinct based on this classification.

Cracking the Code: What Age Can I Collect My PBGC Pension Without Penalties?

The magic number for a full, unreduced payout is typically age 65. This is defined as the normal retirement age under the vast majority of trusteed plans. But what if your original company promised you could walk away with full benefits at 62? That changes everything, except that the PBGC imposes its own overriding caps. If you decide to claim your monthly check before reaching their designated normal retirement age, the agency slashes the benefit using specific actuarial reduction factors for every single month you participate early.

The Steep Cost of Early Retirement at Age 55

Can you actually retire at 55? Yes. Should you? That is a completely different question. For every year you pull benefits prior to age 65, the payout shrinks by a massive percentage (often around 5% to 7% annually depending on the specific plan plan structure). Imagine expecting a $2,000 monthly check but receiving closer to $1,000 just because you could not wait. But because some workers face sudden unemployment or health crises, that heavily reduced early pension becomes their only viable lifeline. It is a financial compromise that requires cold, hard math rather than emotional wishful thinking.

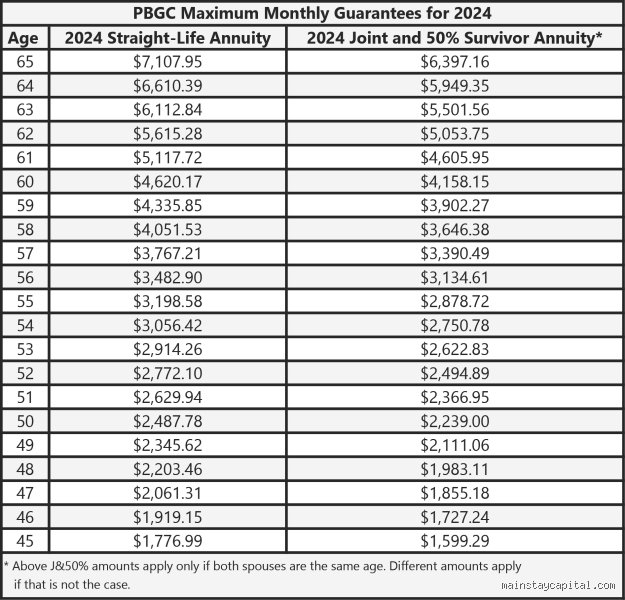

The 2026 Maximum Guarantee Tables and Why They Matter

Every year, the government adjusts the maximum amount it is legally allowed to pay out to an individual. For a 65-year-old retiring in a recently terminated plan, the statutory cap might hover around several thousand dollars a month, but that cap plummets dramatically if you are only 55. The agency calculates these limits based on the exact date your plan failed and your age when you begin receiving payments. If you were a high earner expecting a massive executive pension, these federal caps will likely chop off a significant portion of your anticipated wealth.

The Hidden Variables That Shift Your Retirement Timeline

Nothing with a federal agency is ever truly straightforward. Your target age is not just a date on a calendar; it is a moving target influenced by phase-in rules and complex legal provisions. For instance, if your plan was amended to increase benefits within five years of the collapse, the PBGC will not guarantee that full increase. They phase it in at 20% per year. Why do they do this? To prevent dying companies from promise-loading their pensions right before dumping the liability onto the taxpayers.

The Impact of Surviving Spouse Options on Your Age Strategy

Choosing when to collect also forces a tough conversation about joint and survivor annuities. If you want to ensure your spouse continues to get a check after you pass away, your monthly benefit drops even further from the baseline. Did you know that the PBGC automatically reduces your payout to fund a 50% survivor benefit unless your spouse waives it in writing? This means a 60-year-old worker faces a double reduction: one for retiring early, and another to protect their partner. It is a heavy financial pill to swallow.

Comparing the PBGC Payout Timeline to Social Security and Traditional IRAs

We are far from the simplicity of a unified retirement age across the board. Your PBGC timeline operates completely independently from Social Security Administration rules. You might hit your full PBGC age at 65, while your Social Security Full Retirement Age sits at 67 for anyone born in 1960 or later. This creates a awkward two-year gap where you have to patch together income from personal savings or part-time work if you want to maximize both streams. Meanwhile, traditional IRAs allow penalty-free withdrawals at age 59 and a half, adding another layer of chronological confusion to your strategy.

The Danger of the Subsidy Mirage

Many private corporate pensions offer early retirement subsidies—special temporary boosts to bridge the gap until you can claim Social Security. Forget about them. The moment the federal government takes over the fund, those temporary supplements usually evaporate into thin air. The issue remains that workers frequently build their entire early retirement plan around these corporate promises, only to realize the safety net only covers the bare-bones basic annuity. As a result: reliance on old benefit statements from a defunct employer can ruin your financial future. Always request an official, specific benefit determination directly from the agency before making any permanent life changes.

