The Historical Context of the 90% Rule in Leasing and the ASC 840 Framework

To understand how we arrived at this hyper-specific calculation, we have to look back at the era of FASB Statement No. 13, which later mutated into ASC 840 in the United States. Before these rules took teeth, airlines, shipping conglomerates, and retail giants routinely kept thousands of delivery vehicles, Boeing jets, and storefronts off their balance sheets entirely. They argued that because they did not legally own the property, the future payments were just operational expenses.The Four-Test Gateway to Capitalization

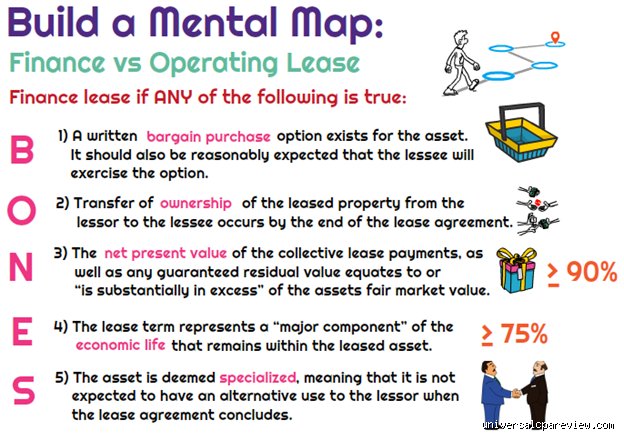

Regulators got tired of the hide-and-seek. They established four bright-line tests to classify a lease as a capital lease. The first three were straightforward enough: automatic transfer of ownership, a bargain purchase option, or a lease term spanning 75 percent or more of the asset's economic life. But where it gets tricky is the fourth test—our infamous 90% rule in leasing. If a tech company in San Francisco leased a server farm in 2015 worth $2,000,000, and the contractual payments, when discounted using their incremental borrowing rate, totaled $1,805,000, they crossed the line. Boom. Capital lease. The asset and the corresponding debt landed squarely on the balance sheet, destroying their debt-to-equity ratios overnight.Why Accountants Played a Dangerous Game of Cat and Mouse

The issue remains that human nature despises a rigid boundary, meaning corporate treasurers spent decades reverse-engineering contracts just to hit 89.9%. If they could shave off a fraction of a percent through creative structuring—perhaps by shifting maintenance costs or tinkering with the residual value guarantee—the lease remained safely tucked away in the footnotes of the financial statements. I find it fascinating how much intellectual energy was wasted on this. It was a game of financial engineering where the goal wasn't operational efficiency, but rather the preservation of a pristine, debt-free balance sheet.The Mechanics of the 90% Calculation: Peeling Back the Financial Algebra

Let us look at how this math actually functions because people don't think about this enough until an auditor is breathing down their neck. The calculation relies entirely on a concept called the Present Value of Minimum Lease Payments (PV of MLP). You cannot simply add up the monthly checks you write to the leasing company; instead, you must discount those future cash outlays back to the present day using a specific interest rate.Choosing the Discount Rate: The First Operational Hurdle

This is where the math gets highly subjective. A lessee must use its incremental borrowing rate unless they happen to know the implicit rate the lessor used to calculate the payments, and honestly, it's unclear why lessors would willingly hand over their profit margin data. Let us say a logistics firm in Chicago wants to lease a fleet of 50 freight trucks on January 1, 2018. The total fair market value of the fleet is $5,000,000.The math requires calculating the present value of those monthly payments over a five-year term. If the logistics firm uses a discount rate of 6.5 percent, the present value might come out to $4,450,000. Divide that by the $5,000,000 purchase price, and you get exactly 89 percent. They escaped the capital lease trap by a hair. But change that discount rate to 5.5 percent? The present value climbs, the ratio hits 91 percent, and suddenly that changes everything.

What Actually Counts as a Minimum Lease Payment?

But what gets included in that calculation? It is not just the base rent. Accountants must include any guaranteed residual values, non-refundable deposit fees, and even penalties for failure to renew. Except that they exclude executory costs like insurance, taxes, and routine maintenance. Because of this distinction, smart corporate negotiators often convinced lessors to bundle heavy maintenance packages into the lease contract, artificially lowering the base rent component to ensure the 90% rule in leasing was never triggered.The ASC 842 and IFRS 16 Revolution: Did the 90% Rule Survive?

