Beyond the Safe Ledger: Demystifying the Ultimate Shock Absorbers

To grasp why these financial behemoths matter, you have to look at them as the insulation inside the walls of global capitalism. Reinsurance is quite literally insurance for insurance companies. When a primary insurer gets buried under an avalanche of claims after a catastrophic earthquake or a systemic supply-chain collapse, they do not face insolvency alone. Instead, they cede a portion of their risk liabilities, alongside a corresponding slice of their premium revenue, to wholesale corporate entities. This institutional mechanism prevents a localized catastrophe from triggering a domino-style meltdown across retail banking and commercial real estate sectors.

The Statistical Anchor of the Global Underwriting Sandbox

The entire global marketplace relies on a surprisingly concentrated pool of capital. Recent industry data compiled by rating agency AM Best indicates that the top 50 global reinsurance groups control over ninety percent of the total market capacity. If you think the financial system is decentralized, think again. The top tier is an oligopoly. Within this exclusive bracket, the metrics used to measure corporate scale have recently undergone a massive bureaucratic upheaval. For decades, analysts compared these entities using gross written premiums. That era is dead. Today, the institutional divergence between accounting metrics has turned simple corporate comparisons into an absolute statistical minefield.

The Accounting Schism: How Swiss Re and Munich Re Fractured the Leaderboard

Where it gets tricky is the implementation of the new international financial reporting standard, specifically known as IFRS 17. This regulatory framework completely overhauled how insurance contracts are measured and presented on corporate balance sheets. Instead of utilizing traditional premium metrics, compliant organizations must now report gross reinsurance revenue, a metric that reflects the actual services provided during the fiscal period rather than cash collected up front. This technical pivot caused an immediate structural shakeup at the summit of global finance. It fundamentally reordered the traditional leaderboard and sparked fierce debate among equity analysts.

The Statistical Coup of the Zurich Titan

The numbers tell a story of ruthless corporate maneuvering. Following its formal adoption of the IFRS 17 regime, Swiss Re claimed the absolute number one spot for compliant global reinsurers by posting a staggering $36.2 billion in gross reinsurance revenue. This pushed the Zurich-based institution past its historic Bavarian rival. Munich Re dropped down to the second position on this specific ledger, registering a highly competitive $32.6 billion in reinsurance revenue. Honestly, it's unclear whether this ranking will remain permanent or flip back next quarter. The currency fluctuations between the Euro and the Swiss Franc can alter these positions overnight, meaning we are far from a settled, permanent hierarchy.

Munich Re's Efficiency Counterpunch

But gross volume is a deceptive metric if you ignore the actual underlying profitability of the underwriting portfolio. While Munich Re slipped to the second slot in raw revenue, its operational performance was nothing short of a masterclass in risk selection. The German powerhouse recorded an astonishing non-life reinsurance combined ratio of 77.3%. For those unfamiliar with insurance math, a combined ratio below 100% indicates underwriting profitability; the lower the number, the cleaner the operation. Swiss Re, by comparison, tracked behind with a less efficient combined ratio of 85.2%. People don't think about this enough: would you rather possess the largest top-line revenue or the most profitable bottom line? I would choose the latter every single time.

