And that’s where things get interesting. Because if you’re asking about PAA’s dividend, you’re probably not just scanning for yield—you’re trying to figure out whether this midstream giant still belongs in a dividend portfolio, or if it’s become something else entirely.

Understanding PAA: What Exactly Is Plains All American Pipeline?

The Core Business: Moving Oil Where It Needs to Go

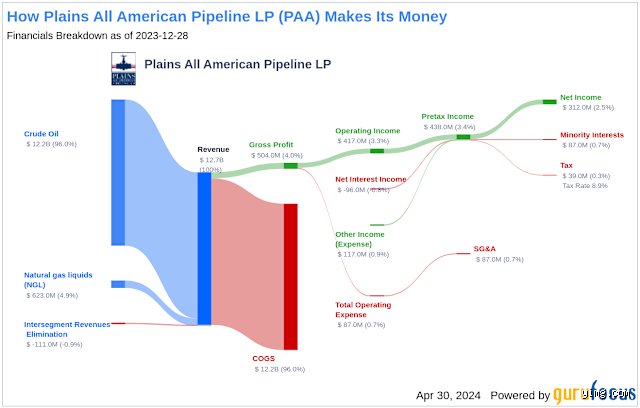

Plains All American Pipeline, trading under the ticker PAA, isn’t in the business of drilling or refining. It’s a midstream operator—think of it as the circulatory system of the oil industry. It gathers crude from wells, transports it via pipelines, stores it, and delivers it to refineries. This separation from exploration risk used to make companies like PAA favorites among conservative energy investors.

Their operations stretch across more than 18,000 miles of pipeline and include 120+ terminals with over 100 million barrels of storage capacity—figures that matter because scale translates to pricing power and resilience during downturns.

MLP Structure: Why It Once Meant Big Distributions

Here’s where it gets technical—and important. PAA was structured as a master limited partnership (MLP), a tax-advantaged entity that’s required to pass most of its cash flow to investors. That’s why, back in the 2010s, yields routinely hovered between 6% and 9%. People flocked to them like bees to syrup.

But MLPs also come with messy tax forms (K-1s, not 1099s), and their distributions aren’t dividends in the traditional sense—they’re return of capital, which complicates tax reporting. Still, for yield-hungry retirees or income funds, the payout was worth the hassle—until it wasn’t.

When the Dividend Stopped: The 2020 Suspension That Changed Everything

The Financial Strain Behind the Decision

Crude prices collapsing to negative $40 a barrel in April 2020? That wasn’t just dramatic—it was catastrophic for midstream cash flows. PAA was carrying around $7 billion in long-term debt and facing covenant risks. And that’s when management made the call: suspend the distribution to preserve liquidity.

They didn’t just trim it—they zeroed it out. The $0.30 per unit quarterly payout, which had already been slashed from over $0.70 in prior years, vanished. Investors took the hit. The stock dropped 40% in two weeks. And no, it wasn’t a surprise to analysts who’d been warning about leverage since 2018.

Restructuring and the Move Away from MLP Status

Then came the bigger shift: in 2023, PAA completed a corporate reorganization, converting from an MLP to a traditional C-corporation. That simplifies taxes for investors—no more K-1s—but it also signals a cultural change. The relentless pressure to distribute cash is gone.

The thing is, C-corps can still pay dividends. But they’re under no obligation to. And right now, PAA’s leadership is prioritizing debt reduction, asset optimization, and reinvestment over shareholder payouts. That’s not a temporary pause. It’s a strategic reprioritization.

Current Investor Returns: If Not Dividends, Then What?

So, no dividend. But that doesn’t mean PAA offers nothing. The stock has returned over 80% in the past three years (2021–2024), outperforming the broader energy sector. That’s capital appreciation, not income—but for total return investors, it’s still a win.

And you know what’s wild? The company generated $1.7 billion in free cash flow in 2023 alone. That could cover a modest dividend. But instead, they used it to cut debt by nearly $1 billion and buy back $400 million in shares. Buybacks aren’t passive income, but they do boost per-share value over time.

