Understanding the Baseline: What It Takes to Be in the Top 10 Percent

The Raw Statistical Benchmarks

Let's look at the numbers straight from the source. Recent Internal Revenue Service data and Federal Reserve economic summaries reveal that individual earners must clear about $148,812 in gross adjusted income to peek over the fence into the top decile. The thing is, looking at an isolated individual doesn't tell the full story because most Americans pool resources. For a household, the national median entry point slips past $211,400, which ironically matches up with where the federal 24 percent tax bracket starts to pinch married couples. If you are tracking the ultimate high-water marks, the Federal Reserve points out that the bottom boundary of net worth for this same group sits at roughly $970,900. We are far from the ultra-wealthy territory here, but it is a massive leap from the standard American baseline.

Why Averages Lie to the American Taxpayer

You cannot trust a nationwide average when analyzing upper-tier wealth distribution. Where it gets tricky is that a single national figure lumps a surgeon in Cleveland together with an administrative law partner in Washington D.C. The broad national metric suggests a level of comfortable uniformity that simply does not exist on the ground. Think about a dual-income family pulling in a combined $205,000 in a mid-sized Midwestern metro. They feel rich. But hand that exact same paycheck to a family renting a three-bedroom apartment in San Francisco or Manhattan, and suddenly they are scraping by after childcare costs and state taxes consume the surplus. Honestly, it's unclear why macroeconomists still prefer flat national numbers when the regional realities are so violently mismatched.

Geographic Disparities: How Location Radically Redefines the Top Ten Percent Income

The Costly Coasts versus the Heartland Barrier

Location changes everything. In West Virginia, a local household bringing in $198,000 comfortably buys admission into the top ten percent, giving those families immense relative purchasing power within their communities. But pack up those exact same moving boxes and drive northeast toward Boston or New York City, and that illusion of luxury vanishes instantly. In Massachusetts, the required household threshold skyrockets to a punishing $386,800. That is nearly double the entry fee for the exact same statistical designation. If you look at Washington, D.C., the anomaly becomes even more absurd; due to an intense concentration of corporate lobbyists, federal contractors, and high-level legal firms, households must clear roughly $635,000 to count themselves among the local elite.

The Real Estate and Local Tax Trap

But wait, there is an even bigger hurdle. High gross revenue invariably attracts heavy local taxation and inflated housing markets, which quickly eats away at your take-home pay. A household earning $350,000 in California or New York faces a combined marginal tax rate that can easily swallow over 40 percent of their marginal earnings. Combine that with a median home price that hovers around a million dollars in premium coastal ZIP codes, and your "elite" income is suddenly spoken for before it even hits your checking account. It is a strange paradox where a family can statistically rank in the top tier of national earners yet still experience genuine anxiety over funding a basic retirement account or paying for their kids' college tuition.

The Evolving Definition of Wealth: Gross Wages versus Real Assets

The Illusion of High W-2 Earnings

I find it fascinating how obsessed we are with salary numbers when salary is actually the least efficient way to build sustainable wealth. Relying entirely on a high W-2 paycheck means you are trading your immediate time for cash that is taxed at the highest possible ordinary rates. The issue remains that a doctor earning $250,000 a year from patient consultations has zero leverage if they stop working. Experts disagree on the exact tipping point, but true financial security in the upper decile is rarely built on labor alone. It requires turning that earned income into appreciating capital assets as quickly as humanly possible.

The Role of Capital Gains and Dividends

This is where the real division inside the top ten percent happens. The lower half of this group relies almost entirely on regular wages, whereas the upper half increasingly derives sustenance from corporate equities, commercial real estate, and private business equity. The Internal Revenue Service rewards this behavior by taxing long-term capital gains at a maximum base rate of 20 percent for single filers clearing over $533,400, which is significantly lower than the 37 percent top marginal rate levied on equivalent regular wages. As a result: the families who truly thrive in this bracket are those who have successfully shifted their economic dependence away from the time-clock and toward the stock market ticker.

Comparing the Top Ten Percent to the Rest of the Economic Ladder

The Widening Chasm Above the Middle Class

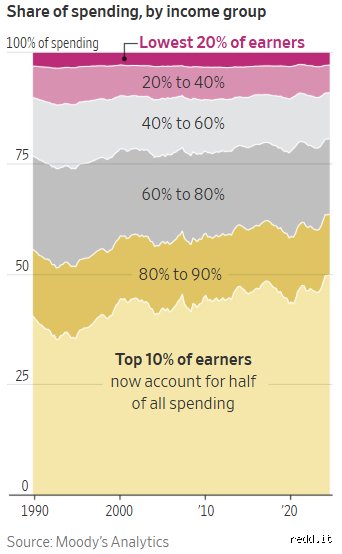

To truly understand upper-class earnings, you have to look at the distance between the top ten percent and the rest of the country. The U.S. Census Bureau recently noted that the real median household income in the United States reached an all-time high of $80,610. Do the math quickly. This means a household at the entry gate of the top ten percent is making nearly three times what the average American family brings home. Since 1970, upper-income households have seen their gross revenues grow by 78 percent, while the middle class struggled along with a much more modest 26.5 percent bump over a similar long-term trajectory. This historical divergence has fundamentally altered the social fabric of American neighborhoods.

The Quantum Leap to the Top One Percent

Yet, for all this growth, the top ten percent is still just a middle-management tier when compared to the apex predators of the economy. To jump from the top ten percent to the top one percent requires your household income to blast past $794,129 annually. That is not just a step up; it is an entirely different economic universe driven by institutional equity ownership and global corporate scale. In short, while a top-decile earner is worrying about the price of a new European SUV or the annual dues at a local country club, the top one percent is busy dictating the actual terms of the market itself.