Common Mistakes and Misconceptions Regarding PBGC Timelines

Thinking the Pension Benefit Guaranty Corporation operates exactly like your old HR department is a fast track to financial disappointment. It does not. Many future retirees assume that the moment they blow out the candles on their 65th birthday, a magical direct deposit appears. The problem is, government bureaucracies require paperwork, verification, and patience. If you sit around waiting for them to contact you, your wallet will suffer the consequences.

The "My Plan Rules Still Apply" Delusion

When a private pension goes under and the feds step in, the original rulebook gets a serious haircut. You might think you can still grab that juicy 30-and-out early retirement subsidy your union negotiated back in 1995. Except that the PBGC imposes its own statutory maximums and reductions. They recalculate everything based on ERISA guidelines, meaning your expected windfall could easily shrink. Why risk your retirement security on outdated company handbooks that no longer hold weight?

Assuming Maximum Caps Apply to Everyone

Every year, headlines trumpet the rising maximum guarantee limits, tempting people to assume they will pocket the full amount. For instance, the 2026 maximum for a 65-year-old retiree receiving a straight-life annuity is a specific statutory ceiling, but that figure drops drastically if you retire earlier. Let's be clear: if you flip the switch at age 55 instead of 65, your monthly check is slashed by a massive percentage to account for those extra ten years of payouts. Furthermore, if you chose a joint-and-survivor option to protect your spouse, that headline maximum shrinks even further.

The Diligent Search Obligation and Expert Navigation

Here is something your former colleagues probably do not know: the PBGC will not hunt you down like a bounty hunter when you hit early retirement age. They manage millions of participants, which explains why the onus of tracking down your money falls squarely on your shoulders. If they lose your current address, your benefits simply sit there, gathering dust but zero interest.

Unclaimed Dollars and the Missing Participants Program

The agency holds onto millions in unclaimed pension assets from terminated defined benefit plans. If you vanished from their radar decades ago, you have to proactively use their online directory to claim what is yours. But do not expect retroactive payments stretching back years if you simply forgot to file on time. They generally only pay back-benefits to the date you actually became eligible or when the plan terminated, depending on specific plan mechanics, meaning procrastination costs you real money.

Frequently Asked Questions

Can I begin receiving my payout at age 55 if my original plan allowed it?

Yes, you can typically choose to start your monthly benefits as early as age 55, but doing so comes with a permanent financial penalty. The agency reduces your monthly check for each month you retire before reaching the normal retirement age of 65 to offset the longer payout period. For example, a worker whose plan collapsed might see their base benefit slashed by roughly 5% to 7% for each year they anticipate their normal retirement date. This means jumping the gun at 55 could permanently cut your monthly pension check by up to 50 percent of the total value you would have received by waiting. As a result: patience pays off mathematically, while early filing permanently locks in a lower standard of living.

What happens to my payment if I keep working past age 65?

Continuing to punch the clock past your 65th birthday will not stop you from collecting, but it alters the math. Unlike Social Security, which implements a strict retirement earnings test that can temporarily claw back your benefits, the PBGC does not care how much money you earn at a completely new job. Yet the issue remains that your monthly benefit will not automatically increase just because you delayed past age 65, unless your specific terminated plan contained explicit provisions for late-retirement actuarial increases. You must formally submit your application regardless of your employment status, or you risk leaving thousands of dollars on the table completely uncollected.

Are my step-down or early retirement supplements guaranteed by the feds?

Temporary supplements designed to bridge the gap between early retirement and your Social Security eligibility are rarely fully covered. The federal safety net is designed to protect basic, permanent retirement benefits rather than temporary gimmicks or temporary buyout incentives your old employer used to downsize the workforce. Under strict federal insurance rules, any benefit that drops or disappears after you reach a certain age is generally categorized as a non-guaranteed supplemental benefit. Consequently, the agency will strip these temporary add-ons away during the plan rehabilitation phase, leaving you with only the core, lifetime annuity calculation.

A Final Verdict on Timing Your Application

Waiting until the absolute last minute to figure out your pension timeline is a recipe for financial disaster. We see too many workers treat federal pension guarantees as a passive safety net rather than an active financial instrument that requires aggressive management. The math dictates that maximizing your monthly check requires balancing your personal health reality against the steep early retirement penalties imposed by federal law. Do not let laziness dictate your lifestyle during your golden years. Treat this application process like a second job, document every single communication with federal administrators, and demand clarity on your net monthly distribution before finalizing your exit from the workforce.