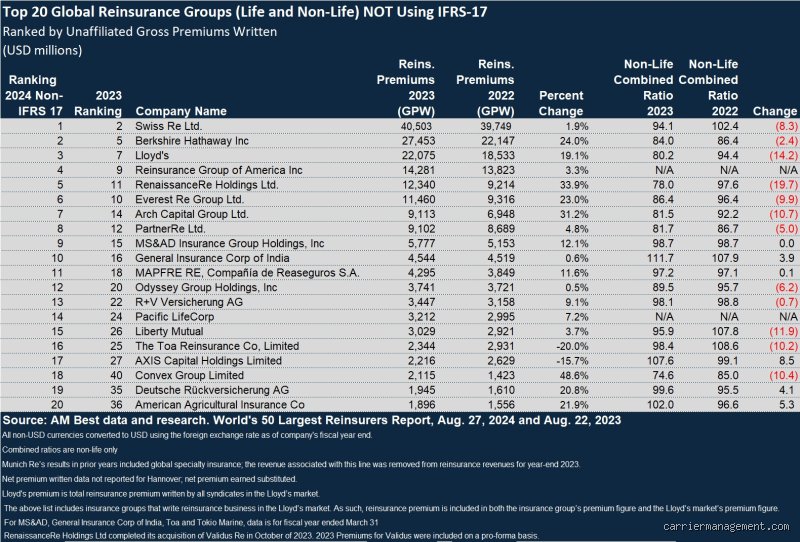

The Unregulated Contenders: Berkshire Hathaway’s Shadow Empire

The plot thickens when we look across the Atlantic. Because US-based corporations operate under domestic GAAP principles rather than international standards, AM Best was forced to bifurcate its global rankings into two completely separate corporate tracking lists. This technical division allowed Warren Buffett’s Omaha-based conglomerate, Berkshire Hathaway Insurance Group, to officially claim the undisputed title of the largest non-IFRS 17 reinsurer in the world. Berkshire reported a monstrous $26.9 billion in gross written reinsurance premiums. That changes everything because Buffett handles liquidity differently than anyone else in Europe.

The Incomparable Power of the Omaha Float

Comparing a European giant like Swiss Re to Berkshire Hathaway is like comparing a traditional naval battleship to a nuclear submarine; they operate in entirely different ecosystems. Berkshire does not view reinsurance simply as a fee-generation business. Instead, it treats the massive influx of upfront premium cash—famously termed the float—as a low-cost capital engine to fund aggressive corporate acquisitions and public equity investments. Supported by an unimaginable pool of total adjusted shareholders' funds exceeding $272 billion, Berkshire can comfortably underwrite massive, volatile property catastrophe risks that would cause smaller European boardrooms to instantly panic. Yet, they remain structurally distinct from their continental peers who must satisfy rigid European regulatory capital regimes.

The Tier-Two Chasers: Mapping the Contenders for the Crown

Directly underneath the big three, a relentless battle for market share is unfolding among secondary players. Germany’s Hannover Re firmly occupies the third position on the IFRS 17 leaderboard, generating a very substantial $27.5 billion in annual reinsurance revenue. They have successfully carved out a highly profitable niche by acting as a lean, transaction-focused partner to primary carriers, eschewing the massive administrative overhead that bogs down its larger neighbors. Further down the list, French multinational SCOR SE holds the fourth spot within the European cohort, though they have recently faced headwinds, showing an average capital surplus decline of 3.8% alongside China Reinsurance Group.

The Alternative Hubs and the Rise of Bermuda

The traditional dominance of continental Europe is also facing structural pressure from alternative capital havens and specialized specialty hubs. Consider the unique marketplace of Lloyd’s of London, which brought in $23.5 billion in gross written premiums through its distributed syndicate network. Meanwhile, the mid-tier market is dominated by agile Bermudian players like Everest Group, which pulled in $12.9 billion, and RenaissanceRe, which recorded an impressive 32.4% surge to reach $11.7 billion in gross written premiums. This shifting corporate landscape proves that while the absolute largest reinsurer in the world might sit in Zurich or Munich, the geopolitical center of gravity for risk placement is becoming increasingly fragmented.

Common mistakes and widespread misconceptions

People love a simple leaderboard. Gross written premiums usually dictate who wears the crown in global insurance rankings, yet this metric paints an incomplete picture. If you look solely at the top line, Munich Re and Swiss Re perpetually trade the top spot like a game of musical chairs. The problem is that premium volume does not equal risk retention or economic reality. For instance, some companies write massive amounts of business only to retrocede—basically, reinsure the reinsurer—a huge chunk of it away. Are they truly the largest reinsurer in the world if they do not hold the ultimate risk? Let's be clear: size is a shape-shifter in this industry.

The premium volume illusion

We often conflate revenue with actual market dominance. In 2024, Munich Re reported gross premiums in its reinsurance segment exceeding 45 billion Euros, which leads many analysts to instantly proclaim it the undisputed heavyweight. Except that Swiss Re occasionally edges them out depending on how currency fluctuations between the Euro and the Swiss Franc shake out. Because exchange rates fluctuate wildly, the title of world's largest reinsurer can change on paper without a single new policy being signed. It is a corporate optical illusion. Relying purely on premium volume ignores the strength of a company's balance sheet and its net asset value.

