Beyond the Shiny Brochures: What Is the KPMG Controversy at Its Core?

Let us be real for a moment. Auditing sounds boring, the kind of dry, spreadsheet-heavy work that keeps the global economy humming along in the quiet background. Except that when it fails, societies fracture. The KPMG controversy is not a singular event; rather, it is a persistent pattern of looking the other way while massive corporate clients cook their books, paired with internal ethical lapses that shocked even seasoned Wall Street veterans. It is about a culture that allegedly prioritized lucrative consulting fees over rigorous, independent skepticism.

The Architecture of a Global Auditing Giant

To understand how we got here, you have to look at the sheer scale of the network. KPMG operates as a decentralized cooperative of independent member firms spanning over 140 countries, a structure that defenders claim limits localized liability but critics argue allows systemic malpractice to flourish without centralized accountability. But where it gets tricky is the inherent conflict of interest. How do you aggressively audit a multinational conglomerate when that same corporate board holds the power to fire you or dangle multi-million dollar non-audit advisory contracts in front of your partners? We are far from the idealized vision of independent financial oversight taught in business schools.

A Culture Strung Out on Billable Hours

The issue remains deeply rooted in institutional culture. Behind the glossy recruitment drives promising corporate social responsibility lies a hyper-competitive pressure cooker where meeting revenue targets frequently eclipses the tedious, adversarial work of true forensic accounting. I believe we have reached a point where these firms view regulatory fines merely as a standard cost of doing business, a cynical line item in an annual budget. When partners are judged almost exclusively on the revenue they generate rather than the fraud they uncover, structural failure becomes an absolute certainty.

The Fatal Blindspots of the Carillion Collapse and British Economic Tremors

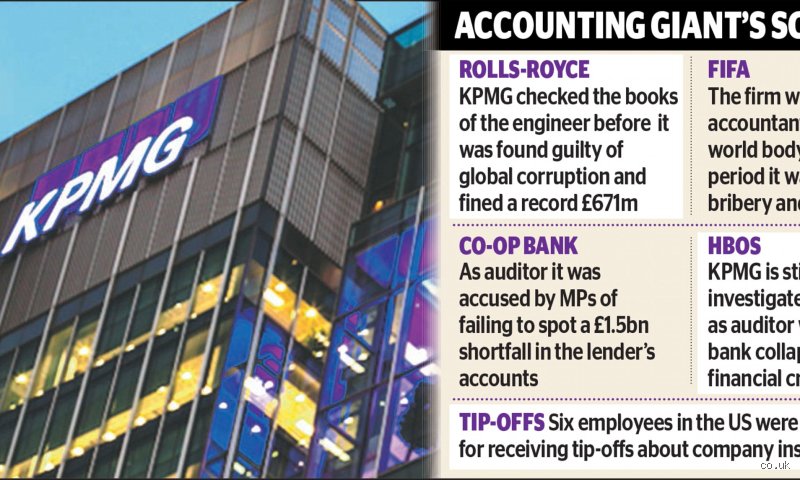

If you want to pinpoint the moment the British public realized the system was profoundly broken, look no further than January 15, 2018. That was the day Carillion, a massive government contractor managing everything from hospital catering to military housing, went into compulsory liquidation with 7 billion pounds in liabilities and a pathetic 29 million pounds in cash left on its balance sheet. It was the biggest corporate failure in modern British history, and guess who had signed off on their accounts as a clean bill of health just months prior? KPMG had pocketed roughly 29 million pounds over nineteen years of auditing Carillion, failing to issue a single qualified opinion despite the company's aggressive, debt-fueled accounting practices and rapidly deteriorating cash flow.

Signaling All Clear While the Ship Was Sinking

The UK Financial Reporting Council eventually handed down a record-breaking 21 million pound fine in 2023 for what it described as an extraordinary lack of objectivity and challenge. But the thing is, the rot ran even deeper than mere incompetence. During the subsequent investigation, it was revealed that rogue partners had actually falsified documents, creating misleading meeting minutes and retroactively altering spreadsheets to deceive the regulators who were reviewing their Carillion work. That changes everything. It transformed a narrative of mere professional negligence into a dark, deliberate conspiracy to mislead public watchdogs.

The Human Cost of Corporate Accounting Blindness

Because when a giant like Carillion vanishes overnight, the shockwaves tear through the real world, far away from air-conditioned boardroom suites. Thousands of sub-contractors went unpaid, small family businesses collapsed into bankruptcy, and vital infrastructure projects like the Royal Liverpool University Hospital were delayed for years. Yet, despite a scathing parliamentary report declaring that the Big Four acted as a cozy club protected by an ineffective regulator, no senior executives went to prison. Honestly, it is unclear whether the industry learned anything at all from this debacle, except perhaps to hide their tracks a little better next time.

