Beyond the Scary Headlines: What Does Real Madrid Debt Actually Mean?

People don't think about this enough: debt in the world of elite football isn't like a credit card balance you can't pay off; it’s more like a strategic mortgage for a palace. When the club reports its finances, they tend to separate "operating debt" from "infrastructure debt." It makes sense, right? If I buy a 100 million euro player, I need that cash now, but if I rebuild a stadium to host Taylor Swift concerts and NBA games, I’m building a money-printing machine for the next thirty years. That changes everything because it shifts the focus from "how much do they owe?" to "how easily can they pay it back?"

The Concept of Net Financial Debt

Where it gets tricky is the definition of net debt. For the 2024/25 fiscal year, Real Madrid reported a net debt of 11.7 million euros. Honestly, for a club with 1.185 billion euros in annual revenue, that is basically the loose change found between the sofa cushions. This "net" figure is calculated by taking their gross financial obligations and subtracting the cash they have in the bank. Because the club maintains a healthy liquidity reserve—around 166 million euros as of mid-2025—the net figure stays low. But—and this is a big "but"—this calculation conveniently leaves out the massive loans taken for the stadium.

Gross Liabilities vs. Operating Liquidity

The issue remains that the total liabilities are hovering around the 1.78 billion euro mark if you include every pending invoice, tax obligation, and stadium loan installment. Is that a problem? Not necessarily. As long as the club's EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) stays high—it hit a record 243 million euros recently—banks are more than happy to keep the credit lines open. Yet, we saw a slight liquidity crunch in late 2025 where cash reserves dipped to 3.4 million euros momentarily. It was a "point in time" dip that caused a minor panic in the Spanish press, but most experts agree it was just a result of aggressive treasury management rather than a sign of actual insolvency.

The Great Bernabeu Gamble: Financing the 1.5 Billion Euro Renovation

The renovation of the Santiago Bernabéu is the elephant in the room, and it’s a very expensive elephant. Originally, the club secured a 575 million euro loan at a fixed interest rate of 2.5%. That was a steal. But because the world decided to get complicated with a global pandemic and rising material costs, they had to go back to the well. Total investment in the stadium has now climbed past 1.34 billion euros, with some investigative reports suggesting the all-in cost with interest will eventually touch 1.5 billion euros by the time the final brick is polished in 2026.

Loan Structures and Annual Repayments

Florentino Pérez didn't just walk into a bank and ask for a billion euros; he structured these loans to be repaid over 25 to 30 years. As a result: the annual debt service is roughly 29.5 million euros. When you consider that the "new" Bernabéu is projected to generate an additional 150 to 200 million euros in annual revenue from non-football events, the debt starts to look like a bargain. It’s the classic "spend money to make money" trope, except the stakes are the future of the world's most successful sports franchise. And because the interest rates were locked in before the recent global inflation spikes, Real Madrid is actually paying back these loans with "cheaper" euros today than they borrowed yesterday.

The Risk of Non-Sporting Revenue

But what if the concerts don't come? Or what if the neighborhood associations (who have already complained about noise levels) manage to cap the number of events? This is where the nuance of the debt comes in. If the stadium doesn't perform as a 365-day-a-year venue, that 1.5 billion euro debt becomes a heavy anchor. We're far from it yet, but the club has already faced some legal hurdles regarding acoustic permits for late-night shows. (It's funny how even a billion-euro stadium can be brought to its knees by a few grumpy neighbors with decibel meters.)

Revenue Records vs. The Growing Wage Bill: A Balancing Act

While the stadium debt is long-term, the day-to-day debt—mostly player wages and transfer amortizations—is what usually sinks clubs like Barcelona or Juventus. Real Madrid has been incredibly disciplined here, keeping their wage-to-revenue ratio at 43%. That is significantly lower than the 70% threshold recommended by UEFA. However, the arrival of superstars like Kylian Mbappé and the constant renewal of young talents like Vinícius Júnior means the salary mass jumped by 26.2% in the 2025/26 season.

