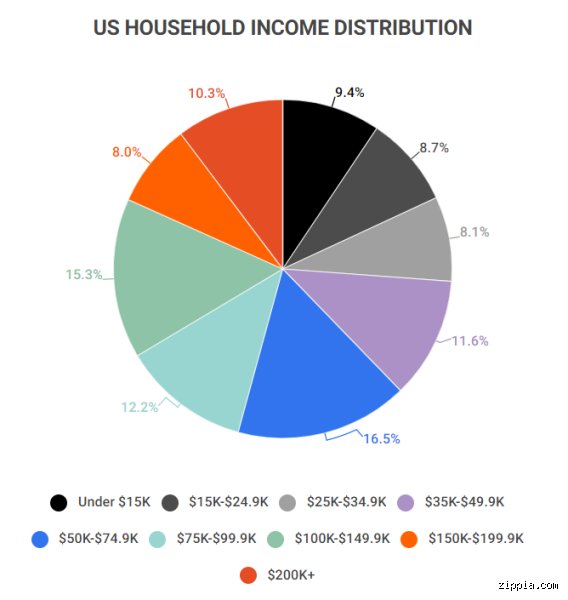

The Fragmented Reality of the American Paycheck

We love to chase a single magic number. The Bureau of Labor Statistics recently posted a median weekly earning report that translates to roughly $60,000 a year, but let's be real—nobody is living the American Dream on that in 2026. What is considered a good US salary in one ZIP code would barely cover rent and a basic health insurance premium in another. The issue remains that national averages are a mathematical illusion masking a fractured economic landscape.

The 0k Psychological Threshold vs. Purchasing Power

For decades, six figures was the ultimate milestone of making it. But hitting $100,000 today feels eerily like earning $75,000 just a few short years ago, thanks to a brutal compounding stretch of post-pandemic inflation that permanently shifted the cost of groceries, utilities, and used cars. It is a psychological milestone, sure. Yet, when Uncle Sam takes his cut through federal, state, and FICA taxes—especially if you reside in a high-tax state like California—your take-home pay shrinks faster than a cheap wool sweater in a hot dryer.

Dissecting the Median vs. the Living Wage

Where it gets tricky is comparing what people actually earn versus what it costs to simply survive without drowning in credit card debt. A living wage calculation for a single adult in a place like Peoria, Illinois, is vastly different from the financial oxygen needed to breathe freely in San Francisco. Because of this, looking at the national median income gives us a flawed benchmark; it tells us what is common, not what is comfortable or sustainable for a forward-thinking career professional.

Geographic Taxations and the Great Locality Chasm

Geography dictates your financial destiny far more than your actual job title. You can take a remote software engineering role paying $140,000, which makes you an absolute king in McAllen, Texas, where housing costs are practically subterranean. Move that exact same salary to Manhattan, and suddenly you are hunting for roommates on social media and wondering why a mediocre salad costs twenty-five bucks.

The Coastal Premium: New York, SF, and Seattle

To truly understand what is considered a good US salary in America’s economic engines, you have to throw out standard budgeting rules. The traditional 30% rule for housing is dead and buried in places like Brooklyn or downtown Seattle. In these coastal concrete jungles, a good individual salary starts at $180,000, which explains why tech workers making two hundred grand still complain about feeling stuck in the middle class. Except that they aren't actually poor—they are just asset-poor because the baseline cost of entry for property ownership has skyrocketed beyond reach.

The Sunbelt Shift and the Death of "Cheap" Cities

Then we have the massive migration waves toward the Sunbelt over the last few years. Austin, Phoenix, and Miami used to be the affordable havens where a mid-tier corporate income went incredibly far. Not anymore. I watched the median home price in cities like Boise, Idaho, detach completely from local wage growth between 2021 and 2026, driven by an influx of remote workers carrying coastal paychecks into local economies. As a result: local teachers and hospitality staff have been priced out entirely, proving that "good" is a highly volatile, moving target.

The Real Math: Fixed Costs, Taxes, and What is Left Over

Let's actually look at the ledger. Take a gross salary of $120,000—a number most Americans would consider fantastic. After a standard deduction, federal income taxes devour a massive chunk, state taxes take another bite (unless you are lucky enough to live in Florida, Texas, or Nevada), and healthcare premiums for a family easily run $500 to $1,200 monthly depending on the employer's subsidy.

The Hidden Drain of Student Loans and Childcare

People don't think about this enough when negotiating a job offer. If you graduated from a private university with $80,000 in debt, your monthly student loan payment acts like a second rent. Combine that with the staggering cost of full-time infant daycare in America, which currently averages over $1,500 a month in suburban markets, and your seemingly robust income starts evaporating before you even buy groceries. Can you really call a salary good if it leaves you with just a few hundred dollars of discretionary income at the end of the month?

How Our Definition of Financial Comfort Has Changed

What we expect from our income has fundamentally evolved over the past decade. A generation ago, a solid income meant owning a three-bedroom suburban home, keeping two sedans in the driveway, and taking a two-week summer vacation to the coast. Today, the younger workforce views a good salary through the lens of stability and options rather than material accumulation.

The Death of the Pension and the Burden of the 401k

The thing is, modern workers carry financial burdens their parents never even had to consider. Since corporate pensions have largely vanished into the annals of history, saving for retirement is entirely on your shoulders. A truly good US salary must be high enough to allow you to maximize your 401(k) contributions—which stands at a maximum of $23,500 for standard filers—without forcing you to eat instant ramen for dinner every night. If your wage doesn't allow for aggressive investing, it is merely a survival wage, no matter how many commas are on the pay stub.

