The Post-Pandemic Landscape of Pharmaceutical Giants

The pharmaceutical sector has evolved into a battleground of contrasting corporate philosophies. People don't think about this enough, but the massive divergence in stock performance over the last three years isn’t just a fluke. It is a direct consequence of how each company deployed its capital during the chaotic boom times of the early 2020s. Pfizer rode the mRNA wave to historic heights, stuffed its pockets with cash, and then faced an absolutely brutal hangover as public health demands cratered. Merck, meanwhile, played a much steadier hand, anchoring its entire corporate existence around a single, world-conquering cancer immunotherapy drug.

Unraveling the Financial Trajectories

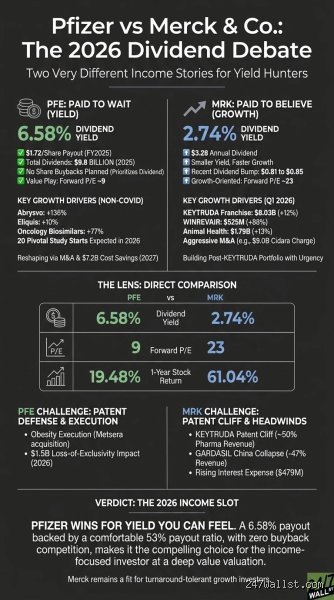

The numbers speak volumes about where these giants stand today. Pfizer enters mid-2026 trading at approximately $25.63 per share, boasting a forward price-to-earnings ratio of 19.81. That is a massive discount compared to Merck, which hovers around $118.72 with a premium P/E ratio pushing past 32.64. The issue remains that the market hates uncertainty, and Pfizer has spent the last twenty-four months swimming in it. Yet, the deep value proposition here is impossible to ignore if you have a stomach for volatility. Pfizer brought in $62.6 billion in total 2025 revenue, showing that despite losing its massive pandemic windfall, the core business is far from dead. Merck countered with an annual revenue of $65.01 billion, demonstrating remarkable top-line consistency that has driven its market capitalization up to an impressive $293.22 billion, nearly double Pfizer's $148 billion valuation.

Evaluating Pfizer's Deep Value and Pipeline Reconstruction

Where it gets tricky with Pfizer is looking past the wreckage of its COVID-19 franchise. Everyone knows the story of Comirnaty and Paxlovid dropping off a cliff. But that changes everything when you realize management didn't just sit on their hands; they went on an aggressive $43 billion shopping spree, highlighted by the acquisition of Seagen, to entirely rebuild their clinical pipeline from scratch. Honestly, it's unclear if this massive bet on targeted oncology will pay off immediately, but early indicators from the recent ASCO 2026 conference suggest the tide is turning. Pfizer presented stellar seven-year data for Lorbrena in treating advanced lung cancer, alongside strong readouts for Talzenna in prostate treatments.

The Yield Cushion and Cost Realignment

But what about the immediate payout for investors holding the bag? Pfizer spent a staggering $9.8 billion on cash dividends in 2025 alone, yielding an incredibly attractive percentage that hovers well over 6.5% at current compressed stock prices. Management has explicitly reaffirmed its full-year 2026 revenue guidance of $59.5 billion to $62.5 billion, proving that the operational baseline has finally stabilized. And they are aggressively hacking away at expenses. Their rolling cost realignment program is explicitly engineered to wring out $5.7 billion in net cost savings by the end of December 2026. If you buy the stock here, you are essentially getting paid a premium yield to wait out a massive corporate restructuring. It is a classic contrarian setup.

Mitigating Single-Asset Vulnerability

There is another hidden strength in Pfizer's current balance sheet that the market seems willfully blind to right now. Product diversification. No single asset inside Pfizer's stable accounted for more than 22% of its total 2025 revenue. Instead, the weight is distributed across a robust portfolio of blockbusters: Eliquis brought in $7.96 billion, the Prevnar vaccine family generated $6.49 billion, and Vyndaqel chipped in $6.38 billion. This means that if any single clinical trial fails, or if a specific patent expires prematurely, the company won't suffer a catastrophic operational collapse.

