The Evolution of Modern App-to-Bank Vulnerabilities

The tech landscape has shifted underneath our feet. We used to worry about sketchy desktop downloads, but today, your smartphone is the primary target because it consolidates your entire financial existence into a single, pocket-sized glass slab. People don't think about this enough.

The Blur Between Socializing and Banking

WhatsApp was never designed to be a vault, yet it has become the default operating system for our daily interactions, including, increasingly, our financial transactions. In places like Brazil and India, millions of citizens use WhatsApp Pay to settle bills directly within the chat interface, which changes everything because it creates a direct API bridge between a casual messaging ecosystem and core banking infrastructure. When you mix emojis with financial routing numbers, the psychological barrier to entry drops significantly, leaving users vulnerable to catastrophic oversights that no legacy firewall can prevent.

Why Modern Hackers Shifted From Code to Psychology

Let's be blunt: modern banking apps are incredibly tough to crack directly from the outside. Financial institutions spend billions on end-to-end encryption and multi-factor authentication, making a direct brute-force attack on a bank server almost entirely unprofitable for routine cybercriminals. So, where it gets tricky is the human element. Why waste three months trying to exploit a hardened banking mainframe when you can spend three minutes convincing a distracted parent on WhatsApp that their daughter needs an emergency wire transfer to fix a broken phone? The chat app becomes the delivery vector, the mechanism by which the human firewall is systematically dismantled.

The Anatomy of a WhatsApp Financial Heist

How does this actually play out in the wild? It is rarely a cinematic explosion of green code across a monitor; instead, it is a slow, methodical manipulation of trust, device permissions, and architectural loopholes.

The Hijacked Session Token Nightmare

The most sophisticated attack method does not even require your bank password. In a chilling case documented by cybersecurity researchers in Berlin in October 2025, attackers utilized malicious WhatsApp Web QR codes—a tactic known as QRLjacking—to mirror users' active sessions onto remote servers. Once the attackers gained control of the WhatsApp account, they intercepted the one-time passwords (OTPs) transmitted via chat by automated banking bots. But how do they bypass the official banking app's biometric lock? Simple: they don't have to if they can use the intercepted identity to initiate a web-based password reset through the bank's customer service portal, using the compromised WhatsApp account as proof of life.

Malicious Media Payloads and Zero-Day Exploits

This is where the tech gets genuinely frightening. While WhatsApp patches vulnerabilities rapidly, zero-day exploits—unpatched flaws bought and sold on the dark web for millions of dollars—can allow attackers to execute code remotely. Remember the infamous Pegasus spyware incident? A similar vector was observed in early 2026, where a specially crafted .mp4 video file sent via WhatsApp could trigger a buffer overflow vulnerability on older Android operating systems. Once the user clicks play, the malware silently installs a hidden keylogger in the background, which waits patiently until you open your Chase or Barclays app to log in, capturing every keystroke and sending your credentials directly to a command-and-control server in Eastern Europe.

The Danger of Compromised Backup Files

The issue remains that while your live chats are encrypted, your cloud backups might not be. If a hacker gains access to your Google Drive or iCloud account through a completely unrelated phishing scam, they can download your unencrypted WhatsApp chat history. If you have ever texted your credit card details, a photo of your driver's license, or your banking PIN to your spouse for convenience—a habit that roughly 34% of smartphone users admit to doing—you have effectively handed over the keys to your kingdom on a silver platter.

The Deceptive Psychology of Conversational Engineering

We need to talk about the sheer brilliance of the psychological traps being laid here. Honestly, it's unclear why more people haven't realized that the threat isn't just technical; it's deeply emotional.

The "Hi Mum" Fraud and Institutional Spoofing

In 2024, UK citizens lost a staggering £10.5 million to the "Hi Mum" scam alone, a fraud format that has now evolved using deepfake audio technology. You receive a text from an unknown number claiming to be your child who lost their phone. The conversational cadence is identical to your child's because the scammers scraped their public Instagram videos to train an AI voice model. They send a voice note via WhatsApp asking for an urgent bank transfer to pay an overdue bill. You comply because panic overrides cognitive defense mechanisms. Is that a technical hack of your bank account? No, yet the financial damage is absolutely identical to someone cracking your online banking portal.

