Deconstructing the madness of the price-to-earnings metric

People don't think about this enough: a valuation multiple is only as reliable as its denominator. The price-to-earnings ratio looks like simple arithmetic, a clean fraction dividing the current share price by the trailing twelve months of earnings per share. Yet, it can turn into a complete optical illusion when underlying conditions shift violently. We track this metric religiously to see how much the market is willing to pay for a single dollar of corporate profit. Historically, a normal, boring long-term average for the S&P 500 hovers somewhere around 15 or 16.

The mathematical trap of a shrinking denominator

When corporate net income drops toward zero, the resulting fraction approaches infinity. That changes everything. You see, the spike in 2009 to over 120 times earnings occurred because aggregate corporate earnings for the index plummeted by more than 90% in the wake of the global financial crisis. Stock prices fell too, of course, but they found a bottom in March 2009 and began discounting a future economic recovery. Because trailing earnings were still abysmal, reflecting the horrific write-downs of toxic banking assets, the mathematical result was an all-time record valuation multiple. It was a phantom bubble.

Trailing twelve months versus forward-looking projections

Where it gets tricky is choosing which corporate timeline to actually measure. A trailing price-to-earnings calculation relies entirely on realized, audited, historical facts from the past year. But what if those historical facts are completely unrepresentative of the next twelve months? Forward calculations swap out the past for consensus Wall Street analyst estimates, which smooths out the severe trailing spikes but introduces human bias and relentless optimism. Honestly, it's unclear which method provides the truest signal during a crisis, because both are deeply flawed snapshots of an evolving economic reality.

The absolute peaks of broader market valuation indexes

If we look beyond standard market cycles, the historical record shows only a handful of moments where the entire stock market truly detached from normal valuation bounds. The dot-com crash and the 2008 financial meltdown stand as the twin peaks of this statistical absurdity. Yet, the underlying mechanisms that drove these two legendary peaks were completely antithetical to one another.

The tech bubble peak of 2001

Before the Great Recession redefined mathematical absurdity, the dot-com bubble collapse pushed the S&P 500 trailing price-to-earnings ratio to a then-unheard-of 46.50 in December 2001. That era was defined by pure, unadulterated speculative mania where companies with zero revenue were capitalized at billions of dollars. Investors eagerly bought into narratives of a new economic paradigm. When the dream shattered, stock prices crashed hard, but the simultaneous evaporation of tech-sector earnings kept the trailing valuation multiple compressed at historically elevated levels for months. It took years of painful corporate restructuring and real cash-flow generation to bring the market back down to Earth.

The post-pandemic anomaly of late 2020

A similar, though less extreme, phenomenon played out during the strange economic dislocations of the recent past. By October 2020, the market multiple surged to 34.24 as tech giants rallied aggressively while traditional brick-and-mortar businesses saw their revenue temporarily wiped out by global lockdowns. Investors were looking clear across the valley of the pandemic, paying premium prices for tech earnings that were accelerating wildly due to remote work trends. The issue remains that when public policy and massive liquidity injections flood the financial system, asset prices react instantly, while the underlying corporate income statements require several quarters to reflect the actual macroeconomic shifts.

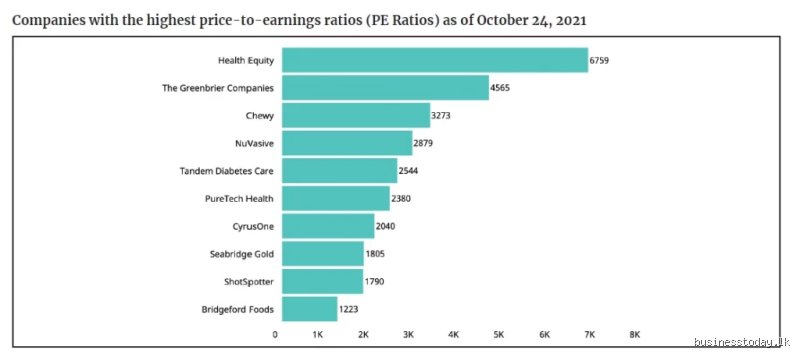

Corporate outliers and the realm of infinite valuation multiples

Individual public companies make the broader market index look incredibly tame. When a single company catches a massive wave of technological disruption or industry hype, its multiple can ascend into thousands, or simply cease to exist mathematically if they run a net loss. I believe looking at these individual corporate outliers tells us far more about human psychology than it does about cold, hard financial theory.