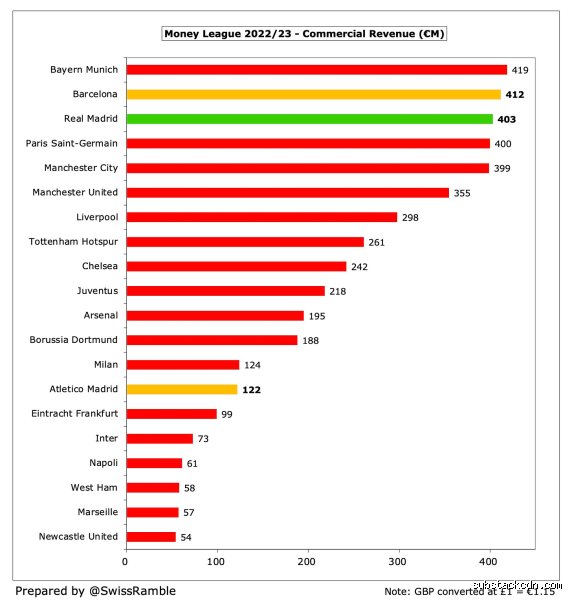

Maintaining the Top Spot in the Deloitte Money League

Success on the pitch is the ultimate hedge against debt. In 2025, Real Madrid reclaimed the top spot in the Deloitte Football Money League, becoming the first club to surpass 1 billion euros in revenue without even counting player sales. This massive income stream allows them to carry debt that would crush a smaller club. Which explains why they aren't selling their best players to balance the books; they don't have to. The commercial engine—merchandise, sponsorships, and the new "Socio" membership tiers—is currently outpacing the interest payments on their loans.

The Hidden Costs of Success

And then there is the FIFA Club World Cup and the expanded Champions League format. These tournaments bring in more cash, yes, but they also require a deeper, more expensive squad. Real Madrid's strategy involves drawing on credit lines—they have about 475 million euros in untapped credit—to bridge the gap between tournament payouts. It's a high-wire act. If they ever have a "down" year where they exit the Champions League early, the working capital deficit (which reached 406 million euros recently) could stop being a technicality and start being a headache.

How Madrid’s Debt Compares to the Rest of the European Elite

To understand if Real Madrid's debt is "bad," you have to look at the neighbors. Barcelona’s debt has been the stuff of nightmares, involving "financial levers" and selling off future TV rights just to register players. In contrast, Real Madrid’s debt is almost entirely investment-grade. They haven't sold their soul; they've just mortgaged the house to build a better garage. Manchester United and Tottenham also carry massive debts (Tottenham’s stadium debt is over 1 billion pounds), so in the context of the "Big Six" and the European giants, Madrid is actually in a position of relative strength.

The "Socio" Model Protection

Unlike Manchester City or PSG, Real Madrid cannot rely on a sovereign wealth fund to write a check and wipe out the debt. They are owned by their members (Socios). This means they have to be more careful, but it also gives them a unique protection. Because they aren't trying to pay out dividends to shareholders, every euro of profit goes back into servicing the debt or buying players. It’s a self-sustaining loop that, so far, hasn’t skipped a beat despite the billion-euro construction project looming over the city of Madrid.

Common misconceptions regarding the white house accounts

The problem is that fans often conflate different types of financial obligations, leading to the erroneous belief that Real Madrid is drowning in red ink. We must distinguish between operational liabilities and long-term structural investment. When you hear that the club carries a gross debt exceeding 600 million Euros, it sounds apocalyptic. However, this figure includes player transfer installments and trade payables which are standard industry practice for any global entity. People assume a high debt-to-equity ratio signals impending doom, yet for a member-owned club, the logic shifts entirely. Unlike a PLC, Real Madrid CF does not pay dividends to shareholders, meaning every cent of surplus stays within the sporting ecosystem. But does this mean they are untouchable? Not exactly. Most casual observers ignore the nuance of deferred tax liabilities, which can fluctuate based on Spanish fiscal policy. As a result: the terrifying headlines often ignore the massive cash reserves sitting in the bank, which as of the last fiscal year sat comfortably around 128 million Euros. Let's be clear, the club is not "broke" just because it owes money to construction firms or other teams. It is a matter of liquidity management versus insolvency. Which explains why Florentino Perez remains remarkably calm during transfer windows despite the astronomical figures being tossed around.

The stadium loan vs. sporting debt

One massive mistake is viewing the Santiago Bernabeu renovation loan as a drain on the club's ability to buy players. Because the loan was structured over 30 years with fixed interest rates as low as 1.53%, the annual repayment is almost negligible compared to the total revenue. Yet, critics scream about the 1.17 billion Euro total cost. The issue remains that this is ring-fenced debt, specifically designed to be paid off by the incremental income the new stadium generates. It is a self-financing loop. In short, the stadium debt is an asset-backed investment, whereas sporting debt—buying a striker who fails to perform—is the real poison that kills balance sheets. If the stadium produces an extra 150 million Euros annually, the debt ceases to be a burden and becomes a profit engine.

Net debt vs. Gross debt confusion

Why do analysts keep arguing over "Is Real Madrid in any debt?" when the numbers are public? The confusion stems from the Net Debt calculation, which recently turned negative in some reporting cycles. This happens when liquid assets and receivables from other clubs outweigh the immediate financial liabilities. You see, a club can have high gross debt but be "debt-free" in net terms. It is a beautiful accounting sleight of hand. Except that it requires consistent Champions League revenue to maintain. If the team crashed out of the group stages for three years straight, that negative net debt would evaporate faster than a summer rain in Castile.

