The Day the Ledger Changed: Demystifying the Core Definitions of Accounting Adjustments

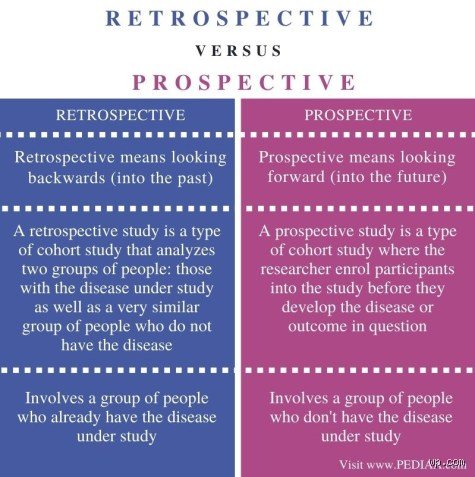

Imagine waking up to discover that every coffee you bought over the last decade must now be capitalized as a long-term asset rather than expensed immediately. That is the chaotic reality corporate finance teams face when accounting bodies shift the goalposts. When we look at retrospective application, we are talking about full-blown financial time travel. The company adjusts the opening balance of retained earnings for the earliest period presented, dragging old numbers into a new reality. I find it fascinating how much faith we place in historical data, considering it can be legally rewritten with the stroke of a regulator's pen.

Rewriting History via the Retrospective Approach

Because consistency is the bedrock of market analysis, standard-setters usually default to this method. If a firm changes its inventory valuation from First-In, First-Out (FIFO) to Weighted-Average Cost, comparing last year's performance with this year's becomes a farce without retrofitting the old data. The accounting team must physically go back, recalculate the Cost of Goods Sold (COGS) for 2024 and 2025, and restate those prior-year columns in the current 2026 report. Why go through this torture? Investors demand a seamless trend line, yet it forces companies to spend millions on forensic accounting just to change an internal metric.

Looking Ahead: The Philosophy of Going Prospective

Then comes the pragmatic escape hatch. Under prospective treatment, you do not touch the ghosts of your financial past. The historical figures remain safely locked in their graves. You implement the new policy on day one, and everything moving forward reflects the updated rule. It is a clean break, favored heavily when reconstructing the past proves to be an expensive mathematical impossibility.

Where It Gets Tricky: Navigating IFRS and US GAAP Triggers

The regulatory framework dictated by the International Accounting Standards Board (IASB) via IAS 8—and its American cousin, ASC 250—establishes rigid guardrails for when you must look back or look forward. Companies cannot just choose a path based on what makes their earnings per share look prettier this quarter. The issue remains that a clear distinction must be made between a formal change in accounting policy and a mere change in accounting estimate. The former demands retrospective correction, except when it is completely impracticable; the latter explicitly mandates prospective treatment.

The High Stakes of a Policy Shift

A voluntary change in accounting policy requires a company to prove that the new method provides more reliable and relevant information. Think about the transition of a major tech conglomerate switching its revenue recognition model for cloud subscriptions. When software giants adjusted to the sweeping IFRS 15 guidelines, the impact was monumental. Billions of dollars in deferred revenue suddenly had to be pulled forward or pushed back across multiple fiscal years. In short, the backward-looking adjustment rewrote the historical growth trajectory of entire tech sectors.

The Pragmatic Softness of Estimates

Estimates are different because they are inherently slippery. You guess how long a factory machine will last—say, 10 years—and then 4 years later, you realize new technology makes it obsolete in 2 more. That is a change in estimate. You do not rewrite the depreciation expense for the last 4 years; you simply accelerate it over the remaining 2. Experts disagree on whether this creates an easy loophole for earnings management, but honestly, it is unclear how else we could manage the fluid nature of business without breaking the system entirely.

The Financial Mechanics: How Retroactive Adjustments Reshape the Balance Sheet

Let us look at a concrete corporate scenario to see how this plays out in the trenches. Suppose a manufacturing firm based in Ohio decides to change its method of accounting for long-term construction contracts in January 2026. Previously, they used a method that delayed revenue recognition until project completion, but now they are moving to the percentage-of-completion method to better align with industry peers.

The Domino Effect on Retained Earnings

The transition requires a surgical strike on the equity section of the balance sheet. If the firm had three active multi-year contracts in 2024, the revenue recognized under the new policy would have been $4.5 million higher than what was originally reported. Because that money was technically earned in the past, it cannot be dumped into the 2026 income statement. That changes everything. The accountants must increase the opening balance of Retained Earnings on January 1, 2026, by that amount, net of a 21% corporate tax rate adjustment. Consequently, the prior-year comparative columns for 2024 and 2025 are restated in the annual report, completely shifting the baseline that Wall Street analysts used to evaluate the company's historical efficiency.

The Impracticability Exception: The Ultimate Escape Valve

But what happens when the historical data is a black hole? The regulations offer a pass code: the impracticability exemption. If a company suffered a catastrophic server failure losing 2023 inventory logs, or if determining the historical effects requires assumptions about management's intent that cannot be verified, retrospective application is abandoned. As a result: the firm is permitted to apply the change prospectively from the earliest date workable. People don't think about this enough, but it creates a strange situation where a disorganized company with terrible record-keeping can sometimes escape the grueling burden of restatement that its meticulous competitor must endure.

