The Legal Reality of Reaching the Magic Number 60

The financial world loves arbitrary milestones, but age 60 sits in a weirdly complicated sweet spot. In the United Kingdom, for example, the normal minimum pension age is currently 55, though this threshold is scheduled to climb to 57 on April 6, 2028. Because of this shifting timeline, hitting 60 means you have legally cleared the baseline hurdle for accessing private and workplace pensions. But people don't think about this enough: just because the gate is unlocked does not mean you should sprint through it. You are dealing with your own future survival, not a lottery win.

The Critical Difference Between Pot Types

We need to clear up some heavy confusion before moving forward. If you hold a defined contribution pension—which is basically a giant pot of money built by your own and your employer’s monthly inputs—you have immense freedom. You can take the lot. Yet, if you are fortunate enough to possess a defined benefit scheme, which is often called a final salary pension, the calculations shift dramatically. These gold-plated schemes are designed to pay out a guaranteed income based on your service years, and trying to cash them out at 60 usually triggers savage early retirement penalties. The trustees will recalculate your lifetime value using actuarial factors, and—poof—a massive chunk of your projected annual income evaporates because you dared to ask for it early.

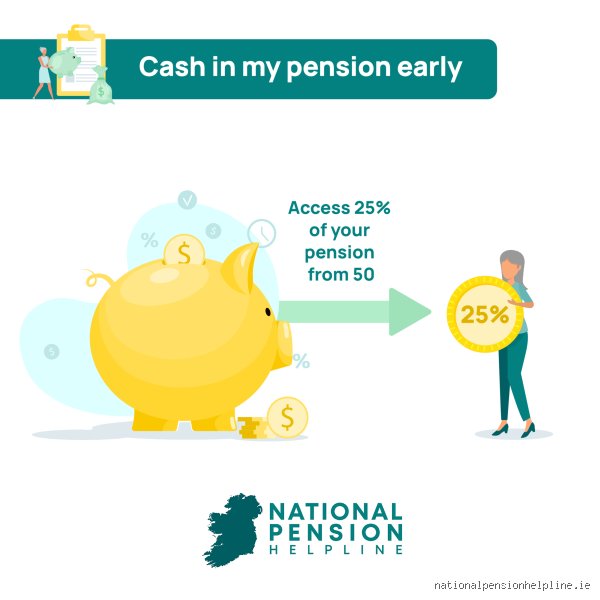

How the Taxman Gouges Your Lump Sum Withdrawals

Here is where it gets tricky, and frankly, where most savers lose their shirts. The headline rule sounds incredibly generous: you can take a 25% tax-free lump sum from your total pension pot. If you have managed to accumulate 400,000 pounds by the time you hit 60, you can legally pocket 100,000 pounds without giving a single penny to HMRC. That changes everything, right? Except that the remaining 75% of your pension pot is treated exactly like ordinary income.

The Emergency Tax Trap That Blindsides Savers

Imagine a scenario where a saver, let's call him David from Bristol, decides to cash out his remaining 300,000-pound balance all at once in a single tax year to buy a holiday home. David assumes he will just pay standard tax rates, but his pension provider is legally obligated to apply an emergency month-one tax code to that monstrous withdrawal. The system panics. It assumes David is going to make that exact same 300,000-pound withdrawal every single month of the year, pushing him instantly into the highest tax brackets. He ends up with a horribly depleted payout and has to spend months groveling to the government for a tax refund via a P55 form. It is a bureaucratic nightmare that could easily be avoided by dripping the money out over several fiscal years.

The Danger of Crossing Income Tax Thresholds

Do not forget that large lump sums stack directly on top of any other earnings you have in a calendar year. If you are still working a part-time consultancy gig at 60 and earning 25,000 pounds, pulling an extra 60,000 pounds from your pension instantly catapults you from the basic rate band straight into the 40% higher rate tax bracket. I strongly believe that paying unnecessary tax on money you spent thirty years saving is the ultimate financial sin. Why hand over nearly half of your hard-earned cash to the state just for the psychological satisfaction of seeing a massive balance in your current account? It makes zero mathematical sense.

The Hidden Costs of Lifetime Lifetime Trajectories

We must look at the cold, hard numbers regarding longevity. A healthy 60-year-old individual today has a very high probability of living well into their late 80s or 90s. If you completely cash out your pension at 60, you are demanding that this finite pool of money stretch across a 30-year retirement horizon. That is three full decades of inflation eroding your purchasing power like battery acid on metal.

The Nightmare of Inflation and Sequential Risk

Let us look at a historical comparison: a basket of goods that cost 100 pounds in 1994 costs more than double that amount today. If you liquidate your investments at age 60 and park that cash in a low-interest bank account because you want to "play it safe," you are guaranteed to lose money in real terms. Worse still is the threat of market sequence risk. If you keep the money invested but aggressively draw large chunks out during a stock market downturn—such as the 2008 financial crash or the 2020 pandemic dip—you lock in those losses permanently. Your pot will bleed out far faster than any spreadsheet predicted, and honestly, it is unclear how many savers actually understand this danger before pulling the trigger.