Common mistakes and misconceptions

The individual versus household conflation

You hear a number and instantly apply it to your own paycheck. The problem is that national data sets frequently oscillate between measuring single tax filers and entire domestic units. When assessing what is the top 10 income in the US, an individual threshold sits dramatically lower than a joint household pool. If you earn $150,000 alone, you might assume you trail behind the elite pack. Except that your standalone salary actually places you well into the upper echelon of solo earners nationwide. Blending these two metrics distorts your understanding of financial standing. It causes professionals to misjudge their relative fiscal power. Conflating individual wages with household sums creates a distorted picture of where the true boundaries of wealth reside.

Ignoring the geographic cost variations

Raw numbers look imposing on a spreadsheet. Let's be clear: a six-figure baseline does not carry the same weight across different state lines. An annual revenue of $160,000 makes you an absolute financial aristocrat in Cleveland or Mississippi. Yet, that identical sum leaves an individual feeling shockingly middle-class in Manhattan or San Francisco where housing costs consume vast percentages of disposable funds. The Internal Revenue Service does not adjust its brackets for local real estate spikes. Because of this, looking solely at a flat national threshold creates a massive analytical blind spot. You cannot evaluate top-tier earnings accurately without factoring in regional purchasing power indices.

Believing income equates to net worth

High cash flow creates an illusion of permanent stability. It is a classic error to assume that entering the highest decile of annual compensation means someone possesses millions in liquid reserves. Many high-earning households face massive student debt burdens from elite universities. Others simply burn through their capital via lifestyle creep. A corporate attorney bringing home a massive salary might still have a negligible asset portfolio compared to an older, retired individual with zero active salary but a fully paid-off home and a robust stock portfolio. Mistaking annual revenue for accumulated wealth leads to flawed conclusions about economic security.

Little-known aspect or expert advice

The heavy reliance on non-wage capital

Most workers trade time for a fixed salary. When you cross the boundary into upper-tier compensation structures, the anatomy of how you get paid changes completely. The highest earners rarely depend entirely on standard W-2 paychecks. Instead, their wealth generation is driven by equity grants, performance bonuses, real estate distributions, and qualified dividends. This reality alters the financial landscape. As a result: your strategy for upward mobility cannot rely solely on asking for a standard corporate raise. You must pivot toward asset accumulation. Experts know that tax optimization becomes the primary driver of actual wealth preservation once your baseline compensation reaches these levels. Diversifying into non-wage revenue streams represents the hidden engine of sustainable fiscal dominance.

Strategic tax positioning for high earners

Are you maximizing your structural deductions? If you find yourself approaching the threshold of upper-tier earnings, traditional savings accounts will no longer shield your capital from aggressive taxation. The top decile contributes a massively disproportionate share of the national tax burden. This explains why sophisticated financial planning relies heavily on backdoor Roth IRAs, tax-loss harvesting, and corporate entity structures like S-Corps or LLCs to reclassify active compensation. Moving beyond basic retirement accounts is vital. In short, true fiscal mastery requires you to view your personal finances as a complex corporate enterprise rather than a simple checking account. Proactive structural tax management determines how much of your high yield stays in your pocket.

Frequently Asked Questions

What is the minimum individual salary needed to reach the top 10 percent of American earners?

To cross this specific threshold as an individual filer, recent data indicates you need an annual gross salary of approximately $148,812. This baseline fluctuated slightly due to recent inflation adjustments implemented by the Internal Revenue Service. It is important to remember that this figure represents the absolute entry point rather than the average of the group. If your standalone earnings clear this hurdle, you outpace roughly ninety percent of the active workforce in the United States. Consequently, achieving this milestone places a worker in a highly distinct economic tier, even if local living costs diminish the daily perception of that affluence.

How does household composition alter the top ten percent financial benchmarks?

When multiple earners combine their resources within a single domestic unit, the statistical bar rises substantially. A household typically requires a combined annual revenue exceeding $212,100 to officially enter the highest decile of national distribution. This shift occurs because a significant percentage of high-earning households consist of dual-income professionals who hold advanced degrees. These couples effectively double their earning capacity while consolidating fixed living expenses like mortgages or utilities. Therefore, measuring yourself against household metrics requires a completely different analytical framework than evaluating individual occupational salaries.

Which industries offer the most predictable pathways to securing a top-tier national income?

The occupational landscape reveals that specialized legal practices, healthcare specialties, corporate management, and advanced technology sectors dominate these upper brackets. Software architects, orthopedic surgeons, corporate executives, and investment bankers consistently command the compensation packages required to clear these high entry bars. Educational attainment correlates heavily with these outcomes since professional or doctoral degrees yield a median household net worth of roughly $592,600. While entrepreneurial ventures occasionally produce massive financial breakthroughs, traditional corporate ladders in highly technical fields remain the most statistically consistent routes to these numbers.

Engaged synthesis

Fixating entirely on a specific numerical baseline misses the true underlying narrative of modern American economics. The reality is that reaching an elite tier of compensation is no longer a guarantee of absolute financial freedom, especially when structural costs like housing and elite education continue to outpace baseline wage growth. We must recognize that high income is merely a temporary tool, a high-octane fuel that accomplishes absolutely nothing if your personal financial vehicle has a leaking tank. True economic resilience belongs exclusively to those who aggressively convert their active labor into permanent, yielding assets rather than upgrading their material lifestyles with every subsequent promotion. Do not just aim to collect a top-tier paycheck; resolve to build a fortress of independent wealth that survives long after your active salary stops flowing.