The Evolution of Global Thirst and Liquid Capital

We need to talk about how a medicinal syrup concocted in an 1886 Atlanta pharmacy became a geopolitical staple. It wasn't accidental. The global beverage landscape shifted dramatically after World War II, a period where the company guaranteed that every American soldier could buy a bottle for a nickel, regardless of where they were stationed. That changes everything. By embedding itself into military logistics, the brand established bottling plants across Europe and Asia, effectively subsidizing its own international expansion.

Decoding the Core Definition of a Global Beverage

What actually qualifies a drink to top the international charts? Industry analysts at Euromonitor look at gross retail value, volume displacement, and geographic penetration. It is not just about selling a lot of liquid in one populous country. Thums Up dominates parts of India, yet it barely registers on the global scale, which explains why true dominance requires winning across multiple continents simultaneously. The thing is, most regional favorites fail to cross oceans because taste preferences are stubborn things.

The Disruption of Regional Palates

Yet, local resistance persists. In Peru, a yellow, bubblegum-flavored soda called Inca Kola outsold the American giant for decades, forcing the Atlanta firm to simply buy a 50% stake in the Peruvian company to neutralize the competition. It was a brilliant, cutthroat move. Honestly, it's unclear if any pure homegrown brand can ever replicate that kind of defensive market maneuver on a global stage again.

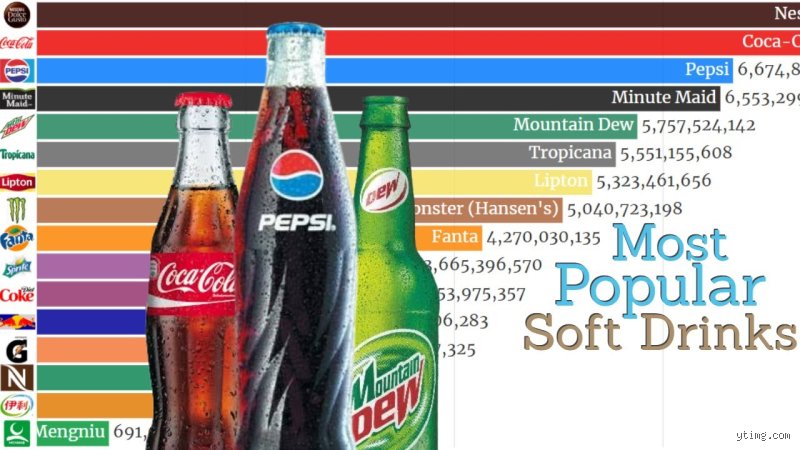

Dissecting the Market Share of Coca-Cola Classic

Let's look at the raw data because numbers do not lie, even when the beverage industry tries to obfuscate them behind confusing metrics. In 2024, the parent company's net revenues eclipsed 45 billion dollars, a staggering sum driven largely by its flagship cola. PepsiCo might boast higher overall corporate revenues, but—and here is the kicker—that is because of their massive Frito-Lay snack empire, meaning their liquid division trails significantly. When we isolate pure beverage volume, the red brand wins by a landslide.

The Statistical Gulf Between First and Second Place

The gap is downright embarrassing for competitors. In the United States alone, the flagship red can holds roughly 19% of the total liquid refreshment market, while Dr Pepper and Pepsi battle furiously for a distant second place at around 8.3% each. Think about that for a second. The number one soft drink in the world possesses a market share nearly double that of its closest rivals combined on its home turf, a trend that replicates itself across Latin America and Europe.

Why Diet and Zero Sugar Variants Alter the Calculus

Where it gets tricky is the modern shift toward health consciousness. The rise of Coca-Cola Zero Sugar has created a secondary engine of growth, capturing a demographic that loves the heritage flavor profile but despises the 39 grams of high-fructose corn syrup packed into a standard 12-ounce serving. This formulation wizardry saved the company from the steep declines facing traditional sugary sodas. It kept the brand relevant among millennials who grew up hearing warnings about metabolic syndrome.

The Psychological Warfare of Modern Distribution Systems

You cannot buy what you cannot see. The secret weapon of the world's favorite beverage isn't the closely guarded merchandise recipe locked in an Atlanta vault; it is the terrifyingly efficient route-to-market strategy. They have perfected a system of franchised bottlers. The corporate parent manufactures concentrate, then sells it to local bottling partners who handle the heavy lifting of physical distribution. Because of this decentralized architecture, a fresh bottle can reach a remote village in the Andes faster than local government aid.

The Fountain Monopoly in Fast Food Chains

And then we must consider the exclusive pouring rights. The legendary 1955 pact between McDonald's and the beverage giant changed the restaurant industry forever, creating a symbiotic relationship where the fast-food chains serve the soda via specialized stainless-steel syrup tanks instead of standard plastic bags. This ensures the crispest, most heavily carbonated pour imaginable. As a result: generations of consumers have been conditioned to believe that the burger-joint version tastes exponentially better than the supermarket cans.

The Ubiquity of the Cold Drink Equipment Fleet

People don't think about this enough, but those red glass-front coolers positioned next to supermarket cash registers are corporate real estate. The beverage company owns them. They lease them to store owners under strict contractual obligations that forbid the placement of any competitor products inside. This aggressive strategy ensures absolute visual dominance at the exact moment a shopper decides to make an impulse purchase.

The Alternative Contenders and Cultural Outliers

Is anyone actually capable of dethroning the king? If we look strictly at pure volume within a single territory, the results get weird. Take Irn-Bru in Scotland, a bright orange carbonated drink that has historically beaten the global leader in per-capita consumption, fueled by a national identity that prides itself on rejecting standard American imports. But Scotland is a tiny market. The issue remains that regional victories do not translate to global coups.

The Energy Sector and the Rise of Functional Beverages

Except that the definition of a soft drink is mutating. Brands like Red Bull and Monster are capturing the attention of Gen Z consumers who view traditional colas as their parents' drinks. Red Bull sold over 12 billion cans globally in recent years, utilizing extreme sports sponsorships to cultivate an edgy aura that traditional soda brands simply cannot match with standard Santa Claus holiday commercials. But energy drinks are expensive, niche products compared to the mass-market affordability of a basic cola.

The Mexican Coke Phenomenon and Premiumization

Even within the brand's own ecosystem, a strange hierarchy has emerged. Mexican Coke, imported into the United States in distinctive glass bottles and sweetened with pure cane sugar instead of corn syrup, has achieved cult status among foodies. It commands a premium price point. I find it mildly ironic that consumers are willing to pay double the price just to experience the beverage the way it was originally formulated before corporate accountants optimized the supply chain in the 1980s.