The Illusion of the Salary: Understanding the Partnership Legal Model

Most corporate ladder climbers assume that making partner means getting a massive salary bump, a nicer corner office, and a corporate credit card with no limits. But the thing is, Big 4 partners do not actually receive a salary at all. The day you drop your employee status and cross the threshold into the equity tier at a firm like EY or PwC, your legal relationship with the business transforms entirely because you become a self-employed business owner. Instead of a guaranteed monthly paycheck, you receive a draw against predicted profits. This shifts the financial risk directly onto your shoulders.

The Equity Point Matrix

Where it gets tricky is how those corporate profits are divided among the partnership rank and file. The firms use an intricate, internally guarded ranking system usually built on units or equity points. A newly minted partner might be allocated 100 points, while a veteran who has spent two decades embedding themselves into the executive suite of Fortune 500 giants might hold 1,000 points. When the financial year wraps up, the firm totalizes its net profit, calculates the cash value of a single point, and multiplies it by your personal allocation. It is a meritocracy on paper, yet navigating the system requires immense internal political maneuvering.

The Dark Side of the Promotion: The Capital Buy-In Requirement

People don't think about this enough, but becoming a joint owner means you have to buy your way into the shop. You do not just get handed your equity; you purchase it. Recent internal disclosures show that a fresh partner buy-in ranges between $150,000 and $750,000, depending entirely on the practice line and geographic market. How do people afford this? Most new partners end up taking massive, firm-facilitated bank loans to cover this capital requirement. Consequently, during your initial years, a hefty portion of your monthly cash draw goes straight toward servicing that debt and funding your self-employed tax obligations.

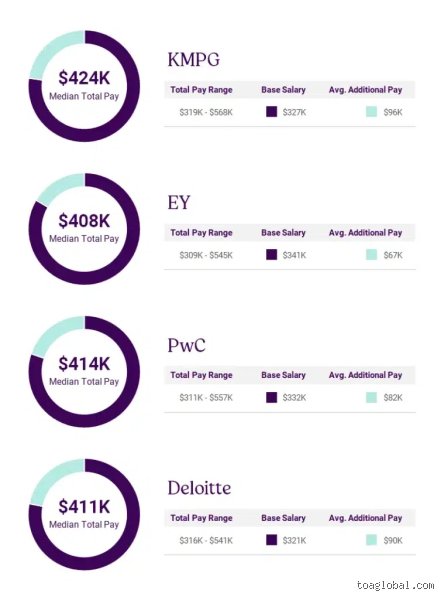

Deconstructing the Numbers: What Do the Big 4 Partners Take Home in 2026?

To really see where the money flows, we have to look at the massive differences across the specific service lines. In the United States and United Kingdom markets, corporate transparency laws and mortgage data have given us a remarkably clear picture of the current compensation ecosystem. The public numbers often show massive averages—like Deloitte UK reporting an average partner profit share of £1.01 million or KPMG UK hitting £880,000—but those blended figures are deeply misleading. I am telling you, the gap between the top and the bottom of the partnership pyramid is a canyon.

The Advisory and Strategy Arm Premium

If you want the real money, you stay far away from the traditional compliance divisions. The consulting and advisory arms—specifically elite strategy boutiques like PwC Strategy&, EY-Parthenon, and Monitor Deloitte—command the highest billable rates and the fattest profit margins. A partner in these specialized strategy units can easily pull down a starting total compensation of $700,000 to $1.5 million in their first few years, moving up toward the multi-million-dollar mark far faster than their peers. That changes everything when you are calculating lifetime earnings. Why? Because corporate clients are simply more willing to pay massive premiums for a high-stakes merger integration strategy than they are for a routine IT risk assessment.

The Commodity Grind of Audit and Assurance

Yet, the steady, predictable engine of the Big 4 remains the audit practice, even if it sits on the lower end of the compensation spectrum. According to a recent empirical study on U.S. partner compensation utilizing mortgage application data, the average audit partner brings home roughly $678,280. The bottom 25th percentile of audit partners pulls in about $344,000, which might shock ambitious senior managers who think the title guarantees instant wealth. The issue remains that audit services have become heavily commoditized; corporations view them as a regulatory tax, resulting in downward pressure on fees and, by extension, partner payouts.

The Hidden Levers: Performance, Seniority, and the Rainmaker Tax

Your paycheck is determined by three variables: your geographic market, your years in the saddle, and the size of your managed book of business. A partner who manages a massive, multi-million-dollar global account in New York City or London will out-earn a partner doing mid-market tax work in Salt Lake City every single day of the week. Honesty, it is unclear why more junior staff do not realize how regionalized these pools are. A look at the typical progression scale reveals the steep trajectory of the partnership life cycle:

The Standard Payout Progression Scale

The financial reality of the corporate lifecycle can be split neatly into distinct eras:

Years 1 to 5 (The Junior Tier): Average earnings sit around $450,000 to $600,000. Most of this cash is eaten alive by loan repayments for the initial equity buy-in, tax withholding, and pension funding.

Years 6 to 10 (The Mid-Tier Seniority): Compensation climbs to $1.25 million to $1.5 million as the partner inherits larger corporate accounts and expands their personal book of business.

Years 10+ (The Star Rainmakers): These individuals generate massive revenue streams, pulling in $1.5 million to $2.5 million by originating big-ticket advisory work.

The Management Circle (The Executive Elite): Global chairs, regional heads, and practice leaders who take home between $2.5 million and $5 million+, putting them on par with mid-sized investment bank managing directors.

