The Evolution from IAS 1 to IFRS 18: Why the IASB Blotted Out the Old Presentation Playbook

For decades, IAS 1 gave companies a long, loose leash. Chief Financial Officers loved the flexibility, but investors were increasingly drowning in a sea of non-GAAP alternative performance measures (APMs) that made comparing a tech giant in California with one in Frankfurt almost impossible. The thing is, the income statement had become a Wild West where "operating profit" meant whatever management wanted it to mean. IFRS 18 General Presentation and Disclosures finally steps in as the sheriff to clean up the town.

The Death of Wild West Operating Income and the Birth of Three Defined Categories

Under the old regime, companies routinely buried inconvenient expenses or highlighted bespoke definitions of core earnings. But that changes everything. The new standard creates three distinct operating, investing, and financing categories, which might sound suspiciously like the statement of cash flows, yet the classification rules are entirely distinct (and where it gets tricky, the definitions do not perfectly align). If a retail conglomerate based in London previously included foreign exchange gains on translation within its operating line, it must now critically evaluate whether those belong in the financing category under the strict IFRS 18 classification framework.

Management-defined Performance Measures Enter the Audited Arena

People don't think about this enough: MPMs (Management-defined Performance Measures) are now officially dragged into the footnotes of audited financial statements. If you shout an adjusted EBITDA figure from the rooftops in your press releases, you now have to reconcile it directly to the most comparable IFRS total right there in the notes, accompanied by a full explanation of why this metric provides useful information. Honestly, it's unclear whether this will chill management's love affair with adjusted metrics, or simply give auditors a massive collective headache during the 2027 transition cycle.

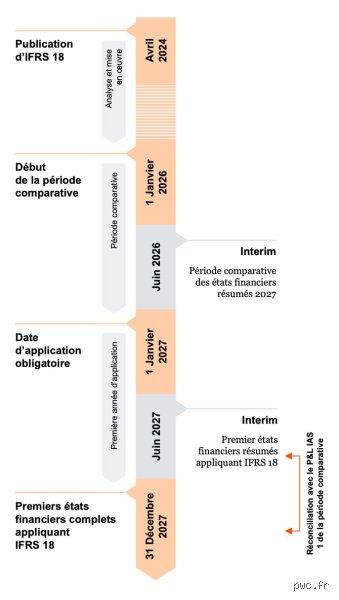

The Technical Verdict: Does IFRS 18 Require Retrospective Application?

Let's cut through the noise. According to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors, any new standard requires a full look-back unless the standard-setters explicitly grant a transition relief, which they did not do here. Consequently, the mandate for retrospective application under IFRS 18 means that when you publish your interim report for the period ending March 31, 2027, your comparative columns for the first quarter of 2026 must be fully restated to match the new structure. Do you really think your legacy ERP systems are ready to map transactions that happened sixteen months ago to entirely new income statement categories? We're far from it.

The Gritty Mechanics of Restating the 2026 Comparative Period

The issue remains that retrospective application is not just a copy-paste exercise. Companies must go back to the ledger for the 2026 financial year and reclassify every single line item into the new categories: operating, investing, financing, income taxes, and discontinued operations. For instance, an industrial manufacturer in Lyon that routinely receives interest income on cash balances must move that revenue out of its main top-line or "other income" bucket and firmly plant it into the investing category, unless its main business activity is providing financing to customers.

The Hidden Trap of the Retrospective Interim Report Reconciliations

But the real operational nightmare lies in the disclosures. IFRS 18 demands that companies provide a structured reconciliation between the income statement originally presented under IAS 1 for the 2026 comparative period and the newly restated statement. Each line item must be mapped out so investors can see exactly where the money went—such as showing how a portion of what was once "selling and administrative expenses" has been carved up to populate the new category of income and expenses from investments.

Deconstructing the New Income Statement Structure: Categories, Categories, and More Categories

The heart of the new standard lies in its structural rigidity, which forces a company's performance into a predefined mold. The operating category is now the default bucket; anything that does not fit into investing, financing, income taxes, or discontinued operations lands here by default. It is a sweeping change designed to capture all income and expenses from a company's main business activities, regardless of whether they are volatile or unusual.

The Operating Category as the Ultimate Catch-All Bucket

The IASB flipped the script by making the operating category a residual zone. I find this approach highly pragmatic, yet it introduces weird anomalies for diversified conglomerates where defining the "main business activity" feels like hitting a moving target. If a firm operates both a shipping fleet and an internal financing arm, the line between what constitutes an operating expense versus a financing cost blurs instantly, forcing management to make heavy-handed judgments that will undoubtedly draw scrutiny from regulators like ESMA.

Financing versus Investing: Drawing a Hard Line in the Financial Sand

We must look closely at how IFRS 18 splits the rest of the board. The investing category is strictly reserved for income and expenses from assets that generate returns individually and largely independently of other resources, such as investment property or equity-accounted joint ventures. Meanwhile, the financing category isolates the effects of transactions that involve only the raising of capital, including the unwinding of discounts on long-term lease liabilities under IFRS 16—a nuance that will shift millions out of operating results for heavy lessees.

Comparative Analysis: How Full Retrospective Application of IFRS 18 Distorts and Heals Financial Trends

When looking at the numbers, full retrospective application is a double-edged sword. On one hand, it heals the historical timeline, allowing an analyst to track a company's organic growth from 2026 to 2027 without a jarring structural break in the middle of the trendline. On the other hand, it distorts the historical reality that management was operating under at the time those 2026 decisions were actually made.

