Deconstructing the Balance Sheet of American Net Worth

To grasp where the money actually sits, we must first look at what the Federal Reserve calls the Distributional Financial Accounts. The concept of wealth is frequently confused with income, yet they are entirely different animals. Income is the steady drip of a kitchen faucet; wealth is the massive, deep-water reservoir built up behind a structural dam over generations. When we strip away the regular wages, salaries, and annual bonuses, we are left with net worth, which is defined as total assets minus liabilities. The thing is, when you dissect these total assets, you quickly realize that the American middle class and the ultra-wealthy are playing two completely different games on two completely separate fields.

The Real Estate Illusion vs. Financial Instrument Monopolies

For the average American household, the primary vehicle for building equity is the family home. It is tangible, it is familiar, and it feels secure. Except that real estate is highly illiquid and susceptible to local market shocks. Where it gets tricky is that while the middle class has its net worth tied up in brick and mortar, the top 1% has systematically monopolized financial instruments. We are talking about corporate equities, mutual funds, private equity stakes, and sophisticated debt securities that generate compounding returns while their owners sleep. People don't think about this enough: a house requires maintenance, insurance, and property taxes, whereas a diversified portfolio of stock tickers feeds itself on global economic growth without needing a new roof.

The Great Asset Divide: Where the Top 1 Percent Dominates

If you want to see where the economic tectonic plates truly fracture, you have to look directly at the stock market. According to recent data from the Federal Reserve, the richest 1% of Americans own approximately 49.9% of all corporate equities and mutual fund shares in the country. Let that number sink in for a second. The bottom 50% of the population combined controls just about 1.1% of that exact same stock market. This monumental imbalance means that whenever Wall Street rallies or a tech giant in Silicon Valley beats its quarterly earnings expectations, the financial windfall bypasses the vast majority of American living rooms entirely and flows straight into the vaults of the ultra-elite.

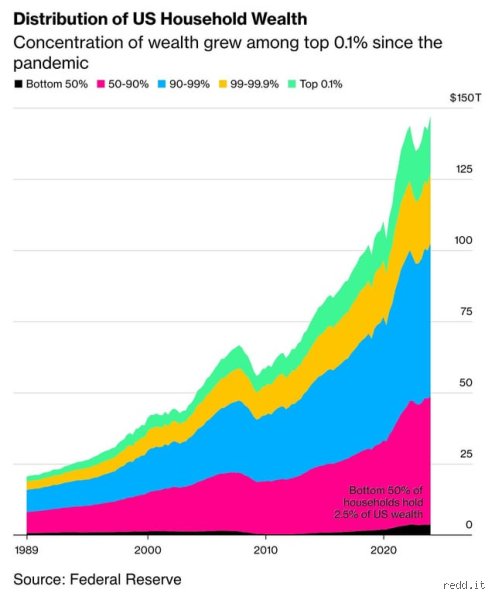

Billionaires, Corporate Equity, and the Pandemic Windfall

The trajectory of this concentration went into hyperdrive during the early 2020s. During the economic upheaval of the COVID-19 pandemic, the wealth held by billionaires in the United States increased by an astonishing 70%. It was the steepest increase in billionaires' share of wealth on record, transforming the top 0.1% into an economic force reminiscent of the Gilded Age. Think about names like Jeff Bezos or Elon Musk, whose personal fortunes fluctuated by tens of billions of dollars in a single afternoon based purely on stock market volatility. Yet, the issue remains that this hyper-wealth is not just a collection of luxury yachts and mega-mansions; it is functional command over the productive capital of the entire nation.

The Disappearance of Closely Held Private Businesses

Beyond public stocks, the top tiers of wealth dominate private business equity as well. The local manufacturing plant, the multi-state logistics firm, the private tech startup before its initial public offering—these are heavily concentrated in the upper echelons of net worth. But wait, aren't small businesses the backbone of the American dream? Technically, yes, but the scale of ownership is vastly unequal. The top 10% of households control more than 75% of total private business equity, which explains why the gap between corporate executives and the frontline labor force continues to widen at an exponential rate.

The Forgotten Majority and the Reality of the Bottom 50 Percent

At the opposite end of this financial spectrum lies a completely different universe inhabited by roughly 165 million Americans. The bottom 50% of households hold a collective net worth of just over 10 trillion dollars, compared to the nearly 56 trillion dollars held by the top 1% alone. This means the average personal wealth of someone in the top 1% is more than a thousand times greater than that of an individual in the bottom half of the country. And honestly, it's unclear how this gap can be bridged under current economic structures without massive, systemic policy interventions.

Debt Secularization and the Liquidity Trap

While the wealthy accumulate appreciating assets, the lower half of the population primarily accumulates liabilities. Household debt in the United States has soared over the past two decades, climbing from 8.29 trillion dollars in 2004 to over 18.8 trillion dollars. Most of this is housing debt, but credit card balances have crossed the 1.28 trillion dollar mark, and student loans sit heavily at 1.66 trillion dollars. As a result: instead of saving to purchase assets that grow, a massive portion of the population is trapped in a cycle of servicing high-interest debt that actively drains their monthly disposable income.

Social Security, Government Benefits, and the Alternative Wealth Metrics

Now, this is where conventional economic wisdom gets turned on its head, and experts disagree fiercely on how to measure the true distribution of economic security. Some prominent economists argue that traditional marketable-wealth metrics are fundamentally flawed because they completely ignore non-marketable assets. What happens when you factor in the present value of future Social Security benefits or defined-benefit government pensions? A landmark study published in the Journal of Finance revealed that when accrued Social Security benefits are included in household wealth calculations, the top 1% share actually drops from its standard market metric down to just under 24% over recent decades. That changes everything, or at least it shifts the perspective from raw capital ownership to lifelong consumption smoothing.

