Beyond Forbes: Why tracking dynastic wealth is a logistical nightmare

We see the headlines. Bloomberg publishes a list, Forbes drops its annual tracker, and everyone assumes we know exactly where the money sits. We don’t. Because tracking the wealthiest global lineages means dealing with centuries of obfuscation, private trusts, and shell companies based in Zug or the Cayman Islands. Most mainstream media outlets focus entirely on public equity, which is easy to calculate because you just multiply share price by outstanding stock. But that changes everything when you realize how much old money prefers total, unyielding silence.

The private trust smokescreen

How do you value an empire when it doesn’t want to be valued? It is a question forensic accountants spend their entire careers trying to solve, and honestly, it’s unclear if we will ever have perfect data. Take the Rothschilds, for instance. For generations, commentators have argued over their actual liquid net worth, with internet conspiracy theorists claiming impossible trillions while traditional analysts downplay their modern relevance. The truth sits in a messy middle; their capital has split into dozens of family branches, hidden behind specialized Swiss wealth management firms and non-profit foundations. That is where it gets tricky for researchers who rely on SEC filings.

Sovereign blurred lines

Then you have families where personal bank accounts and national treasuries are essentially the same room. I believe it is intellectually dishonest to compare an American retail tycoon to a Gulf royal family. In places like Abu Dhabi or Riyadh, state apparatuses fund private investments, which explains why estimating the net worth of the House of Saud or the Al Nahyan clan always triggers fierce debate among geopolitical analysts. Are we looking at state assets, or is it purely family money? The line is practically non-existent.

The retail titans and luxury monarchs at the apex of capital

When looking at the concrete numbers available in generational fortune rankings, the sheer scale of operational control held by just two or three clans is staggering. People don't think about this enough, but you probably gave money to one of these families within the last twenty-four hours. It is not just about having money in the bank; it is about owning the infrastructure of everyday consumption.

The Bentonville behemoth

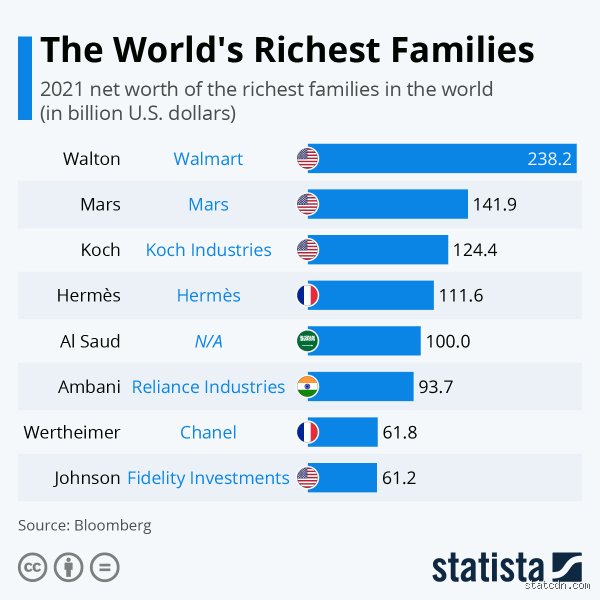

The Waltons remain the poster children for concentrated corporate ownership in America. Back in 1962, Sam Walton founded a single store in Arkansas, and today, his descendants control roughly 45 percent of Walmart’s total equity. That stake yields billions in dividends annually. Think about that for a second. While tech founders experience massive net worth swings based on Nasdaq volatility, the Walton family relies on the fact that millions of people globally must buy groceries and household goods regardless of inflation or recessionary pressures. It is an insulated, self-replicating cash machine.

The high-fashion fortress

Across the Atlantic, the Hermès family proved that exclusivity is even more lucrative than mass-market dominance. In 2023, the French luxury dynasty successfully consolidated its defensive hold over the fashion house, utilizing a tight-knit family holding company called Émile Hermès SAS to ward off hostile takeovers from predatory conglomerates like LVMH. Their collective fortune now surges past $150 billion, fueled by a deliberate strategy of artificial scarcity. They don’t just sell bags; they sell access to an aristocratic club, and that business model is remarkably resilient to economic downturns.

The industrial architects: Oil, candy, and the infrastructure of survival

If retail and luxury provide the glamour, industrial dynasties provide the raw materials that keep civilization functioning. Yet the public rarely interacts with their leadership directly. These families avoid red carpets, preferring boardrooms in Virginia or industrial parks in Germany.

The silent energy empire

Charles Koch and the heirs of David Koch control Koch Industries, a massive private conglomerate with revenues exceeding $125 billion annually according to recent corporate filings. Because they are not beholden to public shareholders, they can play the long game. They invest in everything from oil refining in Texas to chemical production and ranching land. Yet the issue remains that their massive political footprint often overshadows their actual operational mechanics, making it difficult to analyze their wealth without diving into ideological warfare.

Sweet monopolies and global logistics

Consider the Mars family. You know them for chocolate bars, but their real genius lay in diversifying into pet care and veterinary health networks—a pivot that traditional financial journalists failed to predict twenty years ago. As a result: they own a massive percentage of the veterinary clinics you see in suburban strips across North America. But we're far from the days of simple candy manufacturing; they have transformed their multigenerational asset portfolio into an ironclad defense against shifting consumer tastes.

Anarchy versus order: How sovereign dynasties reshape the financial hierarchy

To ask who are the 12 richest families without examining the absolute monarchs of the Middle East is like discussing tech monopolies without mentioning Silicon Valley. This is where conventional economic wisdom falls apart completely.