When individual companies break the valuation matrix

Take a look at companies transforming their business models or riding massive structural shifts. Tesla, for instance, has famously traded at a trailing multiple of nearly 371x within recent market memory, sporting a massive market cap because investors refused to value it as a low-margin legacy automaker. Instead, the market priced it as an autonomy, robotics, and energy infrastructure monopoly. But is that the highest ever for an individual firm? Far from it. During the peak of the internet bubble, infrastructure plays like Cisco Systems or Yahoo traded at multiples well north of 1000x trailing earnings, driven by the belief that their growth trajectories were permanent and linear.

The structural mirage of the turnaround play

Sometimes, an astronomically high corporate multiple is just a boring accounting quirk. Imagine a multi-billion-dollar enterprise that suffers an unexpected legal settlement or a massive asset depreciation charge, leaving it with a net profit of just $100,000 for the year. If its market capitalization is $10 billion, its price-to-earnings ratio will instantly register at a comical 100,000x. This is not because the equity markets have suddenly lost their collective minds. It is simply because a temporary, non-cash accounting event has reduced the denominator to near-zero, creating an artificial spike that disappears the very next quarter when normal operations resume.

Alternative yardsticks to cut through the statistical noise

Because the standard trailing calculation breaks down so easily during economic turning points, macroeconomists have spent decades trying to construct better valuation yardsticks. They want to eliminate the noise of the standard business cycle to see whether equities are truly cheap or expensive. The most famous attempt to fix this issue is the Cyclically Adjusted Price-to-Earnings ratio, often called the CAPE ratio or the Shiller PE.

The elegance of the Shiller PE approach

Developed by Nobel laureate Robert Shiller, this alternative model substitutes a single year of trailing data for a rolling, inflation-adjusted average of the past ten years of corporate earnings. As a result: short-term earnings collapses, like the one witnessed in 2009, or temporary profit bonanzas are completely smoothed out. Under this steadier lens, the highest market valuation ever achieved did not occur in 2009 at all. It actually happened in December 1999 at the absolute zenith of the dot-com boom, when the Shiller CAPE ratio reached an all-time high of 44.20. Except that the regular, unadjusted multiple at that exact moment was significantly lower, proving how the two metrics can tell diametrically opposed stories about market risk.

Why the CAPE ratio still draws fierce criticism

Yet, the Shiller method has plenty of detractors who argue that looking backward across a full decade completely misreads the structural shifts of the modern digital economy. Modern corporations hold massive amounts of intangible assets and generate much higher capital efficiency than the manufacturing conglomerates of the 1960s. Hence, critics argue that comparing today's technology-heavy equity index to the historical averages of the mid-twentieth century is an apples-to-oranges comparison that structurally overstates how expensive the modern market really is. The debate is far from settled among institutional asset allocators.

Common mistakes and misconceptions when evaluating valuation peaks

Investors frequently stumble into a psychological trap when hunting for the highest PE ratio ever recorded. They assume a stratospheric multiple automatically signals an imminent market crash. This is a mirage. Let's be clear: a multiple can soar not because the price is inflated, but because the denominator has vaporized.

The denominator collapse paradox

When corporate earnings plunge toward zero during a brutal economic recession, the price-to-earnings metric behaves erratically. Imagine a blue-chip enterprise whose profits suddenly drop from five dollars per share to a single penny. Even if the stock price plummets by eighty percent, the math forces the valuation metric to explode upward. You are looking at a mathematical artifact, not an enthusiastic market bubble. This specific distortion explains why trailing metrics looked utterly insane during the 2008 financial crisis, forcing analysts to mistake structural devastation for unwarranted optimism.