The Argument for Marketable vs. Defined-Benefit Assets

But we're far from it being a settled debate. I take the stance that while factoring in Social Security provides a more nuanced picture of retirement security, it fundamentally misrepresents what economic power actually means in a capitalist society. You cannot borrow against your future Social Security check to fund a new tech startup. You cannot pass your public pension down to your grandchildren to give them a debt-free Ivy League education or a down payment on a house in Aspen. Hence, marketable wealth—the kind you can buy, sell, leverage, and inherit—remains the ultimate metric for measuring true financial dominance and systemic control over the American economic landscape.

Common Misconceptions Surrounding the Distribution of Capital

The Illusion of the Real Estate Equalizer

Many citizens believe their primary residence acts as the ultimate counterweight to billionaire dominance. It does not. While the middle class ties up over 70% of its net worth in primary residential property, the ultra-wealthy view housing as a minor asset category. They buy equities. The richest 1% control over half of all corporate equities and mutual fund shares, leaving everyday homeowners holding illiquid brick and mortar while the stock market mints astronomical fortunes. Let's be clear: your house is a place to sleep, not a vehicle to overtake the top tier.

The Myth of Total Mobility

We love a good rag-to-riches story. But the data paints a vastly different picture of who owns most of America's wealth today. Horizontal mobility has stagnated. Economists track the elasticity of intergenerational income, revealing that nearly 50% of a parent's financial status is inherited by their children in the United States. Do people climb the ladder? Of course. Yet, the systemic inertia means the demographic composition of who owns most of America's wealth remains remarkably rigid across generations, favoring dynastic accumulation over raw merit.

Confusing High Salaries with Actual Net Worth

High-earning professionals like surgeons or corporate lawyers often look rich. Except that income is not capital. A surgeon earning $500,000 annually might spend heavily on lifestyle, taxes, and student loans, leaving them with surprisingly low permanent reserves. Wealth is what you keep, not what you broadcast. The truly dominant asset holders often show minuscule taxable income because their fortunes grow via unrealized capital gains, which avoids regular income taxation entirely.

The Hidden Reality of Private Equity and Non-Public Assets

Where the Elite Really Hide Their Trillions

Public stock markets are highly visible, but the real divergence happens in dark pools and private equity markets. The general public can easily track the S&P 500. However, the richest families funnel their excess liquidity into exclusive venture funds, private credit instruments, and hedge funds that require a minimum investment of $5 million just to enter the room. This creates an insular ecosystem of compounding growth. What chance does a standard savings account have against institutional-grade private placements? The issue remains that the average investor is legally barred from these high-yield playgrounds due to accreditation rules, which explains why the wealth gap widens even during public market downturns.

Expert Strategy: Shifting the Focus from Wages to Equity

If you want to change your financial trajectory, stop focusing solely on your salary. Wealthy individuals optimize for equity ownership and asset location. (Even a tiny slice of business ownership beats a decade of loyal labor.) To alter who owns most of America's wealth on an individual scale, we must democratize access to fractional business ownership and utilize tax-advantaged vehicles to their absolute limits, rather than relying on traditional banking products that lose purchasing power to inflation.

Frequently Asked Questions

Does the top 1% own more than the entire middle class?

Recent federal reserve data confirms that the top 1% of households hold roughly 30% of total national wealth, an amount that effectively rivals or surpasses the aggregate holdings of the entire middle 60% of the population. This specific cohort has seen its share escalate dramatically since the late twentieth century, driven by unprecedented gains in corporate equities and private business valuations. Meanwhile, the bottom 50% of Americans collectively control just about 2.5% of the economic pie, illustrating an intense concentration at the absolute apex of the financial pyramid. As a result: the structural divide between capital owners and wage earners continues to stretch to historic proportions.

How does inflation affect who owns most of America's wealth?

Inflation acts as a regressive tax that disproportionately punishes the lower and middle classes while frequently enriching the top asset holders. Because poorer households hold their limited reserves in cash or checking accounts, rising prices rapidly erode their actual purchasing power. Conversely, the wealthy own inflationary hedges like commercial real estate, commodities, and corporate equity, all of which appreciate in nominal value as consumer prices climb. In short, inflation transfers purchasing power away from wage earners directly into the hands of those who already possess tangible, cash-producing assets.

Will generational inheritance change the concentration of US assets?

The impending Great Wealth Transfer will see older generations pass down an estimated $84 trillion over the next two decades, but this historic shift will largely reinforce existing inequalities rather than leveling the playing field. Because this massive volume of capital is already concentrated within affluent households, the vast majority of these inheritances will flow directly to heirs who are already financially secure. A tiny fraction of the population will receive life-altering fortunes, while the average citizen receives little to nothing. This dynamic ensures that the current architecture of asset ownership will persist, keeping the baseline power structure firmly intact for the foreseeable future.

A Paradigm Shift in Economic Sovereignty

The current trajectory of American capital distribution is mathematically unsustainable for a stable democracy. We have constructed an economic apparatus where money breeds money with effortless autonomy, while human labor is taxed at higher rates and squeezed by systemic inflation. This is not a sustainable blueprint for long-term national prosperity. If we continue to tolerate a system where a handful of boardrooms dictate the material realities of millions, the foundational concept of the American Dream becomes an ironic relic. True systemic resilience requires bold policy intervention, specifically targeting tax codes and asset democratization. We must actively choose whether our economy exists to serve the consolidation of dynastic empires or the empowerment of the broader populace.