The Anatomy of a Financial Mirage: Defining Maximum Potential Exposure in Volatile Markets

Let us stop pretending that modern market risk is a gentle, predictable bell curve. Wall Street loves comfort, yet comfort is exactly what gets institutions wiped out during black swan events. When we talk about maximum potential exposure, or MPE, we are isolating the absolute zenith of credit risk over the entire lifespan of a transaction. It is not a static figure.

The Diffusion Curve Paradox

Think of MPE as an expanding cone of uncertainty. Early on, you know where you stand, but as time marches forward, the potential paths a portfolio can take multiply exponentially. This is the diffusion effect. Yet, because derivative contracts eventually mature and cash flows settle, the risk tapers off near the end of the timeline. The result? A hump-shaped risk profile that peaks long before the final bell rings. It is precisely at that peak where institutions find themselves dangerously under-collateralized if they miscalculate.

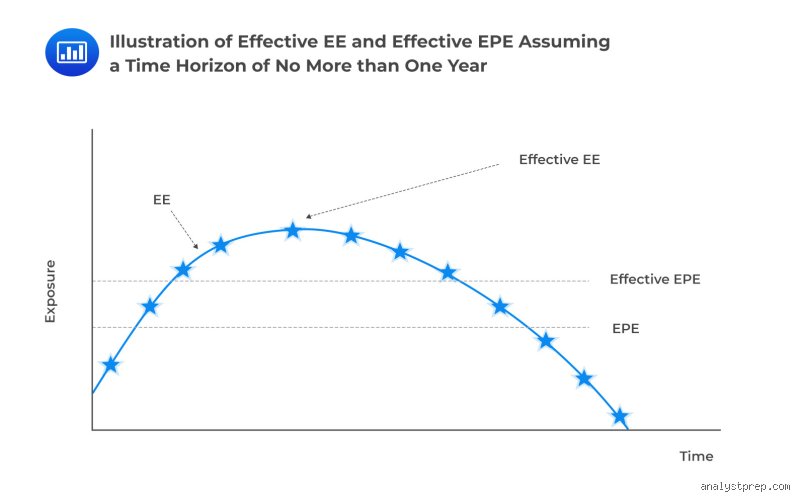

Why Peak Exposure Displaces Average Expectations

Most novice analysts confuse MPE with Expected Positive Exposure (EPE). That changes everything, and frankly, it is a rookie mistake. EPE takes the average of all possible positive outcomes, offering a soothing, smoothed-out metric for capital allocation. MPE does the exact opposite. It ignores the comforting averages to focus exclusively on the terrifying 95th or 99th percentile of potential loss vectors. It asks a brutal question: if the counterparty defaults at the exact moment the market moves violently against us, how much cash vanishes?

Quantifying the Catastrophe: The Mathematical Mechanics of MPE

Calculating this metric is a computational nightmare that devours server capacity. You cannot just look up a historical price and call it a day because the future refuses to mimic the past. Instead, risk engines must simulate thousands of parallel universes.

Monte Carlo Simulations and the 99th Percentile Myth

To pinpoint the maximum potential exposure, quantitative analysts deploy massive Monte Carlo frameworks. These algorithms generate 10000 or more forward price paths for underlying assets—be it interest rates, foreign exchange pairs, or sovereign debt. The system calculates the replacement cost of the portfolio at every single future node. If we examine a standard 10-year interest rate swap, the model might flag year 3 as the danger zone. Why? Because that is where the volatility of the underlying swap rate intersects catastrophically with the remaining tenor of the contract. Honestly, it is unclear why some firms still rely on historical simulation when regime shifts render old data utterly useless.

The Problem with Static Volatility Assumptions

Here is where it gets tricky. Traditional models assume that market volatility behaves itself, remaining constant through the life of a trade. We saw how spectacularly that assumption failed during the 2008 Lehman Brothers collapse, and again during the commodity market dislocations of March 2022. When volatility spikes, the tail of the distribution fat-tens. Your 99th percentile boundary suddenly shifts outward by a factor of three, transforming a manageable credit risk into a balance-sheet-destroying monster.

The Collateral Illusion: Mitigation vs. Real-World Liquidation

Every risk manager points to Credit Support Annexes (CSAs) and daily margin calls as their ultimate shield. They believe bilateral collateralization eliminates credit risk entirely, but we are far from it.

The Margin Period of Risk Trap

Suppose your counterparty, a hedge fund based in Greenwich, Connecticut, fails to meet a margin call on a Tuesday morning. You do not get to seize and liquidate their assets instantly. The legal grace periods, operational friction, and sheer market panic create a lag. This window is known as the Margin Period of Risk (MPOR), typically modeled at 10 to 20 business days. During this agonizing fortnight, the market keeps moving. If you calculated your maximum potential exposure assuming instantaneous liquidation, you are now exposed to uncollateralized market drift during a period of peak panic. The issue remains that closing out thousands of complex exotic options in a illiquid market forces you to accept horrific fire-sale prices.

Rehypothecation and Chain-Reaction Defaults

People don't think about this enough: collateral isn't just sitting in a vault. It gets reused. Through rehypothecation, the high-quality liquid assets pledged to you might have been pledged elsewhere three times over. When a default cascade triggers, the legal gridlock over who owns what security can freeze liquidations for months. As a result: your calculated MPE must incorporate a haircut that accounts for systemic operational paralysis, not just pure asset volatility.

MPE Versus Potential Future Exposure: A Critical Dichotomy

In regulatory capital discussions, terms get thrown around loosely, leading to dangerous conflation. The most frequent mix-up occurs between MPE and Potential Future Exposure (PFE).