Which leads to the real question: are you an income investor hoping for a comeback, or are you willing to accept growth as a proxy for yield?

PAA vs. Other Midstream Plays: Where Else Can You Get Yield?

Enterprise Products Partners (EPD): The Dividend King Still Standing

Still craving that old-school MLP payout? Enterprise Products Partners (EPD) never cut its distribution. It’s increased it for 25 straight years. Currently yielding 6.8%, backed by 50,000 miles of pipeline and $4 billion in annual EBITDA. Solid as bedrock.

Yes, you still get a K-1. Yes, it’s an MLP. But if you want yield with durability, EPD is the gold standard. PAA used to be in that conversation. Now it’s not.

Energy Transfer (ET): High Yield, Higher Risk

ET yields over 8% and has a sprawling footprint from the Permian to the Gulf Coast. But its leverage ratio sits at 4.8x—above the 4.0x threshold many analysts consider safe. And its distribution coverage is tight, hovering near 1.1x.

That said, it’s still paying. For risk-tolerant investors, ET offers what PAA no longer can. But don’t pretend it’s a safe harbor.

Or Just Go with a C-Corp: Chevron’s 4% Yield

Sometimes the smarter move is stepping outside midstream entirely. Chevron yields 4%—lower, sure—but with a 36-year streak of dividend increases and a payout ratio under 50%. It’s less exciting, but also less likely to vaporize your income stream in a downturn.

And that’s exactly where I find PAA’s old investor base ending up: disillusioned, but slowly migrating toward more reliable names—even if the yields aren’t quite as juicy.

Frequently Asked Questions About PAA and Dividends

Will PAA Ever Pay a Dividend Again?

Maybe—but not anytime soon. Management has repeatedly stated that dividends are “not a near-term priority.” Their focus is on achieving an investment-grade credit rating, which they’re halfway to (currently rated BB+, one notch below IG).

Until that goal is met, reinvestment and debt repayment come first. I wouldn’t expect a dividend before 2026, and even then, it would likely start small—think 1% to 2% yield initially. We’re far from it.

Why Convert from MLP to C-Corp If You’re Not Paying Dividends?

Great question. The MLP structure became a liability. Fewer institutions wanted to deal with K-1s. ETFs were excluding MLPs. The market discount widened. By going corporate, PAA made itself more attractive to passive investors and index funds.

It’s a long-game play. The dividend may be gone, but the hope is broader ownership and a higher valuation multiple over time. Whether it works remains to be seen.

Can I Still Make Money on PAA Without a Dividend?

Absolutely. Total return isn’t dead. The stock trades at under 6x EBITDA—cheap compared to peers. Buybacks are accelerating. Free cash flow is strong. If oil stays above $70, PAA’s assets keep producing value.

You just have to be okay with waiting for capital gains instead of collecting quarterly checks. That changes everything for some investors—but not all.

The Bottom Line: PAA Isn’t Broken—It’s Just Different Now

So does PAA have a dividend? Not today. And possibly not for years. But framing the question that way misses the bigger shift. This isn’t a company clinging to its old identity—it’s one reinventing itself for survival and long-term stability.

I find the nostalgia around PAA’s payouts a bit overrated. The pre-2020 model was unsustainable. Debt was ballooning. Commodity swings were eating margins. The old dividend wasn’t “safe”—it was sitting on a fault line.

Now? PAA is leaner, simpler, and better capitalized. It may not send you a check every quarter, but it might actually be around to do so in 10 years—which, let’s be clear about this, was far from guaranteed before.

My take: if you need income now, look elsewhere. EPD, OKE, even XOM offer better options. But if you believe in the enduring need for energy infrastructure—and in management’s ability to allocate capital wisely—PAA could still earn a spot in a growth-oriented energy play.

Just don’t buy it for the yield. Because right now, there isn’t one. Data is still lacking on future payouts, experts disagree on timing, and honestly, it is unclear if the old model ever comes back. But then again, maybe we don’t need it to.