The Global Power Grid: Separating Hype From Hard Factory Output

People don't think about this enough, but making a brilliant battery in a university laboratory means absolutely nothing to the automotive world. The true metric of dominance is gigawatt-hours deployed on real roads under grueling real-world conditions. According to recent data from SNE Research, the global EV battery usage reached 1,187 GWh in 2025, signaling a massive 31.7% year-on-year market expansion. Within this hyper-competitive landscape, a singular Chinese powerhouse has effectively decoupled itself from the rest of the pack.

The Statistical Fortress of Ningde

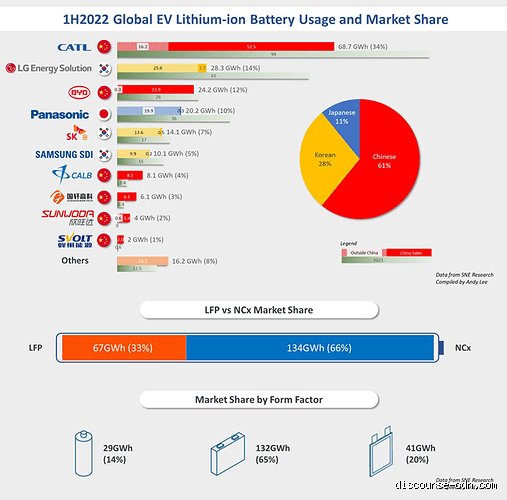

Let's look at the raw numbers because they are frankly terrifying for Western carmakers. CATL alone installed 464.7 GWh of capacity globally over the past year. To put that in perspective, their closest competitor, BYD, captured 16.4% of the market with 194.8 GWh. Everyone else is playing a game of minor percentages; legacy giants like South Korea's LG Energy Solution sit at a distant 9.2%, while Japan's Panasonic has hovered around 3.7%. I believe we are witnessing a permanent structural monopoly, not a temporary market trend. The sheer capital required to match this scale creates an insurmountable barrier to entry.

The Chinese Domestic Ecosystem Duopoly

Where it gets tricky is inside the Chinese domestic market itself, which acts as the incubator for global automotive trends. Together, CATL and BYD control over 64% of China's domestic battery installations. This massive domestic demand provides a steady stream of revenue that funds their massive research budgets. It allows them to iterate generation after generation of cell design while Western startups are still struggling to fund their initial pilot lines. Except that this isn't just a story about building massive factories; it is a story about relentless, aggressive chemical engineering.

Beyond Lithium-Ion: The Structural Revolution in Cathodes and Anodes

For a decade, the automotive industry assumed that ternary nickel-manganese-cobalt cells would always reign supreme due to their high energy density. That changes everything when cost becomes the only metric that matters to mass-market consumers. Chinese manufacturers realized early on that lithium iron phosphate chemistry, despite its lower nominal energy density, was the key to unlocking affordable mass adoption. LFP batteries accounted for over 55% of EV batteries deployed globally in 2025, a massive shift from being considered a low-end option just a few years ago.

The Blade and the Qilin: Structural Pack Innovations

How did they make cheap, low-energy chemistry viable for long-range vehicles? They bypassed cell-level limitations by reinventing how batteries are packaged inside a car chassis. BYD introduced its iconic Blade Battery, utilizing long, sword-like cells that act as structural members of the pack itself to eliminate heavy modules. Not to be outdone, CATL pushed back with its third-generation Qilin Battery architecture. By utilizing advanced cell-to-pack engineering, CATL achieved a volume utilization efficiency of 72%, allowing an LFP pack to deliver range numbers that previously required expensive nickel.

The Silicon-Carbon Anode Transition

But the real chemical wizardry is happening at the anode. Traditional graphite anodes are reaching their theoretical physical limits, forcing engineers to integrate silicon-carbon composites. BYD's latest second-generation Blade variations utilize these advanced anodes alongside lithium manganese iron phosphate cathodes. This engineering leap pushes system-level energy densities consistently past 160 Wh/kg. It is a brilliant compromise: you get the safety and low cost of iron-based chemistry, but with a driving range that satisfies anxious suburban drivers.

