Decoding the Filipino Consumption Basket: Where Does the Money Actually Go?

To understand what people are buying, we have to look at the intersection of cultural habit and disposable income. The local economy is largely driven by a massive, young middle class with an average age under 25, meaning consumer habits trend heavily toward self-expression, mobile connectivity, and instant gratification. Except that we cannot look at retail through a singular lens anymore because the transition to digital payments has fractured how goods are distributed from Manila to the farthest provinces of Mindanao.

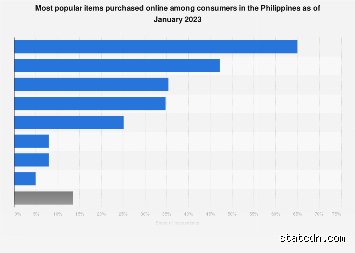

The Statistical Reality of High-Frequency Purchasing

Recent data from multi-channel commerce platforms shows that the average online shopper in the country makes approximately 8.4 purchases per month. That changes everything when you realize these are not calculated, high-investment decisions. Instead, they are high-frequency, low-ticket impulse buys. While basic groceries and food products consume the largest portion of any household budget in terms of raw peso value, the sheer transaction volume belongs to non-perishable consumer lifestyle goods. And this is exactly where the discrepancy between what people need and what they actually buy becomes most visible.

The Role of Mega Shopping Campaigns

Why do certain products experience such violent spikes in sales volume? The answer lies in the monthly double-digit promotional events popularized by regional platforms. Dates like 11.11 and 12.12 have evolved from simple marketing gimmicks into national shopping holidays where millions of items change hands in a 24-hour window. The issue remains that these events bias consumer data heavily toward items that are easy to ship, highly visual, and priced low enough to bypass any buyer hesitation.

---The Digital Overhaul: How Shopee, Lazada, and TikTok Shop Split the Prize

We used to think of retail as a battle between giant shopping malls, but today the real war is fought over smartphone screen real estate. The market share data for fiscal year 2025 shows a fascinating polarization of consumer habits across the three major digital platforms. People don't think about this enough: you aren't just looking at different websites; you are looking at entirely different psychological triggers that dictate what gets bought.

Shopee's High-Volume Dominance in Fashion and Apparel

According to recent industry audits, Shopee secured a massive 55% share of the combined top platform Gross Merchandise Value (GMV), generating roughly 12 billion USD across 399 million orders. Where it gets tricky is looking at what specifically filled those millions of packages. Fashion and apparel led the charge at 27% of Shopee's total GMV. This means casual t-shirts, midi dresses, and affordable footwear are moving at a scale that no physical boutique could ever dream of replicating. It is a system built on habit, fueled by voucher hunting and predictable shipping discounts.

TikTok Shop and the Rise of Entertainment-Driven Impulse Buys

But wait, if Shopee holds the volume, where is the growth? TikTok Shop experienced an explosive 53% year-on-year growth, capturing 29% of the platform market share by leaning heavily into social commerce. On this platform, the data shifts subtly: beauty and personal care products lead at 28% of its GMV, closely followed by fashion at 26%. It is an ecosystem where a single viral short-form video or an engaging live-streamer can cause a specific lip tint or K-beauty serum to sell tens of thousands of units in a single afternoon. Honestly, it's unclear if this hyper-growth can sustain itself without causing consumer fatigue, yet the current numbers are undeniable.

Lazada's Defensive Hold on Branded Consumer Electronics

Lazada presents a completely different story, having contracted slightly to a 3 billion USD GMV, but retaining something highly coveted: the highest Average Order Value (AOV) at 416 PHP per transaction. Instead of fighting over 150 PHP t-shirts, Lazada has successfully cornered the market for higher-ticket, authenticated goods through its specific mall infrastructure. Here, electronics and appliances make up 26% of the GMV, proving that when Filipinos want to buy a smartphone, a reliable power bank, or a new kitchen appliance, they value authenticity guarantees over the lowest possible price floor.