Common Myths Busting the "Perfect Number" Illusion

The Illusion of a Single National Benchmark

You cannot evaluate American compensation using a blanket standard. To declare that a specific six-figure sum guarantees comfort everywhere is pure fantasy. The problem is that a ninety-thousand-dollar paycheck buys a vastly different lifestyle in Manhattan compared to Mobile, Alabama. This massive geographical variance completely distorts what is considered a good US salary. While an individual earning eighty thousand dollars feels like royalty in rural Ohio, that exact same gross revenue forces a worker into cramped, shared housing in San Francisco.

Ignoring the Stealth Tax of Local Cost of Living

Gross income is a vanity metric. Many professionals celebrate landing a high-paying role, only to realize that state income taxes, municipal levies, and skyrocketing grocery prices erode their purchasing power immediately. Let's be clear: a hundred and twenty thousand dollars in Texas, which features no state income tax, frequently yields superior discretionary cash flow than a much higher nominal paycheck in New York. You must calculate net disposable income after accounting for localized inflation, transport costs, and mandatory regional expenses before determining if a compensation package truly qualifies as premium. Regional price parities fundamentally dictate your actual wealth far more than the digit printed on your employment contract.

The Danger of Comparing Base Salary to Total Compensation

Base pay tells only a fraction of the story. Silicon Valley tech workers and Wall Street financiers often look at modest base salaries while pulling down massive annual bonuses, stock options, and comprehensive health benefits. Except that the average observer looks exclusively at the base rate, which explains why so many job seekers misjudge the market. Evaluating a job offer solely on the base figure is a critical misstep. A robust retirement match, zero-premium healthcare, and equity grants can easily transform an otherwise mediocre salary into an elite financial arrangement.

The Hidden Lever: Benefits and Lifestyle Inflation

The Compounding Weight of Lifestyle Creep

Earning more money rarely solves financial anxiety if your expenditures scale up at an identical pace. As professionals climb the corporate ladder, they routinely upgrade their housing, vehicles, and leisure activities, which effectively neutralizes their raises. What is considered a good US salary under these conditions? It becomes a moving target that is impossible to hit. (We all know that one colleague pulling in two hundred thousand annually who still manages to live paycheck to paycheck.) True financial freedom requires decoupling your consumption habits from your earnings trajectory, ensuring that increased revenue funds your investment accounts rather than depreciating luxury assets.

The Outsized Role of Healthcare and Childcare Costs

American infrastructure shifts massive financial burdens onto the individual. For families, the dual monsters of premium medical insurance and private childcare can completely devour a seemingly robust income. In many states, full-time daycare for two children exceeds two thousand dollars monthly, an expense that demands an incredibly high gross income just to break even. As a result: an unmarried twenty-something might thrive on sixty thousand dollars, while a family of four requires triple that amount to achieve identical financial security in the exact same ZIP code. Employer-sponsored health plans can save workers thousands of dollars annually, proving that benefits are just as vital as cash.

Frequently Asked Questions

What is considered a good US salary for a single person in 2026?

For an individual without dependents, a gross annual income ranging between seventy-five thousand and eighty-five thousand dollars provides an excellent quality of life across most of the nation. This range comfortably exceeds the median individual earnings in the United States, which currently hovers around fifty-nine thousand dollars. With this revenue, a single professional can easily afford a modern one-bedroom apartment, maintain a reliable vehicle, fund a retirement account, and enjoy frequent dining out. Yet, if that same individual resides in premium coastal hubs like Boston or Los Angeles, the baseline for a comparable lifestyle climbs drastically closer to one hundred and ten thousand dollars. Ultimately, your personal debt obligations, particularly student loans, will heavily influence how far this money stretches.

How much income does a family of four need to live comfortably?

A household with two adults and two children generally requires a combined revenue of at least one hundred and thirty-five thousand dollars to achieve genuine financial peace of mind. This benchmark allows the family to allocate thirty percent of their income toward a comfortable three-bedroom suburban home while managing the relentless costs of groceries and extracurricular activities. Statistics indicate that the average American family spends over nine thousand dollars annually on food alone, a figure that escalates wildly with teenagers in the house. In short, this income level ensures the family can consistently save for future college tuitions while simultaneously building a robust six-month emergency fund. Families earning below ninety thousand dollars in major metropolitan zones often find themselves making stressful trade-offs between convenient housing and quality childcare.

Does earning a six-figure salary guarantee financial freedom in America?

Reaching the symbolic milestone of one hundred thousand dollars no longer guarantees affluent status in the modern American economy. While hitting this mark places an earner comfortably within the top twenty percent of individual workers nationwide, inflation has significantly eroded its historic purchasing power. Why do so many six-figure earners still feel financially squeezed? The issue remains that high-paying jobs are heavily concentrated in hyper-expensive urban centers where real estate prices are prohibitively high. A salary of one hundred thousand dollars in a city like Seattle will quickly be swallowed by a median monthly rent of two thousand five hundred dollars and steep local taxes. True financial liberation is never a byproduct of a specific income tier, but rather the result of maintaining a wide, deliberate gap between your earnings and your structural overhead.

The Reality of American Compensation

We need to stop chasing an arbitrary national number because the concept of a uniform financial benchmark in a country as economically diverse as the United States is a complete illusion. Chasing a specific dollar amount without factoring in your local geography, family dynamics, and personal definitions of freedom will only lead to perpetual dissatisfaction. Income is purely contextual, meaning a modest paycheck in a low-cost region frequently delivers a superior quality of life compared to a massive, heavily taxed salary in a coastal megacity. Do not let corporate titles or arbitrary cultural milestones dictate your worth or your career choices. True wealth is measured by disposable cash flow and time autonomy, not the misleading gross figure on your tax return. Focus your energy on maximizing your savings rate and minimizing fixed costs, because that is where real financial power resides.