The overlooked genius of the "Socio" model as a financial shield

The most fascinating, yet under-discussed aspect of the club's financial health is its status as a non-profit sports association. We often forget that Real Madrid is owned by its 90,000 members, the Socios. This structure prevents hostile takeovers and, more importantly, it forces a level of fiscal discipline mandated by the Spanish Sports Law. If the board incurs massive losses, they are personally liable to guarantee those losses with their own wealth (a hefty 15% of the budget). Can you imagine a billionaire owner in the Premier League being forced to pay for a bad season out of his own pocket? It creates a unique environment where risk is calculated with surgical precision. (The irony of this is that it makes Perez more conservative than his "Galactico" reputation suggests). Financial sustainability is not just a goal here; it is a legal requirement for survival. As a result: the club has mastered the art of "pre-debt," securing lines of credit before they are needed to ensure they never face a liquidity crunch during economic downturns. This expert-level maneuvering allows them to maintain a credit rating that most sovereign nations would envy. Any expert will tell you that the real secret isn't just making money, it is the cost of borrowing that money, and Madrid borrows cheaper than anyone else in football.

The hidden value of the brand equity

Beyond the spreadsheets, the intangible assets of the club act as a secondary insurance policy. The brand is valued at approximately 1.5 billion Euros, which allows for favorable refinancing terms whenever the market shifts. While other clubs struggle with predatory interest rates, Madrid treats debt as a strategic tool. The issue remains that the club's commercial revenue—reaching 330 million Euros in recent cycles—is the ultimate collateral. It is a fortress built on history, but reinforced by modern corporate strategy.

Frequently Asked Questions

Is Real Madrid in any debt compared to Barcelona?

The disparity between the two Spanish giants is staggering when you look at the structural health of their finances. While Barcelona struggled with short-term high-interest debt that forced them to sell off future media rights (the famous "levers"), Real Madrid maintained a long-term profile with manageable interest. Madrid's net debt has hovered near zero or even turned negative in recent reports, whereas Barcelona's climbed toward 1.35 billion Euros at its peak. The Merengues capitalized on their EBITDA of 158 million Euros to ensure that they never had to compromise their future ownership of assets. Consequently, the capital city club is in a significantly more robust position, enjoying a solvency ratio that allows for aggressive market moves without risking bankruptcy. Because of this, the comparison is almost unfair from a purely accounting perspective.

What happens if the club cannot pay the Bernabeu loans?

Failure to meet these obligations is highly improbable given the diversification of revenue the club has pursued. The loans are secured against the stadium's future income, meaning the bank's primary recourse is the cash flow from the venue itself. Even in a catastrophic scenario, the club's annual turnover of over 800 million Euros provides a massive buffer. However, the loan covenants are strictly monitored by the creditors to ensure the club maintains certain financial ratios. If a default occurred, it would likely trigger a restructuring agreement rather than a liquidation of assets. But let's be honest: with the stadium now hosting concerts and NFL games, the income streams are far more reliable than ticket sales alone.

Does the signing of superstars like Mbappe increase the debt?

Signing a marquee player usually involves a massive signing bonus, but it rarely translates into traditional "bank debt" for Real Madrid CF. Instead, these costs are amortized over the length of the contract, spreading the financial impact across several fiscal years. The club utilizes its cash on hand—which was 128 million Euros in the last audit—to fund these operations rather than taking out new high-interest loans. Furthermore, the commercial upside from jersey sales, sponsorship increments, and social media reach often offsets the wage bill within the first 24 months. The issue remains that the wage-to-revenue ratio must stay below 70% to comply with UEFA's financial sustainability regulations. Madrid currently operates well below this threshold, typically around 54%, leaving plenty of room for "Galactico" expenditures without deforming the balance sheet.

Toward a new era of financial dominance

The verdict is clear: Real Madrid utilizes debt not as a desperate lifeline, but as a sophisticated weapon for capital expansion. We see a club that has successfully transitioned from a mere sports team to a diversified entertainment conglomerate. The issue remains that the football world views "debt" as a dirty word, yet in the boardroom, it is the fuel for the 15th, 16th, and 17th Champions League trophies. Let's be clear, the financial stability of this institution is currently the benchmark for the entire industry. I firmly believe that their monolithic revenue model will eventually make them the first club to consistently cross the 1-billion-Euro annual revenue mark without state-ownership. It is a masterclass in capitalist sport. As a result: the answer to the question "Is Real Madrid in any debt?" is a resounding "Yes," but it is the kind of debt that makes them richer every single day.