The Historical Fault Lines: Where These Financial Empires Came From

We did not just wake up one day with two monolithic systems ruling the capital markets. The Financial Accounting Standards Board, known to insiders as FASB, has been chiseling away at US GAAP since 1973 in Norwalk, Connecticut. They built a fortress of rules. Why? Because American litigators love a loophole, and detailed bright-line percentages give companies a legal shield. But while Washington was perfecting its rulebook, Europe looked at the globalizing world of the late 1990s and realized something had to give. The London-based International Accounting Standards Board unleashed the International Financial Reporting Standards in 2001 to harmonize things, yet here we are a quarter-century later, still straddling a massive structural chasm.

The Battle of Philosophy: Rules Versus Principles

Where it gets tricky is how these two entities view human nature. GAAP assumes that without explicit instructions, corporate CFOs will manipulate the numbers, which explains why the American codification spans thousands of incredibly dense pages. It dictates exactly what to do. IFRS, conversely, trusts executives to capture the true economic substance of a transaction, providing a leaner, conceptual framework. I happen to think this trust is occasionally naive. Some experts disagree, arguing that rigid rules actually invite Wall Street investment bankers to engineer complex financial instruments specifically designed to bypass the letter of the law while violating its spirit. Which approach is truly safer? Honestly, it's unclear.

The Failed Marriage of the Norwalk Agreement

People don't think about this enough, but there was a moment in October 2002 when we almost had a unified global system. The Norwalk Agreement promised convergence, a beautiful dream where FASB and IASB would merge their ideas into a singular financial reality. For a decade, joint task forces met, compromises were hammered out, and then the momentum simply evaporated. The SEC grew fiercely protective of American capital markets, realizing that giving up control over GAAP meant ceding power to an international body. That changes everything because it proved that accounting isn't just math—it is an exercise in geopolitical sovereignty.

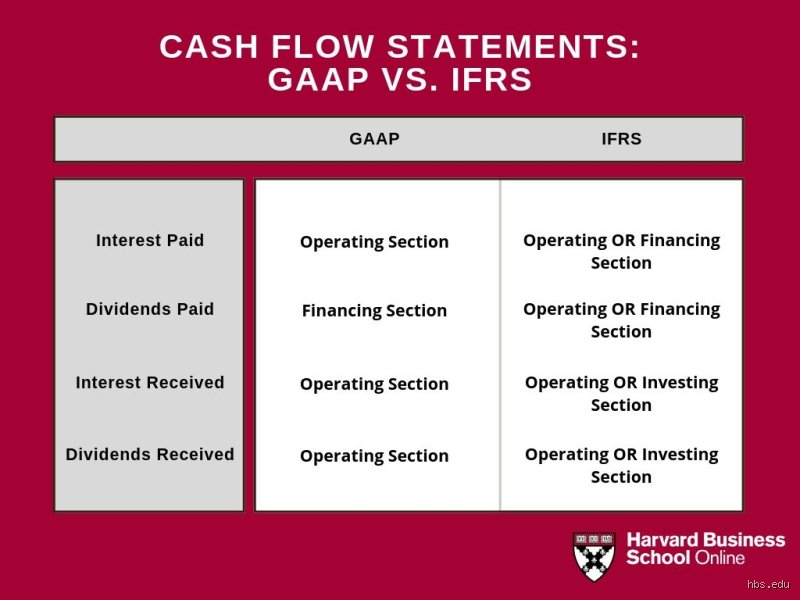

The Inventory Battleground: LIFO, FIFO, and the Ghost of Inflation

Let us look at inventory valuation, a seemingly mundane corner of the balance sheet where the difference between IFRS and GAAP turns into a multi-million-dollar knife fight. The American system permits a method called Last-In, First-Out. This allows companies to assume that the last items placed in the warehouse are the first ones sold. During periods of aggressive inflation, this is an incredible tax shield because it artificially inflates the cost of goods sold, which subsequently depresses reported net income. But across the border, IFRS bans this practice outright. It is completely illegal under international standards.

