The Statistical Illusion of Canadian Upper-Class Thresholds

Slicing the Percentiles on Paper

People don't think about this enough: a top-tier income status looks incredibly impressive on a Statistics Canada spreadsheet but feels surprisingly modest when deposited into a Vancouver or Toronto bank account. If you cross the line of $125,942 annually, you technically clear the barrier into the top 10 percent of Canadian earners. Push that further to $162,210 per year, and you are officially sitting in the top 5 percent of the country's population. It sounds like a massive victory, yet the issue remains that these federal metrics group a corporate executive living in downtown Toronto with a specialized medical professional practicing in rural New Brunswick. The real-world purchasing power of those two salaries could not be more polarized.

The Real Price of the One Percent

Where it gets tricky is looking at the actual peak of the compensation mountain. To cross the threshold into the elite 1 percent nationwide, your personal tax return needs to show at least $315,911 in annual compensation. But if you look closely at the average earnings within that specific group, the numbers skyrocket to $586,900 per year due to the massive bonuses and equity packages given to corporate executives. It is a staggering amount of money, yet we are far from the astronomical wealth seen south of the border. Honestly, it's unclear to many global professionals why Canadian salaries lag so far behind American corporate hubs, but the reality on the ground forces a completely different strategy for preserving wealth.

Taxation Dynamics and the Reality of Net Income

The Illusion of Gross Compensation

Let us look at a brutal truth: a high gross salary in Canada is essentially an accounting fiction until the provincial and federal governments take their massive shares. When you finally climb into the upper class, you are immediately met with a progressive tax system that acts as a financial brick wall. Take a corporate vice president based in Ontario who successfully negotiates a $300,000 baseline salary. On paper, they are an undeniable success story. But after the Canada Revenue Agency and the provincial ministry extract their combined cuts, that impressive sum shrinks down to roughly $172,000 in take-home pay. That changes everything because you are suddenly trying to fund a luxury lifestyle with just over half of what your employer actually pays you.

Marginal Rates as a Wealth Anchor

The system is specifically engineered to make accumulating massive cash reserves through a standard T4 employment slip incredibly difficult. Once your taxable earnings cross the top federal bracket, every extra dollar you bring in faces a combined marginal tax rate that hovers around 53.53 percent in Ontario and peaks at an astonishing 54.8 percent in Quebec. Think about that for a moment. You are doing the high-stress work, putting in the eighty-hour weeks, and taking on massive corporate liability, yet the government becomes the majority partner in your career success. As a result: reliance on a traditional salary alone is a deeply flawed strategy if your goal is true, generation-defining wealth.

The Geographic Great Divide in Modern Purchasing Power

The Cost of Metropolitan Existence

Location is the ultimate variable that completely breaks traditional definitions of financial success. Earning $200,000 as a software architect in Calgary allows you to purchase a sprawling detached home, park two premium vehicles in the driveway, and build a substantial investment portfolio without checking your bank account. Take that identical salary to Vancouver, and you are suddenly looking at a hyper-competitive real estate market where a standard, unrenovated bungalow requires a multi-million-dollar commitment. I have watched high-earning couples bring in a combined $350,000 household income in the Greater Toronto Area who still feel intense financial anxiety because a basic mortgage eats up $6,500 of their after-tax cash flow every single month. Can you genuinely call someone wealthy when they are struggling to outbid twenty other buyers for a semi-detached house built in the 1970s?

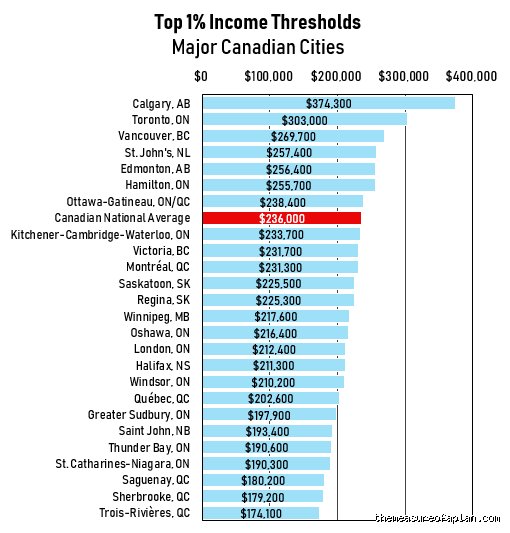

The Regional Disparities of Tax Filers

Statistics Canada confirms this geographic polarization with undeniable data. The median income of the top 1 percent in Alberta sits at a robust $495,300, heavily driven by the resource sector and a flat provincial tax legacy that kept margins higher. Meanwhile, Ontario's top earners average $534,800, but that capital is concentrated in a hyper-inflated real estate ecosystem that aggressively erodes its actual utility. Except that if you look at Prince Edward Island, the entry point for the top 1 percent drops significantly to $386,500. It is a completely different economic universe, which explains why smart professionals are increasingly abandoning the old urban centers for provinces where their dollars aren't instantly vaporized by local living costs.

Salary Wealth Versus Generational Capital Assets

The High-Earner, Not Rich Yet Dilemma

We must make a sharp distinction between a high salary and genuine net worth. A massive income stream can stop instantly due to corporate restructuring, illness, or market downturns—making a high-earning employee surprisingly fragile. This brings us to the rise of the HENRY demographic: High Earners, Not Rich Yet. These are professionals earning $250,000 to $400,000 annually who look wealthy from the outside because they drive German sedans and live in desirable postal codes, but their balance sheets are completely hollow. They are running on a high-speed treadmill, spending nearly everything they earn to maintain an elite social image while saving very little. Yet, experts disagree on whether this lifestyle is sustainable in an era of persistent structural inflation.

The True Power of Asset Ownership

The real divide in Canada isn't actually between people who make $80,000 and those who make $180,000; it is between those who rely solely on a salary and those who own appreciating assets. To comfortably join the wealthiest 1 percent of citizens by net worth, you need to control at least $9,963,458 in total assets. A massive portion of that wealth pays zero attention to traditional income brackets because it grows through capital gains, corporate structures, and primary real estate exemptions. In short, a wealthy salary is merely a temporary tool used to buy freedom, not the destination itself.