The mechanics of a tech pioneer investing in pure boredom

To understand why the man who created modern personal computing is hoarding shares of a garbage collector, you have to look closely at the institutional mandate governing his billions. The capital architecture is split between Cascade Investment LLC and the formal asset arm of the foundation. It is an intricate setup. The trust must generate enough raw liquidity to fund massive annual global health disbursements without chipping away at the core principal during a market downturn. That changes everything when it comes to risk tolerance.

The divergence of founder equity and philanthropic endowments

Where it gets tricky is separating the emotional identity of Microsoft from the clinical necessity of an endowment portfolio. In early 2026, regulatory disclosures revealed a bombshell: the trust completed a phased exit from its remaining 7.7 million shares of Microsoft, bringing its institutional stake down to zero. Honestly, it's unclear to casual observers how a founder can fully cut the cord like that. Yet, the reality is that Gates himself still holds a personal block of roughly 103 million shares of the tech titan outside the charity. The trust, operating under strict asset diversification rules, simply could not keep all its eggs in one tech basket while simultaneously trying to save the world.

The mathematical mandate of an annual payout structure

Endowments are legally required to distribute roughly 5% of their total asset value every single year. When your balance sheet sits around $33 billion, that means you need to produce over $1.5 billion in liquid cash annually without forcing desperate firesales during a macro bear market. Because of this structural reality, the asset managers at Cascade cannot afford to gamble on speculative tech valuations that might collapse by 40% overnight. They need low-beta, high-moat monopolies that cough up reliable dividends month after month.

An analysis of Berkshire Hathaway as a strategic anchor

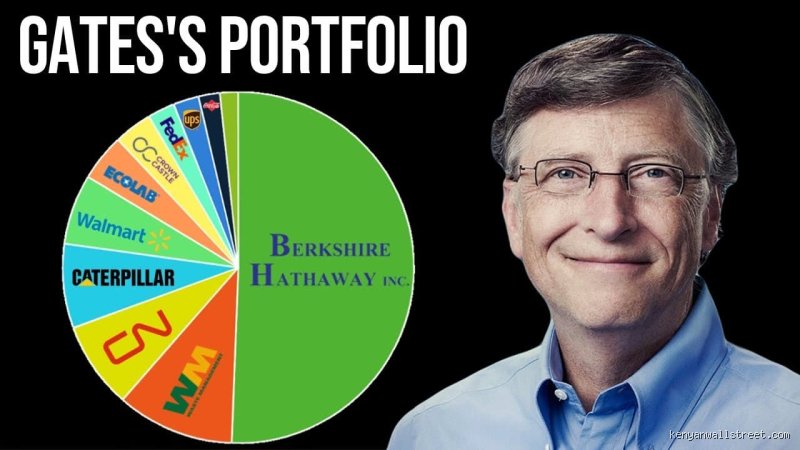

The first massive pillar of the portfolio is Warren Buffett's Berkshire Hathaway (BRK.B), commanding an enormous allocation of approximately 25.8% of the total trust capital. This isn't just a typical open-market buy story; it is deeply intertwined with a decades-long relationship and Buffett's historic philanthropic pledges. But the purely financial logic of holding this massive equity block is bulletproof even without the personal history.

The unique structural engine of insurance float

What makes Berkshire so incredibly attractive to a preservation-first fund is its massive internal diversification wrapped inside a single ticker symbol. Through massive operations like Geico and General Re, Berkshire generates billions of dollars in insurance float—money collected in premiums that hasn't been paid out in claims yet. This float acts as an incredibly cheap, almost free pool of investment capital that can be deployed into cash-generative subsidiaries. As a result: the trust gains indirect, stable exposure to vital infrastructure like the Burlington Northern Santa Fe railroad, sprawling energy utilities, and massive manufacturing entities.

The cushion against macroeconomic volatility

When inflation rages or the broader indexes experience sudden systemic shocks, Berkshire’s underlying operating businesses possess incredible pricing power. They can pass rising operational costs directly down to the consumer because people cannot simply stop paying for electricity, freight rail transport, or auto insurance. Experts disagree on whether Berkshire can beat a hyper-growth index over a twenty-year horizon, but for a fund tasked with preserving capital, that underperformance during bull runs is a perfectly acceptable trade-off for unparalleled downside protection.