The Merck Juggernaut and the Impending Keytruda Patent Cliff

Now, flip the coin and look at Merck. The company has been an absolute darling on Wall Street, delivering a stellar return over the past twelve months that left Pfizer in the dust. Their return on equity stands at a phenomenal 18.94%, demonstrating elite managerial efficiency. Their free cash flow generation is equally monstrous, topping $14 billion. Analysts love this stock; nineteen major Wall Street analysts currently hold explicit buy ratings on it, with zero sell recommendations on the books. It sounds like a slam-dunk investment, right? Well, exception made for one massive, looming problem that keeps thoughtful macro investors up at night.

The 49 Percent Concentration Conundrum

Merck has an agonizingly high dependence on its mega-blockbuster cancer drug, Keytruda. In 2025, Keytruda accounted for a staggering 49% of Merck's total annual revenue. Let that sink in for a moment. Nearly half of a $290-plus billion company's top-line revenue hinges on a single therapeutic asset. And the clock is ticking loudly. Keytruda faces a major loss of exclusivity beginning in 2028. To counter this impending revenue crater, Merck has been aggressively buying up smaller biotech outfits, taking massive multi-billion dollar one-time charges in early 2026 to acquire companies like Cidara and Terns. These strategic moves are brilliant for the long term, but they severely depress short-term GAAP earnings, which explains why the stock recently suffered a sharp 3.19% single-day pullback as institutional investors digested the massive outlays.

Direct Head-to-Head Comparison of Investment Profiles

Choosing between these two corporate titans requires evaluating how much premium you are willing to pay for current operational momentum versus buying a discarded value play. It is an classic investment dilemma. Do you buy the expensive house in the perfect neighborhood, or the discounted fixer-upper with solid bones?

A Contrast in Valuation and Yield Metrics

Let's lay out the hard truth of the financial metrics side-by-side to see the stark contrast. Merck offers an incredibly efficient, highly profitable machine with a forward P/E of 12.41 based on adjusted figures, but its trailing twelve-month GAAP valuation remains highly inflated due to those necessary acquisition costs. Its dividend yield sits at a modest 2.86%, and with a dividend payout ratio currently stretching to 93.52%, there is virtually no room for management to raise that payout anytime soon. Pfizer, on the other hand, trades at an absolute cyclical trough. Its P/E ratio of under 20 offers a significant margin of safety. As a result: Pfizer provides a massive income stream that is more than double Merck's yield, backed by $13.1 billion in cold cash sitting in the bank to defend that payout while they hunt for new revenue streams. I believe the market is severely mispricing Pfizer's stability while ignoring Merck's concentration risks.

Common mistakes and misconceptions about big pharma investing

The pipeline optical illusion

Investors frequently glance at a company's phase 3 trial list and assume a massive pipeline guarantees future revenue. The problem is that clinical trial velocity does not equate to commercial velocity. You see a dozen molecules in late-stage development and assume Pfizer will automatically replicate its pandemic-era dominance. Except that oncology and immunology therapeutics possess an average attrition rate that would make a venture capitalist wince. Counting unapproved assets as locked-in revenue is a rookie blunder. Wall Street models already price in standard probability-of-success metrics, meaning a drug entering phase 3 only carries a fraction of its eventual commercial value in the current stock price.

The dividend yield trap

Look at the trailing yields and it is easy to get seduced by Pfizer's juicy payouts. But let's be clear: a high dividend yield is often the market's polite way of saying a company is starved for organic growth. Income seekers often mistake historical dividend stability for future financial health. When evaluating

Which is a better buy, Pfizer or Merck?, chasing the higher yield blindly ignores the payout ratio sustainability. Merck maintains a leaner payout profile precisely because Keytruda cash flows are being aggressively diverted into business development. A dividend is a cash distribution, not an economic moat.

Misunderstanding the patent cliff timeline

Many retail traders operate under the assumption that a patent expiration date behaves like a sudden financial guillotine. The reality is far more nuanced. When a blockbuster drug loses exclusivity, revenues do not instantly drop to zero on day one. Biosimilar manufacturing requires complex regulatory approvals and massive capital expenditure, which naturally slows down generic erosion. Conversely, savvy investors sometimes forget that aggressive price negotiation from state actors can hollow out a drug's profitability years before the actual patent expires.