The Real-World Chaos of the LIFO Prohibition

Imagine a heavy equipment manufacturer based in Peoria, Illinois, using GAAP, competing directly with a rival in Munich operating under international rules. During the supply chain crunches of recent years, the American firm utilized LIFO accounting to write off expensive steel costs immediately, lowering their taxable income significantly. The German company was forced to use First-In, First-Out, meaning their balance sheet reflected older, cheaper steel, resulting in a massive, glittering profit on paper that triggered a hefty tax bill. That is not a minor technicality. We are talking about millions of dollars in actual cash flowing out of a business simply because of geographic jurisdiction.

Reversing Inventory Write-Downs: A Tale of Two Balances

But the variance does not end at the checkout counter. Suppose market conditions deteriorate and that same Peoria firm writes down the value of its raw inventory by $5 million because commodity prices crashed. Next year, the market miraculously recovers. Under US GAAP, that write-down is locked in stone; you cannot undo it, meaning the asset's carrying value is permanently impaired. IFRS takes a completely different path, permitting a full reversal of the write-down if the economic recovery is verifiable. It creates a far more volatile earnings report, yet it arguably reflects the current market reality with superior accuracy.

Capitalizing Secrets: How R&D Costs Mutate Across Borders

Software development and pharmaceutical research highlight the deepest philosophical difference between IFRS and GAAP. Under the watchful eye of the SEC, American companies must treat virtually all research and development expenditures as immediate expenses. The money leaves the building, hits the income statement, and instantly reduces that quarter's profitability. It is a conservative, cynical view that assumes most corporate research yields absolutely nothing of value.

The International Divide on Intangible Assets

International standards split this process down the middle, distinguishing between pure research and actual development. Once a tech project hits what accountants call technological feasibility—meaning it is viable and the company intends to complete it—the cash spent on development transforms into an intangible asset on the balance sheet. Instead of a massive loss on the income statement, you get an asset that bolsters equity. Is this a fair representation of innovation, or is it just a clever way for tech firms to hide their burn rate? The issue remains that two identical startups, one in Silicon Valley and one in Berlin, will look completely different to an untrained venture capitalist.

The Impact on Tech Giants and Biotech Valuation

Consider a biotechnology firm spending $50 million annually to develop a new cardiovascular drug. A GAAP-compliant statement might show consecutive years of deep losses, potentially scaring away risk-averse retail investors who look solely at net earnings. Meanwhile, an IFRS competitor capitalizing those exact same development costs would show a robust balance sheet packed with valuable intangible assets, presenting a picture of steady, healthy growth. Hence, the American approach protects investors from vaporware, but except that it simultaneously penalizes companies engaged in genuine, long-term innovation.

The Property, Plant, and Equipment Paradox

Fixed assets like factories, land, and heavy machinery are treated like ancient artifacts under US GAAP. Once you buy a piece of real estate, it is recorded at its historical cost, depreciated over time, and that is the end of the story. Even if that office tower in midtown Manhattan appreciates by 300% over two decades, its value on the balance sheet stays stubbornly low. The American system values verifiability over relevance, refusing to trust appraisals that could be subjective or manipulated by over-optimistic corporate boards.

The Revaluation Model: A Volatile Luxury

International firms view their property through a radically different lens. IFRS gives corporations a choice: they can use the historical cost model, or they can opt for the revaluation model. This allows businesses to regularly adjust the carrying value of their property, plant, and equipment to reflect current fair market value. As a result: an international hotel chain can revalue its global resort portfolio upward during a real estate boom, instantly inflating its total equity and lowering its debt-to-equity ratio, making it look far more attractive to commercial lenders.

The Catch-22 of Constant Appraisals

But this accounting freedom comes with a brutal catch that many corporate executives fail to anticipate. If you choose the revaluation model under international rules, you cannot just revalue your assets when times are good and ignore them when the market tanks. You are locked into a cycle of continuous, expensive appraisals. If property values plummet, you must take an immediate hit to your revaluation surplus, or worse, a direct charge against earnings. It introduces a level of balance sheet turbulence that would give most conservative American corporate treasurers a heart attack, proving that flexibility is a double-edged sword.