Side-by-Side Reality: Comparative Impact on Financial Analysis

For an investor trying to value a business, these two methods create radically different landscapes. The choice between looking backward or marching forward alters key financial metrics, making a company look either remarkably stable or wildly volatile to the untrained eye.

Volatility vs. Continuity

Retrospective application preserves the holy grail of financial analysis: comparability. It ensures that when you calculate the compound annual growth rate (CAGR) of a firm's net income over a five-year period, you are comparing apples to apples. Yet, the cost is a sudden, sometimes jarring shift in the historical record. A company that looked like a steady compounder yesterday might suddenly appear cyclical today because past numbers were rewritten downwards. Prospective application offers the opposite trade-off; it protects the historical record from being altered, but it introduces a structural break in the timeline. The 2026 profit margin might look artificially inflated by 15% compared to 2025 simply because the accounting rule changed, we're far from a true operational improvement here.

Common blind spots and structural misconceptions

The phantom restatement trap

Many practitioners erroneously conflate a change in accounting estimate with a full structural revision. They are miles apart. When you deploy a retrospective application, you are effectively rewriting history as if the new policy had always been active since day one. The biggest blunder? Forgetting the tax ripple effects. Adjusting retained earnings without recalculating deferred tax assets creates a balance sheet asymmetry that auditors will instantly flag. You cannot simply patch the current year opening balances and hope the ghost of previous periods vanishes; retrospective and prospective application protocols require a rigorous, dual-entry recalculation for every single affected line item.

The "too difficult" escape hatch

But what happens when data disappears? Under frameworks like IAS 8 or ASC 250, companies often claim impracticability far too quickly to avoid the grueling labor of historic recreation. Let's be clear: laziness is not a legal justification for switching to a prospective application. To bypass retrospective treatment, you must prove that the historic information cannot be reconstructed even after making every reasonable effort, such as when a fire destroys localized physical ledgers or a newly acquired subsidiary lacks granular historical enterprise resource planning data. Otherwise, regulatory bodies will penalize the entity for non-compliance.

The hidden leverage of transitional provisions

Exploiting the choice window

Standard-setters frequently grant a hidden grace period during major policy overhauls. Standard setters like the IASB or FASB often embed specific transitional provisions within new pronouncements, allowing firms a explicit choice between the modified retrospective approach and full prospective rollout. Why does this matter? It dictates your short-term EBITDA trajectory. If you choose a retrospective application during an economic downturn, you might inadvertently artificially depress your historical performance metrics, making your current-period recovery look spectacularly dramatic by comparison. It is legal financial engineering at its finest, except that few financial analysts actually bother to read the dense footnote disclosures where these strategic choices are buried.

Frequently Asked Questions

How often do public companies invoke the impracticability exception for retrospective application?

Empirical financial data indicates that less than 4.5% of Accelerated Filers listed on major global exchanges actively invoke the impracticability exemption during major policy shifts. Regulatory scrutiny remains incredibly hostile toward this escape route because it disrupts the longitudinal comparability that global institutional investors demand. For instance, during the widespread adoption of comprehensive revenue recognition standards over the past decade, retrospective and prospective application choices skewed heavily toward modified historic restatements, with over 85% of firms choosing to absorb a one-time cumulative adjustment to opening retained earnings rather than fighting the regulatory bodies over data unavailability. The issue remains that proving a total absence of historical records requires an exhaustive forensic trail that most corporate legal departments prefer to avoid entirely.

Can a company simultaneously use both methods for a single accounting standard change?

No, you cannot arbitrarily slice a single accounting policy change into a hybrid cocktail of historical rewriting and forward-looking adjustments. The accounting frameworks mandate absolute methodological purity to prevent companies from cherry-picking favorable numbers out of past quarters while pushing liabilities into future horizons. Which explains why a business must apply the chosen transitional mechanism uniformly across all comparative periods presented within the financial package. If a firm adopts a new lease accounting standard, it cannot apply a prospective application to its domestic retail properties while using retrospective adjustments for its international manufacturing facilities. The structural integrity of the financial statements would collapse under the weight of such internal inconsistency.

What are the concrete impacts of these applications on a company's stock valuation?

The impact is immediate, psychological, and frequently volatile. When a mid-cap enterprise announces a retroactive adjustment that slashes its previously reported net income by a margin of 6% or more, algorithmic trading systems automatically trigger sell orders before human analysts can even read the explanation. Conversely, utilizing a forward-looking prospective application creates zero turbulence in historical trend lines, though it might introduce a sudden, unexplained drop in future quarterly margins that leaves investors feeling blindsided. As a result: savvy market participants generally penalize companies that frequently change estimates forward, viewing it as a sign of earnings manipulation or weak internal controls.

A definitive stance on financial transparency

We must stop treating these accounting mechanisms as interchangeable math exercises. The systemic bias toward forward-looking adjustments often serves as a convenient smokescreen for corporate executives who want to bury their past operational miscalculations under the rug of innovation. True financial transparency demands that we default to historical restatement whenever humanly possible, forcing organizations to own the trajectory of their past decisions. Yet, the corporate world continues to lobby aggressively for forward-looking treatments because it protects current stock valuations from the cold, harsh light of historical reality. In short: if you want to understand the true health of an enterprise, you must look at how aggressively they try to avoid looking backward.