The Al Nahyan paradigm

The ruling family of Abu Dhabi sits on top of a fortune that makes Silicon Valley venture capitalists look like small-business owners. Through their control of the Abu Dhabi Investment Authority and various sovereign wealth funds, their collective economic might is tied directly to oil reserves discovered in the mid-20th century. But they aren't just sitting on crude; they have aggressively bought up sports teams, global real estate, and major stakes in western tech firms. Experts disagree on the exact distribution of these funds among the thousands of family members, but the core power structure remains entirely centralized, functioning as a hybrid between medieval governance and 21st-century hyper-capitalism.

Common misconceptions about the world’s wealthiest lineages

The illusion of public stock supremacy

You probably think the Bloomberg Billionaires Index tells the whole story. It does not. Most people glance at daily stock market tickers and assume they are looking at the definitive hierarchy of global wealth. The problem is that the truly monstrous, generational fortunes are locked away in opaque private holdings, complex trusts, and sovereign-linked entities that never see the light of a public exchange. Think about the House of Saud. Their liquid net worth laughs at tech founder valuations, yet you rarely see them topping standard magazine lists because their assets blend seamlessly with state infrastructure.

The myth of the uniform dynasty

Let's be clear:

dynastic wealth preservation is rarely a harmonious family affair. We love to imagine these twelve clans sitting around a mahogany table, unified in their global dominance. The reality is far more chaotic. Fractured branches frequently litigate against one another, diluting the core capital through endless legal battles and complex inheritance divisions. For every unified front like the Walton clan, there are three others tearing themselves apart behind closed doors.

Confusing corporate revenue with family liquidity

A massive corporation does not equal a giant pile of personal cash. When analyzing who are the 12 richest families, amateur analysts often mistake the annual revenue of a conglomerate for the actual disposable wealth of the founders' descendants. If a family enterprise generates

$100 billion in annual revenue, that capital is immediately devoured by operational expenditures, reinvestments, and taxes. The actual distribution to the family members might only be a fraction of that sum.

The invisible scaffolding of wealth perpetuity

The weaponization of family offices

How do they stay at the top for centuries? The secret lies in a hyper-aggressive institutional structure known as the single-family office. These are not mere accounting firms. They operate as private investment banks, employing elite geopolitical analysts, elite tax attorneys, and psychological advisors to manage the family's internal dynamics. By utilizing sophisticated derivative strategies and cross-border regulatory arbitrage, these offices ensure that inflation never erodes the principal capital.

The geographical shell game

Wealth does not sit in a vault in New York or London. Instead, it fluidly mutates across jurisdictions, utilizing a labyrinth of trusts in South Dakota, holding companies in Luxembourg, and foundations in Liechtenstein. Except that this creates a massive blind spot for researchers trying to track who are the 12 richest families. A single asset might be owned by a trust, which is owned by a foundation, which is leased back to the family. This architectural opacity makes traditional wealth tracking practically obsolete.

Frequently Asked Questions

How does inflation impact the assets of the wealthiest bloodlines?

Massive inflation actually acts as a wealth accelerator for these elite clans rather than a destructive force. While the average consumer watches their purchasing power erode, these syndicates hold prime real estate, scarce commodities, and dominant monopolies that naturally price-adjust upward. During hyper-inflationary cycles, the top twelve clans often expand their market share by absorbing distressed mid-tier companies at a massive discount. Statistics show that during the inflationary spikes of the early 2020s, the top 0.01% saw their aggregate asset values increase by over

$1.5 trillion dollars globally. As a result: the chasm between dynastic capital and the middle class permanently widens during economic crises.

Why are royal families often excluded from standard billionaire rankings?

Standard wealth trackers deliberately exclude royal lineages because separating personal family property from state-owned assets represents an accounting nightmare. If a monarch controls a sovereign wealth fund valued at

$900 billion, determining where public governance ends and private opulence begins is nearly impossible. Furthermore, these families possess non-liquid cultural treasures, vast ancestral lands, and strategic monopolies that are legally shielded from public disclosure. Publication of their exact net worth could also trigger severe geopolitical instability or domestic unrest. Which explains why institutional ranking systems prefer to focus on transparent corporate titans whose shares trade publicly every day.

What percentage of these fortunes is held in liquid cash?

Practically none of it sits in a standard bank account. An elite family office rarely maintains more than

1% to 2% of total net worth in liquid cash equivalents, as idle currency represents a catastrophic failure of capital efficiency. The vast majority of their resources is permanently deployed into private equity, venture capital, agricultural land, and yield-bearing infrastructure projects. They utilize specialized lombard loans to borrow against their illiquid asset portfolios when they require immediate liquidity for luxury purchases or opportunistic acquisitions. This strategy allows them to avoid triggering massive capital gains taxes while keeping their wealth continuously working in the global markets.

A final verdict on the architecture of global capital

The relentless obsession with tracking who are the 12 richest families reveals our cultural fascination with ultimate power, yet it simultaneously exposes our fundamental misunderstanding of modern macroeconomics. We shouldn't view these dynasties as mere collectors of currency, but rather as permanent institutional structures that operate above the jurisdiction of sovereign nations. Are we truly comfortable living in a global economy where a dozen private lineages wield more financial leverage than entire continents? The issue remains that democracy and extreme wealth concentration are inherently incompatible forces. If the current trajectory of capital compounding continues unchecked, the concept of a meritocratic free market will become nothing more than a historical fairytale. In short, the elite twelve are no longer just participants in the global economy; they have effectively become its landlords.