The Alternative Paths: Big 4 Equity vs. Mid-Tier and Boutique Models

But what if you do not want to sacrifice your entire personal life to survive the grueling up-or-out culture of the industry giants? Many senior professionals are looking hard at mid-tier networks like BDO, RSM, or specialized boutiques. Conventional wisdom dictates that leaving the tier-one ecosystem means taking a massive financial hit, but the reality contradicts this idea beautifully. In fact, top-performing rainmakers can sometimes make more money at a mid-tier firm where they aren't forced to share their massive local profits with a bloated global corporate infrastructure.

The Economics of the Mid-Tier Alternative

At a non-Big 4 Top 100 firm, an average partner can comfortably expect to earn between $400,000 and $800,000 annually. Look at RSM UK, where average profits per partner recently jumped to £708,000—a figure that is breathing right down the neck of EY’s average UK partner pay. If you can build a highly profitable local client base, you might take home $1 million at a regional firm with a fraction of the administrative red tape and internal metrics that dominate the daily existence of a Deloitte or PwC partner. We're far from the days when the Big 4 held a monopoly on elite professional services wealth. The article continues in the next section, where we will break down the exact performance metrics used to fire underperforming partners.

Common Mistakes and Misconceptions About Partner Compensation

Most junior auditors stare at the equity pinnacle with distorted vision. They assume every partner raking in millions hoards it in a private vault, yet the reality of Big 4 partner earnings is far more cannibalistic. Your local tax partner does not just collect a fat salary check every two weeks. Let's be clear: they receive zero traditional salary because they are completely self-employed owners.

The Myth of the Flat Profit Split

People look at a firm's global multi-billion dollar revenue pool and imagine an egalitarian distribution matrix. That is a fantasy. The problem is that equity units are aggressively skewed based on seniority, client retention, and geographical performance. A newly minted assurance partner in a secondary market might take home $450,000, while a veteran deal advisory partner in New York pulls down $3.2 million. Performance metrics dictate everything, which explains why two partners sitting in adjacent offices often inhabit entirely different wealth brackets.

Ignoring the Capital Buy-In Tax

You do not just get handed your keys to the executive suite without opening your own wallet. New partners must buy their way into the partnership, a steep financial hurdle that frequently requires a capital contribution between $200,000 and $500,000. Many novices assume this is funded by the firm, except that it typically requires a massive personal bank loan. Your early distributions are heavily cannibalized to service this debt, meaning your net take-home pay during those initial years might feel shockingly pedestrian.

The Golden Handcuffs: Capital Retention and Corporate Exit Penalties

Behind the glittering facade of Big Four partner salaries lies a complex web of deferred compensation and strict capital retention policies designed to prevent talent poaching. When you generate millions in fees, the firm does not immediately distribute every dollar of your profit share. Instead, a massive chunk of your annual distribution is retained by the firm as working capital.

The Disappearing Wealth Paradox

What happens if you decide to jump ship to a competitor? You face a brutal financial reckoning. (Firms routinely hold onto your paid-in capital for up to two years after you exit, starved of any interest accumulation). If you breach a non-compete clause, some partnerships can legally strip away portions of your accumulated retirement credits. It is a brilliant, ruthless mechanism. As a result: the true liquidity of your wealth is severely throttled until you hit formal retirement age, creating a psychological trap that makes leaving almost unthinkable for mid-career equity holders.

Frequently Asked Questions

How much do Big 4 partners actually make at the entry level versus senior equity status?

Entry-level junior partners, often referred to as fixed-income or salaried partners, generally start with an annual compensation package ranging from $350,000 to $500,000 depending on their specific service line and market location. As they transition into full equity status over a period of three to five years, their income scales alongside their book of business. Senior equity partners who manage massive global accounts or lead entire regional divisions regularly see their Big 4 accounting firm partner pay climb well past $1.5 million to $3 million annually. The absolute ceiling for top-tier global board members and national managing partners can occasionally breach the $5 million threshold during exceptionally lucrative fiscal years.

What percentage of a partner's total compensation is tied directly to individual sales performance?

While standard base distributions exist to provide a baseline level of financial stability, roughly 40% to 60% of a partner's total year-end take-home pay is directly tied to quantitative metrics like managed revenue, utilization rates, and new business originations. The issue remains that failing to meet these strict origination targets directly deflates the value of your assigned equity units for the following fiscal cycle. Because individual performance is evaluated so aggressively, a bad year can result in a partner being asked to step down or face a severe reduction in their profit share percentage.

Do Big Four partners receive traditional corporate benefits and retirement pensions?

Because partners are classified legally as self-employed equity owners rather than standard employees, they must completely fund their own health insurance, disability coverage, and payroll taxes out of pocket. But the long-term payoff comes in the form of highly lucrative, unfunded partner retirement plans that functions separately from traditional corporate 401k structures. These bespoke pension systems frequently guarantee retired partners a fixed percentage of their highest average earnings for fifteen to twenty years post-retirement, provided the firm maintains its financial stability. Why would anyone endure the grueling eighty-hour work weeks for decades if this massive back-end safety net did not exist?

The Final Verdict on Partner Wealth

Reaching the top of the accounting pyramid is an undeniable financial triumph, but we must stop romanticizing the path as an easy ticket to effortless luxury. The immense payouts are a direct reflection of an unforgiving, high-stress lifestyle that consumes personal relationships and demands absolute corporate fealty. It is a high-stakes trade of your youth and sanity for a slice of an elite profit pool. We believe the financial rewards are spectacular, yet the toll exacted to secure those millions is far higher than most ambitious graduates realize. In short, you will get rich, but the firm will always extract its pound of flesh first.