Stealing the Exam Papers: The PCAOB Leak Scandal That Shocked Washington

Across the Atlantic, the nature of the KPMG controversy took an even more surreal, almost cinematic turn toward outright espionage. In 2019, a federal court sentenced the firm's former national partner-in-charge of audit quality to prison for his role in a conspiracy to alter audit files after illegally obtaining confidential regulatory schedules. The Public Company Accounting Oversight Board, an official body created in the wake of the Enron disaster to police auditors, had a mole inside its ranks who was leaking secret lists of which KPMG audits were slated for upcoming, unannounced inspections.

Fixing the Audit Inspection Game Before It Starts

Imagine a university student getting their hands on the final exam questions a week early; that is precisely what happened here. Having received horribly low marks on its public audits in previous years—with regulators finding significant deficiencies in nearly half of the inspected files—senior leadership desperately wanted to avoid another public embarrassment. As a result, they used the stolen data to quietly go back and clean up specific, messy client files before the inspectors arrived on site. It was an institutional betrayal of the highest order, striking at the very mechanism designed to keep the financial markets honest.

A High-Stakes Brain Drain and Regulatory Capture

The firm ended up paying a 50 million dollar penalty to the Securities and Exchange Commission to settle the charges, alongside terminating several top-tier partners. But people don't think about this enough: how did a regulatory body become so easily infiltrated by the very entity it was meant to oversee? The revolving door between elite accounting firms and Washington regulatory agencies creates a dangerously cozy ecosystem where lines of allegiance blur. Which explains why, despite the historic fines and blistering press releases, the structural framework of Wall Street oversight remains virtually untouched.

Monopolies and Meltdowns: How the Big Four Stranglehold Distorts Accountability

Whenever a major corporate scandal erupts, politicians inevitably threaten to break up the dominant accounting cartels, yet nothing ever changes. We currently live in an economic reality dictated by the Big Four—Deloitte, PwC, EY, and KPMG—who collectively audit over 97 percent of US public companies with revenues exceeding 1 billion dollars. This extreme market concentration creates a terrifying "too big to fail" dilemma for global regulators. If a government were to bar one of these firms from operating due to systemic fraud, the global financial system would grind to a halt because the remaining three giants simply do not have the capacity to absorb the massive workload.

The Illusion of Choice in Corporate Auditing

Hence, regulators find themselves trapped in a corner, forced to issue fines that look massive on paper but represent just a fraction of the firm's multi-billion dollar global revenues. What alternatives truly exist for a multinational bank or a global aerospace firm? Mid-tier networks like BDO or Grant Thornton are frequently passed over by large corporate boards who demand the global reach and prestige of a premier brand, even when that brand is mired in controversy. It is an airtight monopoly where poor performance and ethical lapses rarely result in a loss of market share, completely upending the traditional capitalist rule that bad actors are punished by consumers.

Common mistakes and misconceptions about the audit giant's failures

The single-event illusion

Most observers talk about the KPMG controversy as if it were a solitary, isolated lapse in judgment. It is not. The public memory glues itself to the spectacular collapse of Carillion in 2018 or the South African Gupta family scandal, assuming a sudden, freak systemic malfunction occurred. Let's be clear: auditing giants do not implode overnight due to one bad spreadsheet. Structural rot takes years to fester. When the UK Financial Reporting Council fined the firm a record 21 million pounds in 2023 for its catastrophic Carillion oversight, it exposed a chronic, deeply embedded culture of complacency. We often mistake the spectacular explosion for the spark, ignoring the years of accumulated dry wood that preceded the fire.

Confusing an audit with an absolute guarantee

Why do markets panic when a clean health bill precedes a corporate bankruptcy? Because investors fundamentally misunderstand what an auditor actually does. You probably think a clean sign-off means a company is financially bulletproof. The issue remains that an audit merely measures compliance with accounting frameworks, not operational viability. Yet, when KPMG signed off on Silicon Valley Bank just fourteen days before its dramatic 2023 collapse, the market felt betrayed. Was it fraud? No, it was a terrifying liquidity run, which explains why the traditional audit metrics failed to signal the impending doom. It highlights the vast, dangerous expectation gap between public perception and accounting reality.