The cash-flow dynamics of Waste Management

The second answer to what two stocks did Bill Gates buy is the absolute king of physical moats: Waste Management (WM). Holding roughly 20.06% of the public equity portfolio, this position represents a staggering commitment to a business that literally processes society's refuse. You could argue it is the ultimate anti-tech play. There are no software updates to ship, no microchip supply chain bottlenecks to worry about, and absolutely zero risk of the core service being disrupted by an open-source algorithm.

The regulatory fortress of landfills

Consider the sheer physical impossibility of starting a competing trash disposal corporation today. Securing environmental permits for new landfills in North America is a bureaucratic nightmare that can take decades, if not outright face permanent local opposition. Waste Management owns the actual real estate where the waste goes, creating an inescapable geographical monopoly. If a municipality or a commercial business wants to clear its garbage, they have to pay the player who controls the local landfill network, which explains why the company enjoys such incredibly predictable cash flows.

The transition to environmental infrastructure

But wait, this isn't just about old-school dump trucks rumbling down suburban streets. Waste Management has quietly transitioned into a sophisticated environmental play by capturing the methane gas emitted from its decomposing landfills and converting it into renewable natural gas. This creates an entirely new, highly profitable revenue stream that aligns perfectly with Gates' public focus on green infrastructure and climate technology. It turns a boring old municipal service company into a highly resilient compounding machine that spits out steady dividend increases year after year.

Comparing Gates' defensive duopoly against traditional index funds

Some critics look at this hyper-concentrated allocation and wonder why Cascade doesn't just buy a standard S&P 500 index fund or an aggregate bond ETF. After all, modern portfolio theory heavily preaches broad diversification across hundreds of names. But the issue remains that standard indexes are heavily weighted toward tech giants like Apple, Nvidia, and Amazon, which would re-expose the foundation to the exact same sector risks they just shed by selling out of Microsoft.

The failure of the classic balanced portfolio

The classic 60/40 investment strategy—allocating 60% to equities and 40% to fixed-income bonds—has repeatedly broken down during periods of high inflation and rising interest rates. When both stocks and bonds drop simultaneously, an endowment fund faces a structural crisis. By choosing Berkshire Hathaway and Waste Management instead of conventional debt instruments, the Gates portfolio effectively creates its own custom yield and stability engine. These companies operate like corporate bonds with an embedded equity upside, giving the trust the best of both financial worlds.

The advantage of extreme concentration

Concentration is dangerous for retail investors who lack deep analytical resources, but it is an alpha-generating weapon for an institutional trust with a permanent multi-decade horizon. By anchoring over 45% of the portfolio in just these two entities, the fund minimizes administrative overhead and transaction drag. They don't have to constantly rebalance a complex portfolio of 500 equities. Instead, they let two of the most disciplined capital allocators in corporate history do the heavy lifting while the foundation focuses its energy entirely on deployment.

Common mistakes and misconceptions about the Gates portfolio

The "Bill Buys This Personally" illusion

Most retail traders scrolling through financial news feeds operate under a massive delusion. When headlines scream about what two stocks did Bill Gates buy, the collective assumption is that the man himself sat at a terminal, analyzed cash flows, and pulled the trigger. Let's be clear: he did not. The Gates wealth engine is driven almost entirely by Michael Larson, the notoriously private Chief Investment Officer of Cascade Investment. Larson manages the money while Gates funds global eradication programs for malaria. If you clone these trades thinking you are channeling the specific tech genius of the Microsoft founder, you are fundamentally mistaken about who is steering the ship. The actual decision-making process is institutional, bureaucratic, and detached from personal tech biases.

Ignoring the 13F filing lag time

Why do amateur investors consistently lose money trying to replicate billionaire portfolios? The problem is the regulatory clock. SEC Form 13F filings only reveal what institutional managers held at the end of a specific quarter, published up to 45 days after that quarter closes. By the time you discover the identity of the two specific equities acquired by the Gates foundation trust, those exact positions might have been adjusted, trimmed, or hedged entirely. Relying on this stale data to execute short-term options or rapid day trades is financial suicide. You are looking at a rearview mirror while driving down a cliffside highway. These filings represent long-term commitments, not real-time endorsements for your next weekly option play.