The Illusion of Comparability Across Capital Markets

Corporate financial analysts are rejoicing at the prospect of a uniform operating profit subtotal across international borders, as it eliminates the need to manually adjust for discrepancies in how different firms treat interest income or share-based payments. Yet, the illusion falls apart when you realize that two companies in the same sector can still interpret their "main business activities" differently, resulting in one classifying equity gains as operating and the other as investing. Hence, true cross-border comparability remains a distant utopia, despite the rigorous retrospective efforts forced upon corporate accounting departments globally.

Common mistakes and widespread misconceptions

The "presentation-only" optical illusion

Many practitioners look at the new presentation requirements and assume the changes are merely cosmetic. They are wrong. Because the standard fundamentally reshapes the structure of the income statement, you cannot simply reclassify numbers on the face of the financial reports without re-evaluating the underlying data aggregation. The question of does IFRS 18 require retrospective application finds its sharpest teeth here; companies must rebuild their comparative periods using entirely new definitions of operating, investing, and financing categories. The problem is that historical data systems were never configured to capture these distinct categories automatically. If you assume a simple mapping exercise will suffice, your comparative data will likely fail audit scrutiny.

Misjudging the scope of Management Performance Measures (MPMs)

Another frequent trap involves the disclosure of non-GAAP metrics, now formalised as MPMs. Executives often believe that since these metrics were previously disclosed in the management commentary, they sit outside the strict boundaries of restatement. Let's be clear: any MPM disclosed within the audited financial statements must comply with full retrospective treatment. This means recalculating your favourite bespoke metrics for the prior period using the new IFRS 18 discipline. It is a grueling exercise. Companies routinely underestimate the audit trail required to substantiate these comparative non-GAAP numbers, which explains why early dry-runs are collapsing under logistical weight.

Expert advice: Navigating the hidden operational trap

The operational headache of the stub period

Here is a little-known aspect that senior technical accountants are losing sleep over: the interim reporting mismatch during the year of adoption. When you launch your first quarterly or half-year report under the new regime, you must present fully restated comparative interim periods. Yet, many entities are focusing exclusively on the full-year comparative balance sheet and income statement. What happens to the internal controls required to track these changes on a month-by-month basis during the comparative year? The issue remains that legacy ERP systems cannot easily run parallel accounting structures. You might find yourself maintaining dual spreadsheets for 12 months straight, a recipe for human error that will irritate your sub-committees and auditors alike.

Proactive system architecture mapping

Our explicit recommendation is to implement a dual-ledger environment or a highly robust tagging solution immediately rather than waiting for the transition deadline. Do not rely on manual adjustments at year-end. Why risk a restatement qualification over avoidable system constraints? Except that modifying enterprise software takes time, which is an asset you are rapidly burning through. By embedding the IFRS 18 attributes directly into your chart of accounts today, the retrospective aggregation for the comparative period becomes an automated output rather than an annual forensic investigation.

Frequently Asked Questions

Does IFRS 18 require retrospective application for all baseline presentation changes?

Yes, the standard mandates full retrospective application in accordance with IAS 8, meaning entities must restate the comparative period presented in their first compliant financial reports. For a company adopting the standard for its annual period beginning on 1 January 2027, this means the 2026 comparative income statement must be completely rebuilt from the transaction level up. This requires a systematic recalculation of operating profit and the newly defined categories for every single line item. Estimates suggest that over 85 percent of listed entities will need to alter their primary financial statement layouts to achieve this compliance. As a result: your opening balances and historical presentations must be perfectly aligned to ensure seamless comparability.

How does the retrospective rule impact the disclosure of historical MPMs?

When an entity discloses Management Performance Measures, it must provide a full reconciliation to the most directly comparable IFRS 18 subtotal for both the current and the comparative periods. If a company introduces a new MPM in 2027, it cannot simply leave the 2026 column blank or un-reconciled. You must retrospectively calculate that metric for 2026 using the exact same methodology, unless it is impracticable to do so. In practice, true impracticability is an exceptionally high bar to clear in front of national regulators. Software firms analyzed during the comment letter phase indicated that recalculating historical non-GAAP metrics would increase their interim reporting disclosure volume by roughly 20 to 30 percent.

Are there any exemptions or transition reliefs available for first-time adopters of IFRS?

First-time adopters of international standards receive specific, targeted reliefs under IFRS 1 to alleviate the burden of rebuilding ancient financial history. However, for existing IFRS reporters, the standard offers virtually no escape hatches regarding the comparative period, saving a minor relief for interim periods in the first year of adoption. Specifically, an entity is permitted (but not required) to omit aligned comparative information for micro-level notes if the cost outweighs the benefit, though the primary statements remain strictly bound to restatement. In short, do not expect a free pass from your regulatory body. Statistics from past major standard transitions show that fewer than 5 percent of entities successfully claim true impracticability exemptions for comparative presentation.

A definitive perspective on the IFRS 18 transition

The corporate world is treats this standard as a mere filing annoyance, but we view it as a profound disruption to financial storytelling. The ultimate answer to whether does IFRS 18 require retrospective application is a resounding, uncompromising yes, and it will expose the soft underbelly of poor corporate data governance. Organizations cannot hide behind old aggregation habits anymore. We believe that those who delay their system upgrades will face severe market penalties through delayed financial reporting or qualified audit opinions. This is not an academic debate about accounting theory; it is a high-stakes operational race. Winners will leverage this mandated restatement to provide cleaner, more transparent metrics that lower their cost of capital. Losers will drown in a sea of manual spreadsheet corrections while trying to explain why their historical numbers no longer match their previous investor presentations.