Ignoring the Bermuda and alternative capital engines

Another massive oversight is ignoring players like Berkshire Hathaway or the swelling tide of insurance-linked securities (ILS). Warren Buffett’s National Indemnity carries colossal amounts of capital, allowing it to take on single risks that would make European giants tremble. Yet, because their traditional premium influx looks different, traditional metrics skip them. Do you really think a company with less premium volume but double the capital cushion is smaller? The issue remains that traditional ranking systems fail to capture these non-traditional capital pools, which now control over 100 billion dollars globally.

The hidden engine of retrocession and expert advice

To truly understand who holds the power, we must look at the hidden architecture of the market. Reinsurers do not just sit on risk; they pass it along. This is the shadowy world of retrocession.

The secret safety valve of global finance

The largest reinsurer in the world is never fully exposed to a single catastrophic event. They slice, dice, and distribute their liabilities across a global network of smaller entities and capital market investors. Why should you care about this? If you are evaluating the stability of these mega-corporations, you need to look at their net retained premium, not just the gross figure. My advice to anyone analyzing this space is to look at the enterprise's capital adequacy ratio under Solvency II frameworks rather than public relations press releases. Munich Re consistently maintains a solvency ratio well above 240 percent, which explains why they retain their stellar reputation even during years plagued by unprecedented hurricanes and wildfires. It is the fortress-like balance sheet, not the marketing brochure, that matters.

Frequently Asked Questions

Who officially ranks as the largest reinsurer in the world today?

According to the authoritative annual rankings managed by credit rating agency A.M. Best, Munich Re consistently clinches the number one spot based on total global reinsurance gross premiums written. Their reinsurance revenue alone hovered around 47 billion dollars in recent reporting cycles, comfortably keeping them ahead of their closest rival, Swiss Re, which locked in approximately 40.5 billion dollars. Hannover Re sits firmly in the third position globally, while the French powerhouse SCOR rounds out the top tier of traditional European capacity. Consequently, while the order can shift slightly due to macroeconomic shocks, the Munich-based titan remains the heavy champion of the global risk transfer market.

How do fluctuating currency exchange rates impact these global rankings?

The global reinsurance industry operates across multiple economic zones, meaning that reported financial results are highly sensitive to the strength or weakness of the US dollar against the Euro and the Swiss Franc. When the Euro depreciates against the dollar, Munich Re's reported volume can artificially shrink in American analytical reports, giving the false impression that its market share is contracting. Conversely, a surging Swiss Franc can instantly inflate Swiss Re's financial metrics on the international stage. As a result, savvy industry observers look at constant-currency growth rates rather than converted dollar values to determine who is truly expanding their footprint.

What role does Berkshire Hathaway play in the global reinsurance hierarchy?

Berkshire Hathaway is the wild card of the international insurance ecosystem because it operates with a completely different philosophical playbook compared to its European peers. Instead of focusing on steady, incremental premium growth year after year, Warren Buffett utilizes his massive 160 billion dollar cash hoard to selectively underwrite massive, bespoke super-catastrophe bonds when prices are high. They might rank lower in premium volume during soft market cycles, but their financial muscle allows them to absorb losses that would bankrupt smaller entities. In short, they represent the ultimate backstop of the global financial system, functioning as a shadow giant that defies traditional ranking methodologies.

The final verdict on global risk dominance

Chasing a single, definitive name to crown as the absolute ruler of the reinsurance realm is a fundamentally flawed pursuit. Munich Re holds the statistical trophy for premium volume, yet the true metric of leadership in this volatile century is resilience rather than mere size. We are witnessing an era where climate change and systemic cyber threats are redefining the boundaries of insurability itself. The true champions will not be those who write the biggest checks for premium volume, but those who possess the intellectual machinery to price tomorrow's unpredictable catastrophes accurately. In the end, capital flexibility and underwriting discipline will always triumph over raw corporate scale.