The messy truth about measuring global sovereign liabilities

The thing is, shouting about massive numbers on a digital debt clock makes for great political theater but terrible economic analysis. If a billionaire carries a million-dollar mortgage, nobody blinks because their earning power handles it effortlessly. But give that same mortgage to a barista, and you have a catastrophic foreclosure in the making. That changes everything when we try to pin down who wears the crown of fiscal insolvency.

The divergence between raw cash and relative leverage

Economists generally split into two camps when analyzing this chaos. One camp obsesses over the total nominal pile, pointing nervously at the American treasury market. The other camp focuses on sustainability, calculating what a country owes relative to its gross domestic product. People don't think about this enough, but a country can technically be trillions of dollars deep in red ink and still be considered safer by global investors than a small nation owing just a few billion. Why? Because the larger economy possesses the institutional machinery, tax base, and systemic trust needed to keep refinancing its obligations indefinitely without triggering a panicked run on its currency.

Why simple ledger balances lie to investors

Honestly, it's unclear why public debate remains so primitive when analyzing national balance sheets. Looking strictly at public sector liabilities ignores the massive assets a government might hold, not to mention the crucial cushion of domestic private wealth. Where it gets tricky is when you realize that some of the highest gross debt figures belong to nations with immense industrial capacity and incredibly deep local capital markets. To evaluate financial peril accurately, one must look past the terrifying front-page headlines and dissect exactly who holds the receipts, what currency those receipts are denominated in, and whether the central bank can simply print its way out of a tight corner.

The raw titan: Inside the American multi-trillion dollar cash machine

Let us look at the undisputed heavyweight of nominal borrowing. The absolute mountain of obligations issued by Washington makes every other nation look like small-time spenders. But does this colossal ledger actually mean the world's largest economy is on the brink of collapse? We are far from it.

Deconstructing the thirty-four trillion dollar mountain

By early 2026, the gross federal debt of the United States hovered at an astronomical scale, cementing its status as the largest nominal borrower in human history. To put this in perspective, that single pile of debt is larger than the entire economic output of China, Germany, Japan, and India combined. But the issue remains: the global financial architecture is built entirely on the assumption that American Treasury bonds are the safest assets on earth. And because the global trade network relies heavily on the greenback, the American government enjoys the unique privilege of borrowing vast sums in its own currency. If a crisis hits, the Federal Reserve can theoretically purchase sovereign bonds through open-market operations—a luxury that developing nations simply do not possess.

The real danger of escalating debt servicing costs

Yet, the structural dynamics of the American bond market are shifting in a way that should make policymakers deeply uncomfortable. As the Federal Reserve maintained elevated benchmark interest rates through recent years to combat persistent inflation, the cost of servicing that thirty-four trillion dollar mountain skyrocketed. The math is brutal: net interest payments are rapidly consuming a larger share of the federal budget than the entire national defense allocation. What happens when a country spends more on paying back yesterday's party than investing in tomorrow's infrastructure? As a result: the fiscal space for reacting to unexpected geopolitical shocks or sudden domestic recessions shrinks dramatically, creating a slow-burning vulnerability that no amount of political bravado can fully obscure.

Domestic political gridlock versus systemic market trust

The real risk to Washington isn't a sudden lack of cash, but rather the weaponization of the debt ceiling by ideological factions in Congress. Every few months, the spectacle of potential default plays out on global television screens, threatening to disrupt the plumbing of the global financial system. Except that markets have grown cynical, treating these theatrical standoffs as empty posturing rather than genuine credit events. I believe this complacency is dangerous because public trust is a non-linear resource—it holds firm right up until the moment it utterly evaporates. If international investors, who currently hold trillions in American debt, decide that the political dysfunction has crossed a line, the subsequent capital flight would trigger an unprecedented global monetary earthquake.