Confusing trailing metrics with forward expectations

Why do sophisticated funds ignore historical trailing data when assessing extreme valuations? Because the rear-view mirror tells you nothing about tomorrow's disruption. A tech startup trading at a four-digit multiple might actually be cheap if its proprietary artificial intelligence architecture captures an entire global market sector within twenty-four months. The problem is that human brains naturally crave linear patterns. Yet, exponential growth trajectories defy basic linear intuition, making traditional historical comparisons completely irrelevant. Are you evaluating what a company earned last June, or are you pricing a monopoly that matures in 2030?

The hidden plumbing of extreme market valuations

To truly grasp the dynamics behind the highest PE ratio ever, we must look at liquidity mechanisms rather than simple investor enthusiasm. Wall Street rarely discusses how microscopic float size creates artificial valuation squeezes.

The mechanics of the low-float squeeze

When a highly anticipated company lists only five percent of its total shares for public trading, structural scarcity takes over. The issue remains that passive index funds must purchase these shares regardless of cost to match their tracking benchmarks. As a result: a violent upward spiral occurs where price discovery becomes completely detached from underlying corporate balance sheets. It is an ironic twist of modern finance that the safest passive investment vehicles often fuel the most volatile, speculative asset bubbles. We must admit that predicting the exact apex of these liquidity-driven anomalies is practically impossible because irrational capital flows can outlast your short-term solvency.

Frequently Asked Questions regarding historical valuation extremes

What is the highest PE ratio ever reached by a major index?

During the peak of the dot-com hysteria in 2000, the trailing valuation of the broad Nasdaq Composite Index blasted past 100 times earnings as specualtors bid up technology equities. Even more shocking was the Japanese asset price bubble of 1989, where the Nikkei 225 index hovered around a multiple of 60, driven by hyper-inflated real estate values and complex corporate cross-shareholdings. Individual corporate entities have printed numbers in the tens of thousands during cyclical earnings collapses, but these index-level figures represent the most profound systemic valuation distortions in modern financial history. When an entire basket of hundreds of companies reaches such heights, a devastating multi-year correction becomes almost mathematically guaranteed.

Can a company maintain a quadruple-digit valuation permanently?

No business enterprise can sustain a four-digit multiple indefinitely because gravity eventually demands real cash flows to justify investor capital. As a corporate entity matures from a hyper-growth phase into an established industry titan, its revenue expansion inevitably decelerates to match macroeconomic realities. Consequently, institutional investors begin shifting their focus from speculative future promises to actual net income generation and dividend distributions. This transition triggers a process known as multiple compression, where the stock price stagnates or drops until the valuation aligns with normalized sector averages. What happens if the projected earnings fail to materialize during this critical transition period? The stock simply collapses, obliterating late-stage investors who bought the peak hype.

How did the 1999 tech bubble compare to historical valuation anomalies?

The 1999 technology bubble remains unique because it combined a genuine technological revolution with unprecedented retail speculation. Companies like Cisco Systems and Qualcomm traded at multiples exceeding 100 and even 200 times trailing profits, numbers that defied traditional financial gravity. Which explains why the subsequent crash wiped out trillions of dollars in paper wealth within a matter of months. While previous historical bubbles were localized within specific sectors like railroads or real estate, the dot-com collapse infected global capital markets simultaneously. It proved definitively that placing an infinite valuation on internet traffic metrics while ignoring actual net losses is a recipe for financial catastrophe.

Rethinking the boundaries of financial gravity

Fixating on the absolute highest PE ratio ever misses the broader philosophical point of capital allocation. These numerical anomalies are not mere historical trivia; they are vivid psychological monuments to human greed and systemic liquidity distortions. We live in an era where central bank interventions routinely rewrite the rules of asset pricing, making historical benchmarks look increasingly quaint. Do not comfort yourself with the naive belief that modern algorithms have immunized us against these spectacular speculative delusions. When the next paradigm-shifting technology arrives, market participants will gladly throw the rulebook out the window all over again. Ultimately, the ultimate peak valuation is never a fixed destination, but rather a reflection of how much collective fiction the market is willing to believe at any given moment.