The hidden factor: The antibody-drug conjugate (ADC) arms race

Beyond the standard small-molecule paradigm

While the financial media remains hyper-focused on Merck's Keytruda dependency, the real battlefield has shifted to targeted oncology architectures. Pfizer paid forty-three billion dollars to acquire Seagen, a massive bet on antibody-drug conjugates that essentially function as guided missiles for cancer cells. This wasn't just a routine acquisition; it was an entire corporate pivot designed to replace lost Comirnaty revenue.

The strategic valuation divergence

Why does this matter for anyone deciding

which pharma stock to purchase today? The issue remains that integrating a massive biotech acquisition takes years of operational friction. Merck, meanwhile, is utilizing a string of smaller, bite-sized licensing deals to diversify its oncology portfolio without bloating its balance sheet. If Pfizer successfully scales its newly acquired ADC platform, its current depressed valuation will look like an absolute steal in hindsight. Yet, execution risk is notoriously high in biologics manufacturing, meaning Pfizer is taking a much larger gamble on operational synergy than its conservative rival.

Frequently Asked Questions

Which company possesses a healthier balance sheet for long-term debt management?

Merck currently exhibits a significantly cleaner balance sheet compared to its primary competitor, especially when evaluating leverage ratios. Following the massive Seagen transaction, Pfizer saw its total debt swell to over sixty billion dollars, which pressures its credit rating and elevates interest expenses. Merck maintains a highly manageable debt-to-equity ratio of roughly zero point fifty-five, allowing it greater flexibility for future strategic acquisitions. Because higher interest rates increase the cost of refinancing, Merck's capital structure positions it much better to weather prolonged macroeconomic volatility. Consequently, conservative investors prioritizing fiscal discipline frequently favor Merck's current financial profile.

How do the projected earnings growth rates compare for the next five years?

Wall Street consensus estimates project a stark divergence in earnings trajectory between these two pharmaceutical titans through the late 2020s. Merck is anticipated to post a compounded annual earnings growth rate of approximately eleven percent, fueled by expanded indications for its oncology portfolio and robust animal health revenues. Pfizer, attempting to establish a post-pandemic baseline, faces a more volatile trajectory with projected near-term annualized growth hovering around four percent. Can Pfizer outperform these muted expectations if its newly acquired cancer pipeline delivers early regulatory victories? The data suggests that while Merck offers predictable, steady compounding, Pfizer represents a high-turnaround play with a wider distribution of potential financial outcomes.

What role do obesity and metabolic drug pipelines play in their current valuations?

Neither giant currently commands a dominant position in the lucrative GLP-1 market, a space currently monopolized by Eli Lilly and Novo Nordisk. Pfizer suffered notable setbacks with its oral GLP-1 candidate, danuglipron, discarding the twice-daily formulation due to high adverse event rates in clinical trials. Merck is approaching metabolic diseases from a different angle, advancing early-stage candidates that target dual pathways but remaining years away from commercialization. As a result: neither stock offers meaningful exposure to the current weight-loss boom, meaning their valuations are decoupled from this specific market frenzy. Investors looking for a pure-play metabolic growth narrative should look elsewhere, as both companies remain anchored to oncology, vaccines, and immunology.

Choosing the definitive pharmaceutical winner

The perpetual debate over

Which is a better buy, Pfizer or Merck? cannot be solved by staring at simple valuation multiples. We are looking at two entirely different corporate philosophies masquerading as similar large-cap value stocks. Merck represents an elite, highly focused compounding machine whose mastery of the oncology space justifies its premium pricing. Pfizer is an asymmetric turnaround story heavily discounted by a cynical market that has grown weary of post-pandemic earnings normalization. We believe that Merck's operational execution and superior balance sheet safety make it the superior investment choice for the foreseeable future. Chasing Pfizer's bloated dividend yield is a seductive gamble, but Merck's structural advantages in oncology defense offer far better risk-adjusted protection. Capital preservation dictates backing the company with clear visibility into its near-term earnings, rather than the one still digesting a massive corporate transformation.