Beyond the Myth of the Naive Elder: Redefining Fraud Demographics

For a long time, the public imagination has been captured by the image of the isolated senior citizen wire-transferring their life savings to a fake lottery official in Jamaica. But where it gets tricky is looking at the sheer volume of incidents recorded by regulatory bodies like the Federal Trade Commission (FTC). The reality is that digital ubiquity has democratized vulnerability. Young people buy fast-fashion off sketchy Instagram ads, invest in highly speculative meme coins via unverified Telegram channels, and fall for peer-to-peer payment traps on apps like Zelle or Venmo without a second thought. They are online constantly, which explains why their exposure rate is astronomically higher than any other demographic.

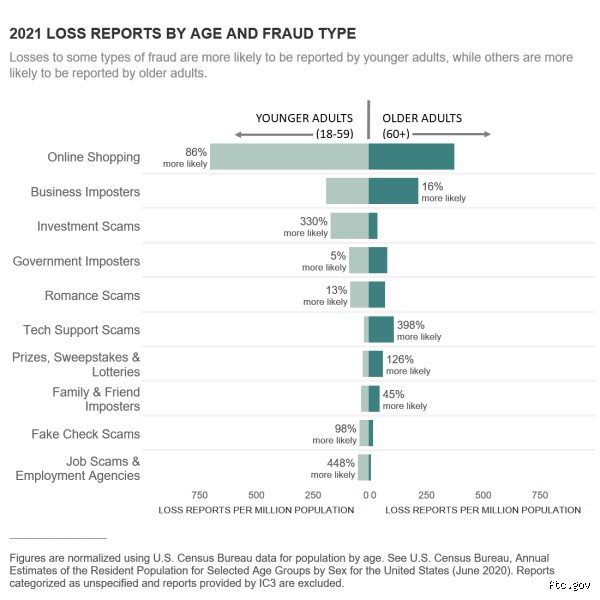

The Statistical Paradox of Age and Total Loss

Let us look at the numbers because people don't think about this enough. According to FTC data tracking consumer reports, adults under 30 report losing money to scams far more often than their grandparents, yet the median loss for a 20-year-old hovering around $500 looks like pocket change compared to the devastating median loss of $1,500 reported by victims over the age of 80. It is a volume versus value play. Young adults get stung frequently for smaller amounts—a fake concert ticket here, a fraudulent sneaker drop there—which changes everything when analyzing societal impact. But the issue remains that older demographics possess the actual wealth, making them the white whales for high-tier transnational syndicates using sophisticated pig butchering scams or elaborate imposter schemes.

Psychological Triggers That Defy Intellectual Immunity

Why do smart people swallow obvious bait? Because fraud is never an intellectual test; it is an emotional hijack. I used to believe that basic digital literacy was enough to protect someone, but honestly, it's unclear if education matters at all when cognitive load is high. Scammers do not target your ignorance; they weaponize your urgency, your loneliness, or your desperate need to pay off student debt. When a phishing email hits your inbox at 4:45 PM on a Friday claiming your bank account has been frozen due to suspicious activity in Romania, your critical thinking centers don't just slow down—they completely disconnect.

The Mechanics of Modern Manipulation and Digital Traps

Fraud has evolved from poorly spelled Nigerian Prince emails into highly industrialized corporate enterprises operating out of Southeast Asian compounds. These are not lone hackers in hoodies. We are talking about organized entities using advanced social engineering playbooks, standardized scripts, and custom-built customer relationship management software to track their marks. The sophistication is terrifyingly corporate.

The Rise of App-Based Financial Predators

The structural shift toward instant, irreversible payment mechanisms has created a goldmine for predatory actors. In the past, a bank wire took days to clear, providing a crucial window for intervention, except that today's Authorized Push Payment (APP) fraud relies on instantaneous peer-to-peer networks. Consider the case of a tech-savvy freelance designer in Austin who lost $4,000 in April 2025 through a spoofed bank representative scam; the perpetrator guided them to use a major bank app to transfer funds to "safety" in real-time. Once you hit send on those platforms, the money vanishes into a web of mule accounts before the victim even finishes hanging up the phone.

Employment and Cryptocurrency Honey Pots

Economic anxiety has birthed a massive surge in fake job postings on reputable platforms like LinkedIn and Indeed. Young job seekers, desperate for remote work, are onboarded by ghost companies, sent counterfeit checks for home-office equipment, and told to wire the surplus back to a "vendor." By the time the bank flags the original check as fraudulent, the victim owes thousands. Meanwhile, the crypto space operates like the Wild West. High-yield investment programs leverage deepfake videos of tech billionaires to siphon millions from retail investors who believe they are getting in on the ground floor of the next financial revolution. But the truth is simpler: they are feeding an insatiable meat grinder.

Analyzing Vulnerability Through Socioeconomic Lenses

Who gets scammed the most isn't just a question of birth years; it is inextricably tied to financial security and systemic pressures. Wealthier individuals are targeted for their assets through bespoke spear-phishing attacks, while lower-income communities face relentless volume attacks designed to extract their last hundred dollars. The predatory ecosystem adapts perfectly to the financial desperation of its prey.

Desperation as an Accelerator for Deception

When you are living paycheck to paycheck, a message offering a guaranteed government grant or a quick-turnaround loan isn't an obvious red flag—it looks like a lifeline. This specific vulnerability is exploited by predatory advance-fee loan operators who demand an upfront processing fee via gift cards or cryptocurrency before disappearing. It is a cruel irony that those who can least afford to lose a dime are the ones subjected to the highest frequency of these aggressive, low-level financial assaults. Experts disagree on whether regulatory crackdowns can ever outpace this kind of hyper-localized, adaptive fraud, but the systemic damage is undeniable.