The Temporal Distinction

While both metrics look at upper-tail percentiles, they view time through entirely different lenses. PFE looks at a specific snapshot in time—say, one year from today. It answers what the risk looks like at that exact milestone. Conversely, maximum potential exposure scans the entire horizon line, hunting for the absolute highest peak across all simulated dates. Yet, regulators often allow banks to use PFE profiles to determine capital requirements under Basel III rules, which can inadvertently mask the true peak vulnerability if the reporting dates do not align with the maximum hump of the diffusion curve.

The distinction matters because managing a portfolio based on PFE snapshots is like checking the weather at 9:00 AM and 5:00 PM while completely ignoring the category 5 hurricane that hits at noon. Hence, sophisticated trading desks utilize MPE as their hard limit for credit lines, ensuring that even if a counterparty defaults at the worst possible micro-second of a fifteen-year structural trade, the survival of the clearing bank is never in jeopardy.

Common mistakes and dangerous misconceptions

Confusing potential loss with immediate reality

Many risk managers fall into a psychological trap where they conflate the worst-case scenario with an imminent operational certainty. Let's be clear: calculating your maximum potential exposure does not mean you are going to lose that exact mountain of capital tomorrow morning. It represents a theoretical ceiling. The problem is that when boards see a staggering figure like 42 million dollars attached to a single counterparty derivative portfolio, panic sets in immediately. They freeze credit lines unnecessarily. Yet, halting business based purely on an extreme statistical outlier is a terrible way to run an enterprise. You must separate the absolute outer boundary of risk from daily operational volatility.

The dangerous illusion of static metrics

Markets breathe. Volatility spikes during geopolitical crises, which explains why a calculation done on a quiet Tuesday becomes completely obsolete by Friday afternoon. Assuming your maximum potential exposure is a fixed, unchangeable monument is perhaps the most expensive mistake a firm can make. If your risk assessment models use historical data that ignores the 2008 crash or the 2020 pandemic anomalies, your ceiling is built of glass. Think of it as a moving target that requires continuous algorithmic recalibration, rather than a quarterly compliance box you can just check and forget about.

Overestimating the safety net of basic collateral

Because you hold collateral, you think you are safe? That is a comforting fiction. If a major counterparty defaults, the liquidation value of those high-yield bonds you accepted as security will likely plummet by 35% or more within hours. The issue remains that standard netting agreements often fail to account for these systemic correlation cascades. You might find that your true financial vulnerability far exceeds the net figures on your ledger, leaving you exposed to the very abyss you thought you had securely mapped out.

Unlocking the extreme tail: Expert liquidity correlation advice

The hidden trap of wrong-way risk

Standard quantitative models often treat market risk and credit risk as separate silos, but they are secretly married. True mastery of managing maximum potential exposure requires you to hunt for specific, toxic correlations known as wrong-way risk. This occurs when your exposure to a specific counterparty surges at the exact moment their probability of default skyrockets. For instance, if you write credit default swaps for an investment bank using that same bank's underlying debt securities as your primary risk benchmark, you have engineered a financial doomsday machine.

To survive, you must inject severe liquidity stress testing into your framework. We recommend applying an artificial 50% haircut to all non-cash collateral during your worst-case simulations. Why? Because when everyone rushes for the exit simultaneously, market liquidity vanishes, and your theoretical maximum potential exposure suddenly morphs into an unstoppable, compounding cash drain.

Frequently Asked Questions

How does maximum potential exposure differ from Value at Risk (VaR)?

While Value at Risk calculates the maximum loss you might expect over a specific timeframe within a standard 95% or 99% confidence interval, it deliberately ignores what happens inside that final, catastrophic 1% tail. The maximum potential exposure metric actively lives inside that extreme territory, mapping out the absolute financial devastation if everything goes wrong simultaneously. For example, a bank might report a daily VaR of 1.5 million dollars, yet its true peak exposure over a ten-year horizon could easily scale past 180 million dollars. As a result: relying solely on VaR to protect your institution against systemic collapse is akin to checking the weather report while ignoring a category 5 hurricane on the horizon.

Can a firm realistically reduce its peak exposure without shrinking its core portfolio?

Yes, you can aggressively mitigate this peak metric through smart structural engineering rather than sacrificing your market share. Implementing daily variation margin calls, setting up tri-party clearing houses, and utilizing legally enforceable

cross-product netting agreements will instantly slash those runaway numbers. If your gross exposure sits at 75 million dollars, a robust bilateral netting framework can frequently compress that risk down to a manageable 12 million dollars. But you must ensure these legal contracts are bulletproof across different international jurisdictions, otherwise your theoretical protection disappears during a cross-border bankruptcy proceeding.

What role do credit rating downgrades play in shifting this risk profile?

A sudden credit rating downgrade acts as an immediate accelerant that can cause your calculated exposure metrics to warp unpredictably. When a counterparty drops from an A rating to BBB-, triggering clauses inside the

ISDA master agreement often demand immediate, massive collateral mobilization. This sudden liquidity drain can force the struggling counterparty straight into insolvency, instantly turning your theoretical

peak financial vulnerability into a realized, systemic credit loss. It is a brutal paradox where the defensive mechanisms designed to protect your capital can ultimately trigger the exact default event you desperately wanted to avoid.

A definitive stance on systemic vulnerability

Treating peak risk metrics as optional compliance bureaucracy is a form of corporate Russian roulette. We are convinced that the next wave of corporate bankruptcies will not be caused by bad luck, but by a arrogant refusal to model the absolute limits of financial vulnerability. You cannot manage a crisis you refuse to quantify. Let's be clear: numbers do not lie, but the human desire to smooth over unpleasant, extreme data points is an ancient flaw. Relying on average historical outcomes is a coward's strategy in an era defined by radical economic shifts. Build your capital reserves for the terrifying storm depicted by your maximum potential exposure, or prepare to watch your entire enterprise wash away when the inevitable tide turns.