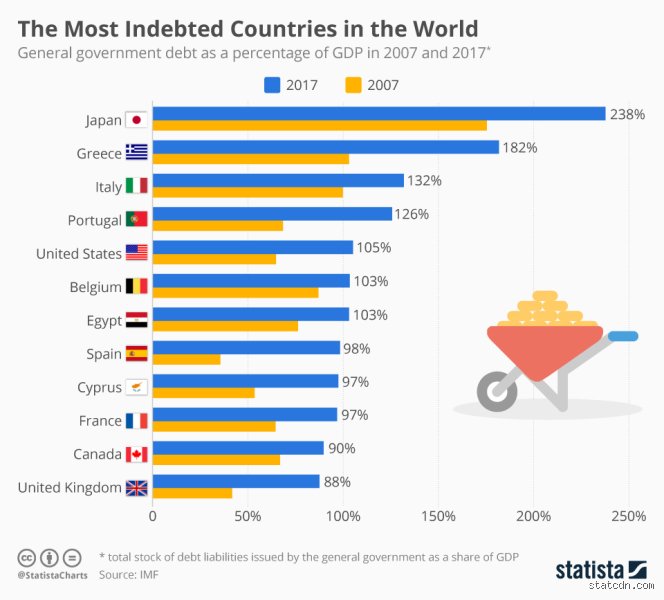

The relative giant: Japan’s paradoxical economic fortress

Shift your gaze across the Pacific, and you encounter an entirely different species of fiscal anomaly. Japan defies conventional macroeconomic wisdom by maintaining a debt-to-GDP ratio that has hovered north of 200% for over a decade, currently sitting at roughly 230% of GDP according to recent International Monetary Fund data.

How Tokyo sustains an impossible debt-to-GDP ratio

Under traditional economic theory, any nation that crosses the 100% threshold is supposed to face surging bond yields and impending ruin. Yet, Tokyo’s 10-year government bond yields remained pinned near zero for years, only creeping up slightly as the Bank of Japan tentatively adjusted its yield curve control policies. How does this bizarre alchemy work? The secret lies in the ownership structure of the debt. Unlike vulnerable emerging markets that rely on fickle foreign speculators, the vast majority of Japanese government bonds are held domestically by local banks, massive pension funds, and the central bank itself. It is essentially an internal family arrangement; the Japanese people are lending money to their own government in their own currency, rendering a sudden speculative attack almost impossible to execute.

The demographic trap crushing public finances

But here is where the story takes a dark turn into structural stagnation. Japan’s real crisis isn't the size of its ledger, but the rapid aging of its population. With a shrinking workforce and a ballooning retirement demographic, the tax base is contracting precisely when healthcare and social security expenditures are skyrocketing. The government cannot easily grow its way out of this trap because economic growth requires either more workers or surging productivity, and Tokyo is currently struggling on both fronts. The Bank of Japan has effectively monetized the state’s fiscal deficit, buying up massive quantities of government bonds to keep the system lubricated, which explains why the yen has faced intense downward pressure against the dollar in recent global trading cycles.

Sovereign leverage models: Structural stability versus imminent default

To truly understand which country is most in debt, you have to look at the massive gulf between advanced economies and developing nations. The stark contrast between how different states handle high leverage reveals the inherent unfairness of the global financial hierarchy.

The shield of reserve currency status

Advanced economies like the G7 nations operate with a profound structural advantage: they borrow in currencies they control. When the United Kingdom, France, or Canada run fiscal deficits, they issue debt denominated in pounds, euros, or Canadian dollars. If investor demand cools, their respective central banks can step in as buyers of last resort. This institutional backstop acts as a financial shock absorber, allowing these nations to sustain high leverage ratios that would instantly bankrupt a less developed economy. It is an elite club where the rules of gravity seem temporarily suspended, though critics argue this endless liquidity creation is simply kicking a massive inflation can down the road.

The brutal reality for emerging market borrowers

Now look at the opposite end of the spectrum, where nations like Sudan, Venezuela, or Lebanon reside. These countries often see their debt-to-GDP ratios explode not because of strategic domestic investment, but due to hyperinflation, political collapse, and currency devaluation. Because international lenders rarely trust local fiat currencies, these vulnerable governments are forced to borrow in foreign denominations like the U.S. dollar or the euro. When their local currency crashes, the real value of their foreign-denominated debt multiplies overnight, making repayment an absolute mathematical impossibility. This is where high debt ceases to be an abstract policy debate and becomes a tangible humanitarian catastrophe, leading directly to medicine shortages, rolling blackouts, and societal paralysis.

Common mistakes in evaluating which country is most in debt

Confusing nominal debt with economic capacity

Big numbers scare people. When observers look at the global financial landscape, they often point to the United States because its gross national debt has sailed past 34 trillion dollars. That sounds catastrophic. The problem is, looking at absolute numbers completely distorts reality. You cannot judge a household's financial health by its mortgage size without looking at its salary. The same applies to nations. A massive economy can carry a massive mountain of obligations without breaking a sweat, which explains why smart analysts prefer using the debt-to-GDP ratio instead of nominal figures.