The myth of the rogue employee

Corporate communications departments love the bad apple narrative. When the 2017 PCAOB leak scandal erupted in the United States, involving former regulators sharing confidential inspection data with top executives, the initial response framed it as isolated misconduct. But how can an organization claim isolation when multiple senior partners are actively participating in the deception? Systemic institutional pressure to maintain prestige drove that behavior. Except that acknowledging this requires admitting that the entire business model might be compromised, a confession no Big Four firm is willing to make.

The hidden structural conflict and expert survival advice

The consulting chokehold on independent oversight

The real engine driving the KPMG controversy is an open secret within the financial sector. Auditing is a low-margin, highly commoditized chore, whereas consulting is a goldmine. Can a firm truly remain a fierce, unbiased watchdog when it simultaneously chases lucrative advisory contracts from the exact same corporate clients? It is highly improbable. In short, the structural framework of the Big Four incentivizes a culture of appeasement rather than rigorous skepticism. As a result: the public loses faith in financial statements, capital markets become volatile, and regulatory fines are simply absorbed as a routine cost of doing business.

How to navigate the murky waters of corporate reports

If you are an investor trying to protect your capital, blindly trusting an auditor's stamp is financial suicide. What should you do? Look beyond the headline opinion page. Dig deeply into the Critical Audit Matters section of the annual report, where the specific areas of high accounting risk and intense subjective judgment are laid bare. Look for frequent changes in accounting estimates or aggressive revenue recognition policies. We must accept our limits as external observers, but we can certainly spot the red flags of aggressive accounting before the inevitable regulatory intervention occurs.

Frequently Asked Questions about the ongoing scrutiny

What triggered the massive 21 million pound fine against the firm in the United Kingdom?

The UK Financial Reporting Council imposed this historic financial penalty in October 2023 due to a total breakdown in the auditing of Carillion, a massive government contractor that collapsed in 2018 under 7 billion pounds of debt. Investigators discovered that the audit team failed to challenge management's deeply flawed assumptions regarding major construction contracts and goodwill valuations. Furthermore, the firm loss-provisioning assessments were severely deficient, misleading the market into believing the company was stable. This specific KPMG controversy highlighted an extraordinary lack of professional skepticism during the 2014 to 2016 review periods. Ultimately, the collapse cost thousands of jobs and forced the regulatory body to demand unprecedented structural changes within the firm's British operations.

How was the firm implicated in the South African state capture scandal?

During the mid-2010s, the firm became deeply entangled with the wealthy Gupta family, who were accused of using their close ties to former President Jacob Zuma to influence state appointments and siphon billions from state-owned enterprises. The firm's local branch missed glaring red flags, failing to report suspicious transactions and allowing Gupta-linked entities to improperly classify wedding expenses as business costs to evade taxes. An internal investigation later forced the resignation of eight top South African executives in 2017, completely shattering the firm's regional reputation. The fallout was swift, with major banking institutions and government agencies immediately severing ties with the disgraced auditor. Did the global leadership react fast enough to contain this ethical catastrophe? The consensus among international governance experts remains a resounding no.

Why did the Silicon Valley Bank collapse renew intense scrutiny on their American practice?

The firm found itself in the crosshairs of global regulators after signing off on the financial health of both Silicon Valley Bank and Signature Bank mere weeks before their historic failures in March 2023. Critics pointed out that the audit reports failed to include a going-concern warning despite the banks' massive exposure to rising interest rates and unhedged bond portfolios. While the firm maintained that subsequent unprecedented depositor bank runs were unpredictable, the omission sparked furious debates in Congress regarding the adequacy of banking audits. A group of shareholders subsequently launched lawsuits, alleging that the firm ignored critical vulnerabilities that directly led to the erasure of billions in market value. This specific aspect of the KPMG controversy amplified calls for the SEC to fundamentally reform how accounting firms evaluate interest rate risk in an inflationary environment.

A definitive verdict on accountability and corporate survival

The endless cycle of fines and public apologies has proven entirely ineffective at changing corporate behavior. We must recognize that nominal financial penalties are merely viewed as a minor business expense by multi-billion-dollar partnerships. True reform requires structural separation between audit and advisory arms to permanently eliminate the inherent conflicts of interest. Governments must show backbone and ban non-compliant firms from lucrative public contracts, which is the only language these entities truly understand. Because as long as the current system remains intact, the public will continue to bear the massive economic costs of corporate collapses. The time for polite regulatory wrist-slaps is over; structural dismemberment of the Big Four oligopoly is the only viable path forward for global market integrity.