How Identity Theft Categorically Targets Different Life Stages

We must separate the immediate, active scams from the long-term, passive exploitation of personal data. Identity theft manifests differently depending on where you sit in the life cycle, hitting both ends of the spectrum with equal malice.

The Untapped Clean Slate of Child Identity Fraud

Think your toddler is safe from cybercriminals? You are far from it. Synthetic identity theft often targets minors because their Social Security numbers are completely clean slates with no credit history attached. A criminal syndicate can hijack a child's identifier, pair it with a fake birth date and address, and build a pristine credit profile over a decade, racking up massive debts without anyone noticing until that teenager applies for their first student loan. It is a silent, invisible crime that gestates for years in the dark corners of the web, proving that lack of an online presence offers zero absolute protection against structural exploitation.

Common mistakes regarding who gets scammed the most

Society loves a convenient scapegoat, so we collectively agreed that Grandpa is the definitive target. This assumption is comforting because it isolates the risk to a specific, supposedly frail demographic. Except that the data relentlessly shatters this myth. Younger digital natives collapse under financial fraud far more frequently than their retired counterparts. While octogenarians lose larger individual sums due to accumulated life savings, the sheer volume of incidents overwhelmingly skews toward tech-savvy internet users aged 20 to 39.

The illusion of digital immunity

Growing up with a smartphone in hand creates a dangerous, unearned sense of security. You assume that because you know how to navigate a decentralized crypto exchange or spot a poorly rendered deepfake, you are impervious to deception. The problem is that fraudsters do not rely on technical illiteracy; they exploit emotional vulnerabilities. Social engineering adapts instantly to current cultural trends, catching younger cohorts off guard through hyper-targeted Instagram advertisements or fraudulent peer-to-peer payment requests. In fact, recent consumer protection agency analyses revealed that adults under 30 are 34% more likely to report losing money to online trickery than older generations.

The wealth bias misconception

Another profound error lies in assuming that criminals only hunt where the coffers are overflowing. Logically, you would expect high-net-worth individuals to top the list of who gets scammed the most. Yet, predatory systems thrive on desperation, not just abundance. Employment scams, fake rental listings, and predatory fee-advance schemes specifically drain resources from those who can least afford it. A bank account hovering near zero represents the perfect breeding ground for a fraudulent "get-rich-quick" lifeline. Socioeconomic vulnerability accelerates victimization rates, turning marginal financial stability into total ruin overnight.

The psychological blind spot: Overconfidence as a catalyst

Why do highly educated professionals routinely fall for obvious trapdoors? It turns out that cognitive superiority serves as an excellent accelerator for deception. When a specialized corporate attorney or a senior software engineer looks in the mirror, they see someone completely incapable of being hoodwinked. ( we all like to believe we are the smartest person in the room, don't we? )

The weaponization of professional authority

Con artists understand that breaking down a sophisticated target requires bypassing intellect entirely and striking directly at ego or fear. They craft scenarios involving regulatory audits, impending professional disgrace, or exclusive, time-sensitive investment windows. Because the victim relies heavily on their own analytical prowess, they spend their energy rationalizing the red flags instead of halting the transaction. As a result: the highly credentialed expert walks themselves straight into the trap, convinced they are merely navigating a complex, high-stakes business scenario. Intellectual arrogance silences the instinctual alarm bells that a more cautious, self-aware individual might actually heed.

Frequently Asked Questions

Which age demographic actually loses the highest total volume of money to fraudsters?

While younger individuals report a higher frequency of incidents, older adults endure the most devastating financial impact. Empirical data from global trade commissions indicates that victims over the age of 70 suffer a median loss of approximately 800 dollars per event. This is drastically higher than the 300 dollars median loss experienced by younger cohorts. Criminals deliberately deploy romance scams and intricate lottery hoaxes against isolated retirees to systematically drain retirement portfolios. Consequently, older demographics remain the definitive answer regarding who gets scammed the most in terms of sheer economic devastation.

How does psychological state influence an individual's susceptibility to fraudulent schemes?

Isolation and cognitive overload act as massive force multipliers for deceptive tactics. When a person experiences profound loneliness or severe burnout, their neurological capacity to evaluate risk plummets dramatically. Scammers explicitly design high-pressure scripts that induce panic, such as threatening immediate arrest by tax authorities or implying a bank account compromise. Under intense emotional duress, the prefrontal cortex struggles to process logical inconsistencies, making the victim highly compliant. Chronic stress completely obliterates our natural defense mechanisms against manipulative behavior.

Are certain personality traits directly linked to a higher probability of victimization?

Psychological profiling reveals that high levels of openness to experience, combined with an impulsive decision-making style, create a precarious vulnerability profile. Individuals who pride themselves on being adventurous often embrace unverified opportunities without conducting due diligence. But the issue remains that compliance traits, specifically the systemic inability to say no to an authority figure, also drive these statistics upward. Culturally conditioned politeness prevents many targets from abruptly hanging up the phone or deleting a suspicious message. Ultimately, the perfect target isn't unintelligent; they are simply excessively trusting and easily hurried.

A radical reframing of modern vulnerability

We must discard the patronizing narrative that fraud is exclusively a tax on the elderly or the uneducated. The unsettling truth is that everyone occupies the target demographic depending on the day, the hour, and the specific emotional vulnerability being exploited. Consumer protection frameworks remain outdated because they focus on teaching people how to spot technical anomalies rather than managing psychological triggers. Fraud is an industrialized, multi-billion-dollar psychological warfare operation that adapts faster than any corporate firewall. Until we acknowledge our collective susceptibility, the cycle of victimization will continue its aggressive upward trajectory. Stop looking down your nose at the victims, because your own specialized blind spot is already being mapped by a criminal enterprise.