Comparing Cashing Out to Modern Alternatives

You do not have to swallow an all-or-nothing approach. The old-fashioned route of buying a lifetime annuity—where an insurance company guarantees you a fixed monthly check until you die—has lost its luster over the last two decades due to historically low interest rates, although recent rate hikes have given them a slight boost. But the real modern heavyweight alternative is flexible pension drawdown.

The Flexibility of Income Drawdown Over Total Liquidation

Instead of cashing out the entire sum, you leave your money invested in the market and selectively harvest small portions. You can take your 25% tax-free lump sum in stages—a process known as uncrystallised funds pension lump sums—or you can take the tax-free cash upfront and let the remainder ride the market waves. This keeps your money growing in a tax-sheltered environment while allowing you to control your annual income tax bracket. It requires discipline, which explains why many people avoid it, but as a result: you maintain control of your wealth rather than surrendering it to an insurance company or a massive tax bill.

Common mistakes and misconceptions

The illusion of a tax-free windfall

People see a massive pool of accumulated capital and instantly hallucinate absolute financial freedom. They believe the state merely shakes their hand and hands over the treasury. Except that it does not work that way at all. While the initial twenty-five percent slice escapes the clutches of the revenue collector, the remaining seventy-five percent undergoes standard income taxation. If you liquidate a massive pot within a single fiscal period, you inevitably push yourself into the highest possible tax bracket. You effectively hand back a staggering chunk of your hard-earned wealth to the government. Let's be clear: treating your retirement pot like a standard bank account is an astronomical blunder.

The lifetime allowance echo chamber

Many individuals remain entirely oblivious to the lingering ghosts of abolished thresholds. They assume recent legislative restructuring means total immunity from historical penalties. The problem is that transition certificates still dictate the precise mechanics of your final payout. If you fail to secure the correct protection documentation before triggering your access, you face irreversible financial friction.

Underestimating the longevity calculation

How long do you honestly expect to survive? It is an uncomfortable inquiry, yet ignoring reality is a recipe for eventual destitution. Pulling everything out early means you must stretch those remaining pennies across potentially three additional decades. Medical advancements continuously push life expectancies higher, which explains why a lump sum that looks massive today dissolves into nothingness by the time you hit eighty-five.

The hidden recycling trap and expert strategy

The stealthy mechanism of pension recycling

The temptation to extract tax-free cash only to immediately reinvest it back into another qualifying vehicle to trigger secondary relief is immense. It sounds like an infallible wealth loop. Yet, the regulatory authorities anticipated this exact maneuver and instituted severe anti-recycling rules. If your contributions spike significantly above your typical historical baseline around the time you draw benefits, your entire arrangement faces aggressive investigation.

The strategy of staggered drawdowns

Instead of a total clearance, smart operators utilize a phased extraction methodology. You pull precise, smaller amounts annually to remain strictly underneath the higher-rate threshold. This ensures your remaining funds continue to experience compounding market growth inside a tax-sheltered ecosystem. Why liquidate an asset that is actively shielding you from capital gains liabilities? It makes zero financial sense.

Frequently Asked Questions

Can I cash out my pension at 60 and continue working?

Yes, you possess the legal right to execute this maneuver, but the long-term fiscal consequences require careful navigation. Once you flexibly access your taxable pot, your annual tax-relieved savings capacity shrinks dramatically via the Money Purchase Annual Allowance, which drops your threshold from sixty thousand pounds to a restrictive ten thousand pounds per annum. This means if you remain employed, your ability to rebuild that nest egg becomes severely choked. Data from recent industry audits indicates that

over forty-two percent of individuals who utilize this dual approach accidentally trigger tax penalties because they fail to monitor this lowered limit.

Will cashing out early impact my State Pension eligibility?

Your private or workplace holdings operate on an entirely separate track from the state-provided safety net. Emptying your personal accounts at sixty will not alter your eventual state entitlement, but you cannot actually touch that statutory state benefit until you reach age sixty-seven or sixty-eight, depending on your exact birth year. Statistics reveal that the maximum full state benefit sits at just under eleven thousand five hundred pounds annually, a sum that rarely covers basic modern living costs on its own. As a result: relying solely on that future state guarantee while completely draining your private reserves early creates a dangerous income void for those middle years.

What happens to my remaining funds if I die after cashing out partially?

Any wealth left untouched within your qualifying retirement wrapper can be passed down to your chosen beneficiaries with incredible tax efficiency. If your demise occurs prior to the age of seventy-five, your heirs generally inherit the remaining balance completely free of income tax. However, if you have already transferred that wealth into a standard checking account or property, it immediately falls into your estate and faces a potential

forty percent inheritance tax blow. Financial sector reports show that families lose millions of pounds collectively each year simply because individuals unnecessarily move assets out of protective wrappers too early.

A decisive verdict on early liquidation

The freedom to dismantle your entire retirement framework at age sixty is an undeniable legal reality, but treating this option as a green light for total liquidation is an act of fiscal self-sabotage. We live in an era where inflation aggressively erodes purchasing power, meaning cash sitting in conventional accounts loses real value daily. Maintaining your capital within an environment that actively blocks tax liability is the only logical choice for sustained financial survival. My definitive position is that total cash-outs are a luxury for the uniform, while structured, cautious utilization is the path of the true professional. (Admittedly, exceptional circumstances like terminal illness dismantle this logic entirely). Do not sacrifice thirty years of future stability for a fleeting moment of liquidity today.