The Anatomy of Concentration: Breaking Down the Core Definition

Regulators did not just pull the 10% benchmark out of thin air. Following the catastrophic fallout of the 2008 global financial crisis, the Basel Committee on Banking Supervision realized that traditional risk-weighted asset calculations were easily gamed by creative accountants. A bank could look perfectly capitalized on paper, but if three of its largest corporate borrowers went belly-up simultaneously, the institution would vanish overnight. That is exactly why the large exposure framework was overhauled. It functions as a hard, unyielding ceiling. It completely ignores internal risk models and looks at raw, nominal exposure because, when a black swan event hits, correlation breaks down and models lie.

The 25% Ultimate Limit and Capital Constraints

The absolute ceiling for any single large exposure is capped at 25% of a bank’s tier 1 capital. If you are dealing with Global Systemically Important Banks—the so-called G-SIBs like JPMorgan Chase or HSBC—the rules tighten even further to 15% when dealing with other G-SIBs. Why? Because the interconnectedness among these titans is terrifying. Think of it as a financial spiderweb where a twitch in New York snaps a thread in Frankfurt. If Bank A lends too much to Bank B, the entire system faces an existential threat.

What Counts in the Exposure Metric?

People don't think about this enough: an exposure is not just a standard corporate loan. The metric is a massive dragnet. It catches traditional drawn loans, undrawn committed credit lines, over-the-counter derivatives, and equity holdings. Even repo trades and securities financing transactions get thrown into the mix. It means treasury departments must constantly aggregate data across disparate trading desks globally, which explains why risk compliance is an expensive, automated nightmare.

The Connected Counterparty Conundrum: Where the Math Gets Sticky

Here is where it gets tricky. If a bank lends money to a parent company and its three subsidiaries, does that count as one large exposure or four separate ones? Regulators look at groups of connected clients through two distinct lenses: control relationships and economic interdependence. Control is relatively straightforward. If Company A owns more than 50% of Company B, they are married in the eyes of the risk department. But economic interdependence? That changes everything, and honestly, it's unclear where the boundaries lie until things start failing.

The Web of Economic Interdependence

If Borrower X buys 80% of its raw materials from Borrower Y, they are economically co-dependent. If Borrower X collapses, Borrower Y will likely default too. The Basel guidelines state that if one counterparty experiences financial problems, the other is likely to encounter repayment difficulties. Hence, the bank must group them together. Imagine a scenario where a regional bank in Ohio exposes itself to a major local automotive supplier and three independent logistics firms that only transport parts for that specific supplier. That is a single, massive concentration risk hiding in plain sight behind different corporate logos.

The Shadow Banking Blindspot

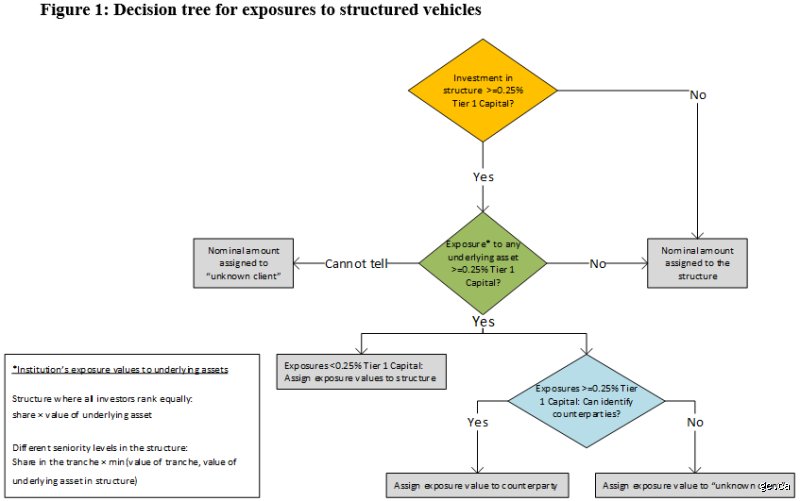

And then we have to talk about funds and securitization structures. When a bank invests in a collateralized loan obligation or an investment fund, it cannot just list the fund manager as the counterparty. It has to look through the structure to identify the underlying assets. If those underlying assets include companies the bank has already lent to directly, the exposures stack up. Yet, tracking this in real-time is nearly impossible, which is why I believe the current look-through mechanisms are fundamentally flawed and lagging behind the speed of modern shadow banking markets.

Regulatory Evolution: From Basel I to the Modern Framework

We have come a long way since the simplistic guidelines of the late twentieth century. Under early regulatory regimes, tracking a large exposure was a retrospective exercise, often calculated at the end of a fiscal quarter. Today, the rules mandated by the European Banking Authority through the Capital Requirements Regulation and the Federal Reserve in the United States require sophisticated, intra-day monitoring. The shift from total capital to eligible tier 1 capital as the sole qualifying capital base drastically reduced the allowable exposure amounts, forcing banks to trim their largest client relationships. As a result: corporate lending desks had to completely restructure how they syndicate massive loans to blue-chip conglomerates.

The Sovereign Debt Exception Paradox

But the issue remains that regulators still maintain blindspots. Sovereign bonds—debts issued by national governments—are frequently exempted from these strict limits, or assigned a 0% risk weight. We saw the absurdity of this during the Eurozone sovereign debt crisis in 2011, when Greek and Italian banks were stuffed to the brim with their own governments' bonds. Was that a safe investment? We're far from it. It was a massive, systemic large exposure that nearly brought down the entire monetary union, proving that political expediency often trumps economic logic when designing safety nets.