Then came the great accounting earthquake of 2019. The Financial Accounting Standards Board (FASB) released ASC 842, while the International Accounting Standards Board (IASB) unleashed IFRS 16. The explicit goal was simple: eliminate off-balance-sheet financing once and for all.The Illusion of the Eliminated Rule

If you ask a superficial spreadsheet-jockey today, they will tell you the 90% rule in leasing is dead. They are wrong, or at least, we're far from it in American accounting. While IFRS 16 completely abandoned the distinction for lessees—forcing virtually all leases onto the balance sheet as Right-of-Use (ROU) assets—ASC 842 took a more conservative, dual-model approach. The old 90% rule in leasing was technically removed as a strict "bright-line" test. The new language states that a lease is a finance lease if the present value of lease payments amounts to "substantially all" of the fair value of the underlying asset.The Substantially All Loophole and the 90% Reality

But guess what? In the implementation guidance, FASB explicitly noted that 90 percent is still a safe harbor. So, while the words changed to sound more principles-based, the actual practice remained identical; most American auditors still use 90 percent as the threshold for "substantially all." It is a classic bureaucratic re-branding. The rigid wall became a heavy velvet curtain, yet the boundary lines remain virtually identical for corporate America.Comparing Operating and Finance Leases Under the 90% Framework

To truly grasp why companies fight so hard over this 90% rule in leasing, we have to look at the violent divergence in how these two lease types impact a company's income statement and cash flow metrics.An operating lease results in a straight-line expense. Every month, you pay the rent, you record a single expense line item, and your EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) takes a direct hit. It is clean, predictable, and penalizes your operational metrics from day one.

A finance lease—triggered by crossing that 90% rule in leasing threshold—is an entirely different beast. Because the transaction is treated as an asset purchase funded by debt, the lessee does not record rent expense. Instead, they record amortization on the ROU asset and interest expense on the lease liability. As a result: your EBITDA suddenly looks spectacular because interest and depreciation are excluded from that metric. Yet, your net income in the early years of the lease is severely depressed because interest expenses are front-loaded. Which explains why a Chief Financial Officer might fight tooth and nail to fail the 90% test if their executive bonus is tied directly to EBITDA targets, even if it means cluttering the balance sheet with millions in new liabilities. Experts disagree on which method reflects true economic reality, but the tactical manipulation of these numbers is an open secret in corporate finance.Common Mistakes and Misconceptions Regarding the 90% Rule in Leasing

Treating the Threshold as a Target Instead of a Hard Boundary

Lessees often misjudge the mathematical gravity of the 90% rule in leasing. They orchestrate payments to hover precisely at 89.9%, assuming this narrow safety margin guarantees operating lease treatment under older framework logic or specific tax structures. That is playing with fire. A minor tweak in the incremental borrowing rate during audits collapses this house of cards instantly. The problem is that lease classification demands pristine mathematical accuracy, not wishful thinking. If your calculations fail to account for escalating maintenance fees buried in the contract, you will breach the barrier. Boom. Your off-balance-sheet asset transforms into a glaring right-of-use asset and a corresponding liability overnight.

Ignoring Retrospective Adjustments and Variable Escalations

But what happens when inflation strikes? Many corporate treasurers erroneously believe the initial test dictates the accounting path for the entire duration of the contract. Except that modifications, index adjustments, or simple renewals trigger mandatory recalculations under modern IFRS 16 and ASC 842 regimes. You cannot just set it and forget it. Variable payments tied to a consumer price index might seem harmless initially. Yet, the moment those variables stabilize into fixed minimum payments due to contract amendments, the entire equation shifts. Failing to reassess the present value of minimum lease payments against the fair market value will distort your financial statements completely.