Common mistakes and misconceptions about accounting frameworks

The myth of absolute convergence

Many practitioners labor under the delusion that the London-based board and its Norwalk counterpart have successfully fused their rulebooks over the last two decades. They have not. While joint projects did harmonize revenue recognition rules, major divergence persists elsewhere. What is the difference between IFRS and GAAP if you look at basic inventory valuation? US GAAP permits Last-In, First-Out (LIFO) calculations, a method that saves American corporations billions in taxes during inflationary cycles. Conversely, international rules ban LIFO outright. Believing these two systems are twins is an expensive blunder.

Rules versus principles is an oversimplification

You have likely heard professors chant that international standards rely on broad principles while American rules dictate rigid formulas. Let's be clear: this binary view is mostly a historical relic. The American codification spans over ninety thousand pages, which admittedly dwarfs the international counterpart. Yet, international rules contain incredibly dense application guidance for complex financial instruments. The issue remains that both frameworks demand rigorous professional judgment. CPAs cannot simply tick boxes, nor can international auditors just follow their gut feelings.

Assuming identical financial statement presentation

A balance sheet is a balance sheet, right? Wrong. Under international conventions, companies routinely list assets in reverse order of liquidity, placing non-current items like property and equipment at the very top. American templates do the exact opposite by starting with cash. Furthermore, the definition of operating income changes depending on geographic jurisdiction. This variance distorts quick visual comparisons, which explains why cross-border investors often misinterpret initial corporate performance metrics.

The hidden volatility of fair value revaluation

The asset upward adjustment trap

Experienced CFOs understand a hidden mechanism in international financial reporting standards that remains strictly forbidden under American oversight. We are talking about the revaluation model for long-lived assets. Under international protocols, an enterprise can adjust the carrying value of its real estate upward to reflect current market realities. (American corporations must stick to historical cost minus depreciation, barring impairment). This means an international balance sheet fluctuates with property market swings. It creates an illusion of wealth during booms, followed by brutal impairment hits during crashes. As a result: your financial statements become a rollercoaster. We believe this introduces unnecessary noise into corporate valuations, making steady long-term forecasting a nightmare for conservative analysts.

Frequently Asked Questions

Can a company switch between accounting frameworks arbitrarily?

No, regulatory bodies strictly police these transitions because arbitrary changes would destroy year-over-year financial comparability. For instance, the US Securities and Exchange Commission requires domestic public entities to use American standards, meaning over 4,000 listed US corporations have zero choice in the matter. Foreign private issuers in New York may use international standards, but they cannot flip-flop between systems annually. If a private entity decides to transition, the implementation process usually requires three years of retrospective financial restatements. This administrative overhaul typically consumes hundreds of thousands of dollars in auditing fees.

How do inventory write-downs differ between the two systems?

The operational divergence here centers on whether a company can reverse a previous write-down when market conditions improve. Under international rules, if the net realizable value of inventory recovers, you can write the asset back up to its original cost basis. But American rules treat a write-down as a permanent reduction of the cost basis. Except that the inventory might actually regain its value, the American system forbids any recovery recognition until the item is sold. This creates a permanent discrepancy in gross profit margins between identical businesses operating under different jurisdictions.

Which framework do international investors generally prefer?

Global capital markets overwhelmingly favor international financial reporting standards due to their widespread geographic footprint across more than 140 jurisdictions worldwide. European, Australian, and Canadian markets demand this compliance, which streamlines cross-border capital allocation. However, Wall Street analysts frequently prefer domestic rules because the prescriptive criteria offer fewer loopholes for aggressive corporate managers. The difference between IFRS and GAAP becomes highly visible here, as international rules grant executives more leeway in structuring transactions to achieve desired accounting outcomes.

The ultimate verdict on corporate transparency

The ongoing dual-system reality represents an artificial tax on global capital efficiency. We are convinced that maintaining two distinct financial languages serves nobody but highly paid accounting consultants and specialized software vendors. The American stubbornness to retain its domestic codification smells of regulatory protectionism. But international standard-setters are not blameless either, given their tendency to introduce volatile fair-value adjustments that distort economic reality. In short, the divergence forces analysts to spend half their time translating numbers rather than judging actual business viability. True global financial integration will remain a fantasy until one framework blinks and surrenders its sovereignty entirely.