The Malicious Employee Impersonation Trap

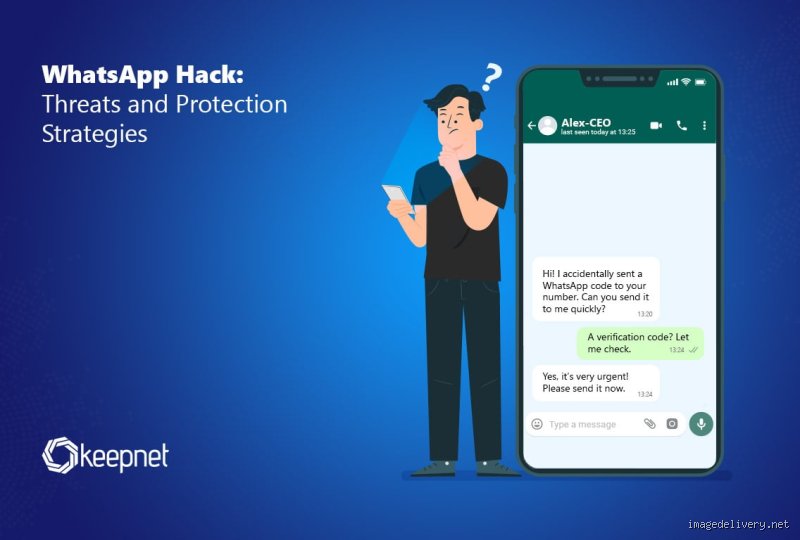

Another variant involves scammers posing as official customer service representatives from major institutions like HSBC or Bank of America. They target users who have posted complaints on public forums like X (formerly Twitter), moving the conversation to WhatsApp under the guise of offering "secure, personalized assistance." They walk the victim through a series of "security verifications," which actually consist of the victim unwittingly reading aloud the two-factor authentication codes arriving on their screen. By the time the chat session is terminated, the victim's savings have been completely liquidated via instant wire transfers.

How WhatsApp Financial Risk Profiles Compare to Traditional SMS

Many industry commentators argue that switching entirely to WhatsApp for banking notifications is safer than relying on traditional cellular networks, but we are far from a consensus on that assertion.

The Hidden Fragility of End-to-End Encryption

Security advocates love to champion end-to-end encryption as the ultimate shield. Yet, this focus on encryption during transit creates a dangerous false sense of security, except that it does absolutely nothing to protect the data once it rests on an endpoint device that has already been compromised by malware. If a bad actor has root access to your device, they are reading the messages right off your screen alongside you. Traditional SMS is notoriously vulnerable to SIM-swapping attacks—where a hacker convinces a telecom carrier to port your number to a new SIM card—but WhatsApp is uniquely vulnerable to account takeovers via device linking, where up to four companion devices can be attached to a single account simultaneously, often without the primary user noticing immediately.

The Dangerous Illusion of the Verified Green Checkmark

Banks often point to the green verification badge on WhatsApp as proof of absolute security. However, the black market for compromised verified business accounts has boomed over the last eighteen months. Sophisticated syndicates buy legitimate, aging business accounts with green checkmarks or use shell corporations to acquire them legally, only to later pivot those accounts toward phishing campaigns. When an official-looking account with a verified badge messages you saying your account has been frozen, your natural instinct is to trust it completely, which explains why these specific attacks boast an incredibly high success rate compared to standard email phishing.

Common misconceptions about instant messaging banking risks

The myth of the omnipotent application

Many users blindly believe that merely opening a text chat can drain a checking account. This is pure fantasy. WhatsApp itself operates within a sandboxed environment on your smartphone, meaning its code cannot freely wander into your banking application to alter balances. The problem is that people confuse social engineering with direct technical infiltration. A hacker does not magically break the encryption of Meta; instead, they exploit the human operating the device. Except that when a user voluntarily hands over a two-factor authentication code to a spoofed profile, the sandbox cannot protect them. But let's be clear: a text message is just data. It cannot execute code on your device without your active, albeit tricked, cooperation.

The false security of end-to-end encryption

Another dangerous trap is assuming that because your messages are encrypted, your money is safe. Encryption prevents outsiders from intercepting your chat logs in transit. Yet, it does absolutely nothing if the person on the other end of the conversation is an imposter pretending to be your son, daughter, or financial adviser. If a malicious actor compromises your device via a malicious PDF link sent through a chat, the secure tunnel is irrelevant. Can your bank account be hacked through WhatsApp? Not via the encrypted tunnel itself, but certainly through the psychological manipulation that occurs within it. Security protocols protect data in motion, not the gullibility of the recipient.