The Holy Grail: Who Wins the Solid-State Race?

Every major legacy automaker, from Toyota to Volkswagen, has spent the last five years pinning their long-term survival on the promise of all-solid-state batteries. The conventional wisdom was that Western and Japanese brands would use solid-state technology to leapfrog China's dominant liquid-electrolyte manufacturing base. The issue remains that China's battery giants are refusing to let that happen. Honestly, it's unclear who will cross the commercial finish line first, but the timeline is moving much faster than experts originally predicted.

CATL's Sulfide-Based Timeline

In early 2026, the World Intellectual Property Organisation published a critical patent revealing CATL's massive breakthroughs in solid sulfide electrolytes. The company has quieted the skeptics by moving past small lab tests to pilot-producing 20-Ah sample cells with an eye-watering energy density of 500 Wh/kg. They are currently at technology maturity level 4, with a hard corporate target to hit automotive-grade level 7 or 8 by 2027. They recently reserved a mind-boggling 626,000 tonnes of specialized copper foil, signaling that they are already preparing their supply chain for massive commercial scaling.

The Mixed Solid-Liquid Compromise Phase

But we are far from seeing purely solid-state cars filling up suburban driveways tomorrow morning because sulfide cells remain three to five times more expensive than traditional packs. Because of these cost barriers, 2026 is emerging as the year of the hybrid solid-liquid battery. SVOLT Energy and SAIC Motor are already preparing to mass-produce 100 kWh hybrid packs for production vehicles. These intermediate steps offer a significant safety boost and improved thermal stability without requiring car companies to completely retool their multi-billion-dollar assembly lines.

The Sodium Disruptor: Cheap Energy Without Lithium

What if the ultimate leader in battery technology isn't the company making the highest-density luxury cell, but the one that frees the world from the volatile lithium supply chain entirely? Sodium-ion technology has quietly transitioned from a laboratory curiosity into a genuine industrial alternative. Sodium is abundant, dirt-cheap, and completely immune to the geopolitical choke points that plague lithium mining. Yet, it suffers from a lower energy density, making it a tough sell for heavy, long-range SUVs.

Mass Production on the Horizon

During their recent Super Tech Day, CATL announced that they had systematically resolved the four primary bottlenecks facing sodium-ion mass production, including ultra-low moisture control and hard carbon gas generation. The company intends to scale up massive production lines by the end of 2026. Proving their immense confidence, they signed a massive three-year, 60 GWh sodium-ion supply agreement with HiTHIUM. Contrast this with the fact that the entire global market for sodium cells was a meager 9 GWh just a year prior. As a result: we are about to see a massive flood of cheap, lithium-free batteries enter the stationary energy storage sector and low-cost urban commuter vehicles.

The Dangerous Blind Spots of the Energy Debate

You probably think the race is all about chemistry. It is easy to get blinded by laboratory breakthroughs and shiny press releases promising thousand-mile ranges. The problem is, scaling a bench-scale miracle into a gigafactory reality is where most ambitious pioneers go to die.

The Myth of the Single Magic Anode

Every week, a new startup claims to have unlocked the ultimate solid-state architecture. We are constantly bombarded with breathless coverage of silicon anodes and lithium-metal breakthroughs. Yet, these laboratory triumphs usually crumble when subjected to the brutal realities of mass production. It is one thing to handcraft a pristine pouch cell for a press conference. It is a completely different nightmare to manufacture millions of them every single day with near-zero defect rates. The true leader in battery technology is not necessarily the outfit with the most patents, but the one that mastered the agonizing poetry of high-speed roll-to-roll manufacturing.