Measuring the Risk: Exposure at Default vs. Nominal Values

How do you actually calculate the value of an exposure when dealing with volatile financial instruments? For a standard loan, it is simple nominal value. But for a complex interest rate swap or a foreign exchange forward, the value changes with every tick of the market clock. Banks must utilize the Standardised Approach for Counterparty Credit Risk to calculate the exposure value of derivatives. This method factors in both the current replacement cost and the potential future exposure, adding a regulatory multiplier that acts as a buffer against market swings.

Credit Risk Mitigation and Netting Agreements

Can a bank lower its reported exposure? Yes, through legally enforceable bilateral netting agreements and eligible financial collateral. If a bank owes a hedge fund 100 million dollars in one trade but is owed 120 million dollars by the same fund in another, the net large exposure is 20 million dollars. But this only works if the legal framework holds up during a bankruptcy. If a court voids the netting clause during a sudden market meltdown—a nightmare scenario that keeps chief risk officers awake at night—the bank's gross exposure instantly balloons, potentially violating regulatory caps and triggering immediate market sanctions.

Common mistakes and misconceptions about concentrated credit risk

The illusion of collateral protection

Many risk officers sleep soundly because a massive credit facility is backed by prime real estate or liquid securities. This is a trap. When a systemic shock hits, asset correlations trend toward one. Suddenly, that flawless collateral vaporizes because everyone tries to liquidate the exact same underlying asset simultaneously. The reality of a large exposure is that collateral is a psychological cushion, not a bulletproof shield, during a true liquidity crunch.

Confusing a corporate group with independent entities

Can you spot the hidden connection between three seemingly unrelated mid-sized enterprises? If they share a single, unrated parent company hidden in an offshore jurisdiction, you are exposed to a singular, massive vulnerability. Failing to aggregate connected counterparties remains the premier rookie mistake in modern banking book management. The problem is that legal independence does not equal economic independence. Because when the mother ship sinks, the subsidiaries rarely survive the suction.

Ignoring the off-balance sheet iceberg

You checked the loan book twice, yet the risk dashboard looks perfectly green. Except that you completely forgot to calculate the committed, undrawn credit lines and complex interest rate swaps. Unfunded commitments frequently morph into massive cash drains during market panics. Let's be clear: a large exposure isn't just what a client owes you today, but what they could legally demand from you tomorrow morning when the entire financial system starts buckling.

Advanced mitigation: The synthetic relief valve

Moving beyond simple loan syndication

The traditional playbook dictates that when a single-name concentration breaches internal limits, you syndicate the excess to regional peers. But what happens if the secondary market is completely frozen? Enter credit default swaps and bespoke balance sheet securitization. By transferring the credit risk synthetically, banks can retain lucrative client relationships while keeping the actual capital consumption strictly below regulatory thresholds. Is it cheap? Absolutely not, but neither is an emergency capital injection from a predatory sovereign wealth fund.

Dynamic threshold setting via macroeconomic stress testing

Static limits are a relic of twentieth-century risk management. A concentration limit that feels perfectly safe during a macroeconomic boom can turn toxic within forty-eight hours of a geopolitical flare-up. Advanced risk architecture utilizes machine learning models to dynamically adjust your single-counterparty boundaries based on real-time credit spreads and macroeconomic leading indicators. It requires immense computational power, which explains why only the top tier of global financial institutions can actually pull this off effectively without crashing their core systems.

Frequently Asked Questions

What is the definitive regulatory threshold for a large exposure under Basel III framework?

Under the standardized Basel III framework, a banking institution must identify and report any counterparty relationship that equals or exceeds 10% of its Tier 1 capital. Furthermore, a strict statutory limit is enforced at 25% of Eligible Capital for any single counterparty or group of connected clients, though this cap drops sharply to 15% for Global Systemically Important Banks interacting with other G-SIBs. These strict quantitative guardrails prevent idiosyncratic failures from triggering a cascading domino effect across the international financial architecture, forcing institutions to diversify their asset allocations whether they want to or not.

How do sovereign debt holdings impact the calculation of single-name concentrations?

Sovereign bonds have historically enjoyed a privileged status, frequently receiving a comfortable 0% risk weight under standardized regulatory regimes worldwide. This preferential treatment encourages banks to accumulate massive piles of domestic government debt, effectively creating a dangerous sovereign-bank nexus that can implode during a localized fiscal crisis. The issue remains that a sovereign default, while statistically rare, instantly compromises the solvency of the entire domestic banking sector because these massive asset concentrations are rarely hedged adequately. As a result: risk managers must look past political rhetoric and establish internal economic capital limits for government exposures, regardless of what the official regulatory handbooks permit.

Can intraday payment flows accidentally trigger a concentration breach?

Yes, massive operational volumes moving through clearing houses can easily create temporary, unregistered spikes that vastly exceed standard overnight parameters. If a major clearing broker delays a settlement payment by even three hours, your intraday counterparty concentration can instantly skyrocket past 40% of available liquid equity. These transient spikes are often excluded from formal regulatory reporting, yet they represent a terrifying operational vulnerability that can paralyze a treasury desk during high-volatility trading sessions. In short, monitoring risk solely on an end-of-day basis is akin to checking your blind spot only after you have already changed lanes on a chaotic highway.

A definitive verdict on concentration risk

The continuous obsession with maximizing immediate return on equity keeps driving financial institutions straight back into the comforting, dangerous arms of oversized corporate relationships. We like to pretend that sophisticated mathematical models and complex hedging strategies can entirely neutralize the inherent danger of a massive, single-name concentration. They cannot. When the music stops, diversification is the only proven life jacket that actually functions, meaning that any institution prioritizing relationship politics over strict exposure limits is actively engineering its own demise. Let's stop treating concentration management as a tedious compliance box to be checked and start recognizing it as the ultimate test of survival. The next systemic crisis will not spare the brilliant optimists who believed their top client was simply too big, or too prestigious, to fail.