Confusing Useful Life with Economic Obsolescence

Let's be clear: the 75% useful life test and the 90% rule in leasing are distinct beasts that frequently get conflated. A machine might physically endure for twenty years. However, if its economic utility to your specific operation terminates after five years, structuring a lease based on the longer timeline is a administrative blunder. Accountants sometimes look at the physical asset rather than the contractual reality. This oversight results in misclassified agreements, skewing key debt-to-equity ratios and surprising stakeholders during annual reviews.

The Hidden Trigger: How Residual Value Guarantees Warp the Math

The Dangerous Allure of Lessor Deception

Here is a little-known aspect that slick asset salesmen rarely mention during negotiations. Lessors routinely use residual value guarantees to shift downside risk onto your balance sheet while keeping monthly payments deceptively low. Why does this matter? Because that guarantee counts heavily toward the minimum lease payments. You think you are signing a flexible, low-cost operating agreement. In reality, that backend promise inflates the present value calculation, pushing the total aggregate over the threshold. It is a brilliant trap for the unwary corporate buyer.

Expert Strategy: Unbundling Non-Lease Components

How do you fight back against this structural inflation? Smart financial executives aggressively unbundle non-lease components from the core contract. If a $150,000 equipment lease includes maintenance, insurance, and operational training, you must separate those service costs immediately. Do not let the total invoice dictate your accounting path. By isolating the pure asset rental cost, the present value drops significantly, keeping you safely below the classification trigger. Which explains why meticulous contract dissection is the ultimate weapon for preserving balance sheet flexibility.

Frequently Asked Questions

How does the 90% rule in leasing operate under ASC 842 compared to older accounting standards?

Under the historical ASC 840 standard, failing the 90% rule in leasing meant an automatic classification as a capital lease. The modern ASC 842 framework removes these rigid, bright-line percentages for classification, replacing them with a more holistic judgment regarding whether the lessor transfers substantially all economic value. However, most American corporate entities still utilize the 90% criteria as a practical expedient or explicit internal benchmark to ensure audit consistency. For instance, a firm managing 500 equipment contracts will retain the quantitative 90% cutoff to prevent subjective, time-consuming assessments by external auditors. As a result: the math remains virtually identical in daily corporate practice, even if the regulatory verbiage shifted toward qualitative terminology.

Can a lease agreement trigger the 90% threshold if the initial asset value is unknown?

Determining the precise fair market value of highly customized industrial machinery is notoriously difficult, which complicates the 90% rule in leasing calculations. When the fair value is unavailable, you must leverage internal production costs or independent third-party appraisals to establish a baseline. For example, if a specialized medical scanner costs approximately $1.2 million to manufacture, your total lease payments over a four-year term cannot exceed a present value of $1.08 million without triggering finance lease classification. What happens if you guess wrong? The issue remains that regulatory bodies will penalize companies that use artificially inflated fair value estimates to intentionally bypass capitalization requirements.

What are the direct financial consequences if an audit proves you violated the 90% rule in leasing?

If an IRS or SEC audit determines that your $5,000,000 fleet lease actually breached the 90% threshold, the financial repercussions are immediate and painful. You will be forced to restate prior period earnings, moving those expenses from simple operating rental deductions straight into depreciation and interest schedules. This structural shift instantly alters your EBITDA metrics, potentially triggering catastrophic technical defaults on existing bank covenants that restrict debt-to-equity ratios. Furthermore, your corporate tax liabilities could surge if depreciation schedules do not align perfectly with the newly mandated asset amortization timeline. Can your current corporate capital structure withstand a sudden, unexpected multi-million-dollar debt inclusion on the public balance sheet?

A Definitive Stance on Lease Optimization

Relying blindly on narrow mathematical loopholes to hide liabilities is a outdated corporate strategy that belongs in the previous century. The 90% rule in leasing should never be treated as an administrative game of hide-and-seek with regulatory authorities. Instead, forward-thinking financial leaders must embrace total balance sheet transparency, focusing on true operational utility rather than artificial accounting engineering. If an asset is vital enough to consume nearly the entirety of its economic value during the contract, businesses should boldly own the asset or explicitly classify it as a finance arrangement. Attempting to skirt the perimeter of this regulation through convoluted contract clauses only invites aggressive audit scrutiny, destroys investor trust, and complicates internal reporting. True financial agility is achieved through clear asset management, not through clever mathematical evasion.