Ignoring the hidden cushion of internal liabilities

Who actually owns the risk? Tokyo owes an eye-watering 260% of its annual economic output, a metric that should signal immediate bankruptcy. Except that domestic investors hold over 85% of this burden. The Japanese government essentially owes money to its own citizens in their own currency. Because of this, the risk of a sudden, chaotic default is drastically lower than it would be for an emerging economy borrowing in foreign denominations. When evaluating which country is most in debt, failing to distinguish between domestic and external obligations is a fatal analytical error.

The trap of omitting private sector vulnerabilities

Public balance sheets only tell half the story. If a state boasts a pristine, low-deficit budget but its citizens and corporations are drowning in leverage, the entire system remains fragile. Look at China, where official central government liabilities appear perfectly manageable. However, local government financing vehicles and a bloated real estate sector conceal a different reality altogether. In short, focusing exclusively on sovereign bonds leaves you blind to systemic economic collapses.

The liquidity mirage and expert risk assessment

Why printing money is not a permanent escape hatch

Can a nation simply print its way out of a fiscal crisis? Central banks can manipulate interest rates and purchase government bonds to keep yields artificially low, acting as a temporary shield. But let's be clear: this mechanism merely shifts the pain from the bond market to the grocery store. Reckless monetary expansion triggers aggressive inflation, eroding the purchasing power of the populace and destroying international confidence. Do you really think global investors will keep buying treasuries if they are repaid in depreciated currency?

Evaluating structural resilience over raw percentages

True economic vulnerability depends on institutional strength and market trust rather than arbitrary mathematical thresholds. A nation with robust democratic institutions, transparent legal frameworks, and deep capital markets can sustain leverage that would instantly crush a fragile state. Which country is most in debt from a risk perspective is rarely the one with the highest nominal ledger. It is the nation that loses the confidence of its creditors, causing interest payments to consume the national budget. (We have seen this tragic movie play out multiple times in Latin America and Sub-Saharan Africa.)

Frequently Asked Questions

Does a high debt-to-GDP ratio always trigger an economic collapse?

Absolutely not, as history consistently demonstrates that institutional credibility matters far more than raw mathematical ratios. Japan has maintained a ratio exceeding 200% for over a decade without experiencing hyperinflation or a sovereign bond default. Conversely, Greece triggered a massive European crisis in 2010 when its liabilities hovered around 130% of economic output, proving that market confidence is highly variable. Creditors tolerate high leverage from nations with stable political systems and reliable tax collection mechanisms. As a result: advanced economies can safely navigate fiscal waters that would immediately capsize developing nations lacking deep domestic capital pools.

Which country is most in debt to foreign creditors?

The United States holds the title for the largest absolute volume of external obligations, with foreign investors owning over 8 trillion dollars of its sovereign liabilities. Japan and China remain the two largest individual holders of this American treasury supply, though their portfolios have fluctuated in recent years due to geopolitical shifts. Yet, when evaluated as a percentage of economic output, smaller nations like Greece and Portugal often show much higher concentrations of external liabilities. This distinction matters because relying heavily on foreign capital leaves a state vulnerable to global market sentiment shifts. Consequently, the international community watches American fiscal policy closely, knowing that any disruption there would instantly destabilize global financial networks.

How do global organizations calculate which country is most in debt?

Organizations like the International Monetary Fund and the World Bank track sovereign liabilities by standardizing data into gross and net metrics across different global regions. Gross metrics capture the total outstanding obligations issued by a government, while net figures subtract the financial assets that the state currently owns. This dual methodology ensures that resource-rich nations with vast sovereign wealth funds are not unfairly categorized alongside impoverished states. Analysts also meticulously separate central government liabilities from those incurred by local municipalities or state-owned enterprises. By using these standardized baselines, economists can accurately determine which nation faces the highest debt risk without being deceived by inconsistent accounting practices across different continents.

A definitive verdict on sovereign leverage

We need to discard the simplistic notion that high sovereign liabilities are an automatic death sentence for a modern nation. The obsession with declaring the most indebted country in the world based on arbitrary percentages misses the deeper geopolitical reality of financial power. True fiscal danger arrives not when a ledger crosses a specific number, but when a state loses its structural capacity to innovate and produce tangible economic value. The United States and Japan will continue to borrow heavily because the global financial architecture demands their liquidity, meaning their leverage is a feature of the system rather than a bug. But let's be clear: this structural privilege is not infinite, and treating a printing press as a replacement for real economic productivity is a dangerous game. Wealthy democracies will likely test the absolute limits of their fiscal elasticity until a major systemic shock forces an incredibly painful paradigm shift upon global markets.