Misunderstanding WhatsApp Web vulnerabilities

Users frequently assume their desktop computer is a fortress compared to their phone. In reality, leaving a WhatsApp Web session active on a shared or poorly secured computer opens a massive back door. A malicious actor with brief physical access can scan your QR code, mirror your conversations, and intercept bank notifications. Session hijacking represents a massive vulnerability because it bypasses biometric checks. Once inside your desktop interface, scammers observe your habits, wait for a banking interaction, and strike when you least expect it.

The hidden vector: SIM swapping and configuration files

The silent interception of configuration payloads

Let us look at a sophisticated mechanism that security researchers rarely discuss openly. Attackers sometimes utilize modified configuration files disguised as innocent media downloads to exploit unpatched media libraries within messaging applications. When the app attempts to parse a corrupted video file, a buffer overflow can occur, allowing remote code execution. At this point, the attacker gains access to your phone's storage, where they can search for poorly encrypted backup files or plain-text notes containing passwords. Device mirroring via exploit payloads is rare, but for high-net-worth individuals, it remains a potent threat vector that bypasses traditional anti-virus solutions.

The devastating reality of SIM swap duplication

How does a simple chat app lead to an empty savings account? The answer lies in your phone number. By using targeted phishing via chat messages, criminals gather your full name, date of birth, and mother's maiden name. Armed with this dossier, they trick your mobile carrier into porting your number to a new SIM card. Instantly, your WhatsApp account activates on the hacker's device, giving them access to your group chats and, more importantly, your bank's SMS verification codes. Why do banks still rely on SMS for high-value transfers when it is so inherently flawed? It is a question of convenience over security, which explains why thousands of accounts vanish overnight. In short, your chat app becomes the reconnaissance tool that makes the SIM swap possible.

Frequently Asked Questions

Can your bank account be hacked through WhatsApp by simply answering a video call from an unknown number?

No, you cannot lose your life savings merely by answering an incoming video call. While historical zero-day vulnerabilities like the famous Pegasus spyware exploit have utilized missed calls to inject code, these are highly targeted state-sponsored tools rather than tools for broad financial fraud. According to global cybersecurity reports from 2025, over 94 percent of successful mobile banking thefts required the victim to download a file or click a link after the call. The call itself serves as a psychological grooming mechanism to build false trust or create a sense of extreme urgency. Do not panic if you accidentally answer an unknown contact; just refuse to download external software or provide security codes. The danger begins only when you move from passive listening to active compliance with the scammer's demands.

What should you do immediately if you realize you shared your banking credentials via a WhatsApp chat?

You must act within minutes because speed is the only barrier to asset liquidation. First, call your financial institution's emergency fraud hotline to freeze all digital banking access and debit cards instantly. Next, revoke all active sessions on your messaging app by navigating to the linked devices menu and logging out of every terminal. You should also change your digital banking passwords from a completely different, clean device to ensure no active keyloggers are monitoring your inputs. Did you know that banks can often reverse fraudulent wire transfers if notified within the first two hours? Waiting until the next morning to report the incident almost guarantees the total loss of your funds, as international laundering networks move stolen money through multiple cryptocurrency layers instantly.

Can hackers use WhatsApp automated bots to empty a user's savings account without their knowledge?

Automated bots cannot autonomously breach a banking app, but they can dramatically accelerate the phishing pipeline. Criminals deploy automated scripts that send thousands of identical, deceptive messages per second pretending to be automated fraud alerts from major institutions. These bots handle the initial conversation, collect your account details via automated forms, and then instantly pass the stolen data to a human attacker who executes the theft. Data from recent financial cybercrime audits shows that automated phishing bots reduced attack execution times from days to under eleven minutes. The issue remains that the bot is merely an efficiency tool; it still requires you to type your credentials or authorize a push notification. Without that initial slip of vigilance, the bot is completely powerless against your accounts.

An honest assessment of mobile messaging security

We must abandon the comforting illusion that our digital wallets are disconnected from our social applications. The reality is stark: your smartphone is a single, interconnected ecosystem where a breach in one corner inevitably compromises the rest. Can your bank account be hacked through WhatsApp? The technical answer is no, but the practical, real-world answer is an absolute, undeniable yes. We place too much faith in software patches while ignoring our own cognitive vulnerabilities. If you continue to treat your messaging inbox as a zone of casual trust, you are practically inviting financial ruin. True security demands an attitude of permanent skepticism toward every unverified link, urgent request, and strange file attachment. Stop looking for a silver-bullet app to save you; your own discipline is the ultimate firewall.