---The Surprising Nuance: Consumables vs. Lifestyle Goods

Every standard economic report will tell you that the most bought products in any developing nation must be rice, instant noodles, or canned sardines. But are we talking about corporate logistics or consumer choice? If we isolate open-market retail and e-commerce, a fascinating contradiction emerges between what traditional brick-and-mortar stores move and what digital logistics pipelines handle.

The Micro-Transaction Economy of Sari-Sari Stores

In the physical world, the true champion of volume is the neighborhood neighborhood store, locally known as the sari-sari store. These tiny establishments process billions of micro-transactions daily, selling single-use sachets of shampoo, instant coffee, and laundry detergent. As a result: the absolute most manufactured and distributed physical units in the entire country are undeniably these plastic sachets. But this is survival purchasing, not discretionary consumer preference. When we ask what the most buyed product is in the context of expanding market trends, we are looking at the modern consumer's shift toward lifestyle upgrading.

The Convergence of Health, Wellness, and Social Proof

In a parallel trend, wellness products have experienced an unprecedented surge, with health and wellness consumables climbing back to an 8% market share on major platforms. Herbal supplements, whitening lotions, and weight-management products are no longer niche health food store items; they are mainstream staples. This shift is directly tied to the expansion of digital wallet networks like GCash, which is now utilized by an astonishing 97% of online shoppers in the Philippines. Because transferring money is now frictionless, buying a 300 PHP bottle of vitamins after seeing a recommendation on social media requires almost zero effort from the consumer.

---Comparing Market Drivers: What Moves Fast vs. What Costs Most

To truly isolate the most bought item, we must build a clear distinction between the velocity of transactions and the total financial footprint of product categories. A single transaction for a mid-range television might equal the value of two hundred pieces of fast-fashion clothing, but which one truly defines the current state of the Philippine market?

When you contrast these categories, the data reveals a stark divide in consumer priorities, which can be visualized by looking at how different brackets of the population allocate their digital funds. On one hand, you have consumer electronics—boasting an incredible 90% penetration rate among surveyed active online buyers—which demands a large chunk of cash but happens infrequently. On the other hand, apparel sits comfortably with a 74% penetration rate but repeats weekly. Which matters more to a logistics company processing millions of sorting center entries every night? The answer is always volume.

The Fast Fashion Velocity

The velocity of apparel purchasing is sustained by an incredibly low barrier to entry. With local manufacturing and cross-border logistics optimizing their supply chains, a consumer can purchase a trendy outfit for less than the cost of a single fast-food meal. This has created a disposable fashion culture where garments are bought for specific social media posts or weekend events and replaced immediately. It is an unsustainable cycle from an environmental standpoint, but from a pure volume perspective, it keeps the shipping hubs working at maximum capacity night after night.

Common Pitfalls in Analyzing Filipino Consumer Behavior

The Illusion of the Megacity Shopping Basket

Step into any towering mall in Bonifacio Global City. You will see shoppers clutching premium espresso drinks and high-end cosmetics. Because of this flashy imagery, external analysts frequently assume that high-ticket electronics constitute the most buyed product in the Philippines. What a massive miscalculation. Metro Manila is a hyper-stylized bubble, yet millions of citizens live outside this urban nucleus. Rural consumption looks entirely different. When we peek into the provincial markets, we find that the true volume drivers are basic necessities rather than sleek smartphones. The problem is that glittering retail hubs blind researchers to the realities of the broader archipelago.

Ignoring the Sachet Economy Phenomenon

Why do multi-billion dollar conglomerates repackage their premium shampoos into tiny, single-use plastic packets? Western observers often mock this practice. They view it as an inefficient, environmentally disastrous anomaly. Except that for the average Filipino household, purchasing power is a daily, fluctuating battle. A laborer cannot comfortably shell out money for a full-sized bottle of detergent. Instead, they buy three small sachets every single morning. If you calculate retail volume strictly by transaction counts rather than total dollar value, these minute portions easily win the race. Failing to account for this micro-retail universe means missing the entire point of how commerce functions here.