Equating Energy Density with Market Dominance

More watt-hours per kilogram sounds inherently superior, right? Except that the automotive and grid industries care just as much about thermal stability, cycle life, and dollar-per-kilowatt-hour metrics. A hyper-dense cell that catches fire when slightly bruised or degrades after three hundred cycles is functionally useless. Cheap, incredibly durable Lithium Iron Phosphate chemistry currently dominates the global landscape despite its lower energy density. Why? Because economics always trumps pure physics at the dealership.

The Hidden Unfair Advantage: The Slurry Processing Secret

Let's be clear: the grand geopolitical chess match of energy storage is not being won by quantum physicists. It is being won by industrial mixing engineers.

Why Dry Electrode Coating Changes Everything

Traditional manufacturing relies on a toxic, massive, and energy-hogging wet coating process using a solvent called NMP. Tesla spent years tearing its hair out trying to master the dry electrode process for its 4680 cells, proving that the smartest minds find this incredibly difficult. Companies like Maxwell Technologies, which Tesla acquired and absorbed, shifted the paradigm by using polytetrafluoroethylene binders to compress active materials into a free-standing film. The issue remains that missing the mechanical tolerances by a mere micrometer ruins the entire batch. Whichever titan perfectly stabilizes this dry coating process at scale instantly slashes capital expenditure by over thirty percent, completely rewriting the global cost curve.

Frequently Asked Questions

Which country currently controls the vast majority of the global battery supply chain?

China absolute dominates the landscape, commanding roughly seventy-five percent of global cell manufacturing capacity and controlling over ninety percent of the refining for key materials like manganese and cobalt. Contemporary Amperex Technology Co. Limited, or CATL, alone held a massive thirty-seven percent of the global electric vehicle battery market share recently. This staggering consolidation means western automakers are fundamentally reliant on Chinese supply chains despite massive domestic subsidy programs like the American Inflation Reduction Act. But can this stranglehold actually be broken before the decade ends? It requires hundreds of billions of dollars in infrastructure replication, which explains why shifting production geographic centers is moving at a snail's pace.

Will solid-state cells completely replace lithium-ion systems anytime soon?

Solid-state variants will not cannibalize the market overnight, though Toyota keeps teasing a commercial rollout packed with over one thousand kilometers of range and a ten-minute charge time. We will likely see these advanced, expensive solid-electrolyte systems relegated exclusively to premium luxury vehicles and niche aerospace applications until at least the mid-2030s. The traditional liquid-electrolyte lithium-ion cell still has immense room for incremental optimization, maintaining a ferocious cost advantage that will keep it dominant for mass-market vehicles. In short, do not expect your entry-level hatchback to sport a solid-state pack anytime in the near future.

How big of a role will sodium-ion variants play in the future market?

Sodium-ion technology represents a massive geopolitical escape hatch because it completely bypasses the need for scarce, expensive lithium and cobalt by utilizing abundant rock salt. While its lower volumetric energy density makes it poorly suited for long-range premium sports cars, it is absolutely perfect for stationary grid storage and urban micro-mobility. CATL has already deployed first-generation sodium cells boasting energy densities around one hundred and sixty watt-hours per kilogram, proving the tech is commercially viable. As a result: we are about to see a sharp bifurcation where lithium powers the fast-lane while sodium quietly runs our power grids and affordable city commuter cars.

The Verdict on Energy Sovereignty

Stop looking for a single savior crown in this hyper-fragmented ecosystem. If we judge dominance by sheer industrial muscle and ecosystem control, CATL remains the undisputed market frontrunner in advanced energy storage by a terrifying margin. They are not just building cells; they are dictating the economic terms of global electrification. Betting on a dark-horse startup to miraculously dethrone this infrastructure behemoth with a single lab breakthrough is a fool's errand. True leadership belongs to the entities that can turn raw earth into millions of reliable, cheap, safely functioning packs every minute. The crown is firmly forged in the fires of mass production, and right now, East Asia holds the only hammer.