Assuming Tech is the primary focus

Because of Microsoft, the world expects Gates to chase AI startups and bleeding-edge Silicon Valley ventures. Yet, a deep dive into the Bill & Melinda Gates Foundation Trust reveals an aggressive appetite for industrial monotony. The two stocks acquired during strategic rebalancing phases frequently look more like 19th-century monopolies than 21st-century disruptors. Waste management, heavy rail, and industrial logistics form the bedrock of this capital. Except that people want glamour, so they misinterpret defensive capital preservation for aggressive growth hunting.

The compounding power of defensive monopolies

Why boring infrastructure wins the long game

If you want to understand the true philosophy behind these high-conviction purchases, look at the lack of competition. The Gates strategy prioritizes businesses with regulatory moats so wide that no startup could ever cross them. Consider the massive capital expenditures required to lay thousands of miles of railroad track or to secure municipal landfill permits across North America. When Cascade Investment allocates billions toward these sectors, they are effectively buying tollbooths on the American economy. Want to move freight across the continent or dispose of medical waste in a major metropolis? You have to pay their toll. It is an inflation-proof ecosystem that generates predictable, compounding dividend streams regardless of whether the broader stock market is experiencing a bull run or a crypto crash.

The diversification imperative for hyper-wealth

We must realize that the objective of a hundred-billion-dollar portfolio is completely different from your personal retirement account. You are likely trying to maximize upside to build wealth. They are trying to prevent the erosion of an empire. This explains the heavy weighting toward defensive value equities. When looking at the specific equity pairs added to the trust, the goal is always low-beta stability to offset the inherent volatility of remaining tech holdings. Can we honestly blame them for preferring guaranteed municipal trash revenues over the wild swings of speculative tech valuations?

Frequently Asked Questions

What two stocks did Bill Gates buy during the recent portfolio rebalancing?

During the recent institutional shifts, the Gates Foundation Trust directed significant capital toward bolstering its positions in Waste Management Inc. and Canadian National Railway. The trust expanded its stake in Waste Management to encompass over 35 million shares, securing a valuation that hovers near 15 percent of the total portfolio allocation. Concurrently, the position in Canadian National Railway remains a dominant pillar, reflecting an investment worth approximately 6.5 billion dollars. These specific acquisitions emphasize a clear, deliberate pivot toward recession-resistant industrial giants that control physical infrastructure. As a result: the portfolio gains immense stability and consistent dividend cash flow to fund global philanthropic operations.

How does the Gates Foundation Trust allocate its total investment capital?

The overarching asset allocation of the trust is surprisingly concentrated, with the top four holdings frequently commanding over 80 percent of the total equity value. Microsoft remains a massive legacy footprint, yet the non-tech allocations specifically target Caterpillar Inc. and Berkshire Hathaway alongside the aforementioned logistics giants. Recent financial disclosures indicate that the total portfolio value exceeds 42 billion dollars, distributed across less than two dozen individual companies. This highly concentrated approach contradicts standard retail advice regarding hyper-diversification. The issue remains that managing billions requires deep liquidity, forcing the trust to stick with large-cap entities capable of absorbing massive capital inflows without moving the market price drastically.

Can retail investors beat the market by cloning the Gates portfolio?

Replicating this specific institutional strategy rarely yields market-beating returns for the average retail trader over short horizons. While tracking what two stocks did Bill Gates buy provides a great safety signal, the strategy is explicitly designed for capital preservation rather than explosive capital appreciation. Historical performance metrics show that this defensive, value-heavy blend underperforms the S&P 500 index during aggressive tech-driven bull markets. But for investors who prioritize wealth preservation, downside protection, and steady dividend growth, the strategy offers an exceptional blueprint. It provides a masterclass in risk mitigation, which explains why the portfolio withstands macroeconomic shocks significantly better than standard growth funds.

A definitive verdict on the Gates investment doctrine

Stop looking for speculative lightning strikes in the transaction history of the world's most visible billionaire. The real genius of the Gates portfolio lies in its deliberate, unapologetic boredom. By anchoring billions in trash collection and railway logistics, the portfolio creates an unbreakable financial floor that prints cash regardless of macroeconomic chaos. This is not an ecosystem built on hope or viral trends; it is built on the absolute certainty of physical necessity. If you want to invest like Gates, you must abandon the emotional high of the hype cycle and embrace the lucrative reality of unglamorous monopolies. In short: wealth isn't maintained by chasing the future, but by owning the indispensable infrastructure of the present.