Overestimating the Death of Brick-and-Mortar

Lazada and Shopee dominate our digital screens. Everyone loves to proclaim that traditional retail has perished. But let's be clear: the neighborhood sari-sari store remains the undisputed monarch of Filipino commerce. Over one million of these home-based shops pepper the landscape. They operate completely offline. Cash remains king. Digital analytical models tend to erase these micro-businesses because their transactions are rarely logged in centralized databases. Therefore, tracking what items people purchase requires looking past the digital app downloads and peering into the humble wooden storefronts on the corner.

The Cultural Tapestry of Pasalubong and Festive Spending

The Unseen Logistics of Gift-Giving Culture

Have you ever wondered why specific food brands experience massive, unpredictable supply shortages during December? It comes down to a deep-seated cultural tradition known as pasalubong. Whenever a Filipino travels, even just for a brief weekend trip, returning empty-handed is a social crime. We are culturally obligated to bring back regional delicacies or snacks for family and coworkers. During Christmas, this impulse intensifies tenfold. This unique psychological obligation creates a massive spike in the sales of packaged baked goods and local sweet treats. As a result: local supply chains frequently buckle under the weight of this collective cultural duty.

The Secret Rule of Brand Loyalty

Filipino consumers are surprisingly risk-averse when it comes to their hard-earned cash. If a mother trusts a specific brand of powdered milk, she will rarely switch to a cheaper generic alternative, which explains why legacy brands dominate the market share for decades. It is an emotional contract of trust. Marketing teams spend fortunes attempting to break these generational habits, yet the old-school favorites endure. True market dominance in this territory is built on familiarity rather than aggressive price cutting.

Frequently Asked Questions

What is the most buyed product in the Philippines regarding daily volume?

When measuring pure transactional volume and daily consumption, instant noodles and canned sardines consistently rank at the absolute top of the national shopping list. The average Filipino household consumes several packs of instant noodles weekly due to their affordability, which keeps these items permanently stocked in every corner store. Recent market reports from major research firms indicate that over 90% of local households purchase these quick-cooking pantry staples regularly. They serve as a reliable safety net for low-income families during tight financial periods. Consequently, FMCG food giants continue to expand their production lines to satisfy this insatiable national appetite.

How does mobile load compare to physical goods in total purchases?

Mobile airtime load represents a massive intangible commodity that rivals physical groceries in terms of transaction frequency. Because a staggering 95% of mobile users in the nation utilize prepaid SIM cards, millions of citizens purchase tiny increments of data and call credits daily. People will occasionally prioritize buying a twenty-peso internet load over a snack just to stay connected with overseas relatives or stream entertainment. This digital lifeline functions as a psychological necessity across all socio-economic classes. It constitutes a massive portion of daily micro-expenditures that traditional retail metrics sometimes overlook.

Are e-commerce platforms changing what citizens buy the most?

Online marketplaces have certainly reshaped access to goods, but they have primarily boosted the sales of fashion apparel, affordable cosmetics, and unbranded home organizers. E-commerce has democratized shopping for tech-savvy youth who crave trendy items that are unavailable in regional provinces. Statistically, fashion items and beauty products account for roughly 35% of total digital sales volume on major regional apps. However, these digital transactions still represent a smaller fraction of total national spending when contrasted with everyday physical grocery shopping. The internet has changed how people browse, but the physical supermarket still claims the majority of the household budget.

A Definitive Verdict on Philippine Consumerism

Pinpointing a single item as the ultimate winner requires looking beyond the superficial glitz of modern mega-malls. We must acknowledge that the true economic pulse of the nation beats within the cramped aisles of the neighborhood micro-retailer. Cheap packaged foods and daily mobile connectivity undeniably dominate the lives of the majority. (Admittedly, tracking every single cash transaction in a fragmented archipelago of over seven thousand islands is an impossible logistical task.) Wealthier urban classes will continue to chase the latest international smartphone releases and gourmet coffee trends. But the real commercial power belongs to the working-class citizen who buys their life in small, affordable increments every single day. We must stop analyzing this market through a restrictive Western lens if we want to understand its true nature.