The Structural Gravity of the Modern Household Ledger

We have been conditioned to believe that fiscal discipline is a war won in the trenches of minor discretionary sacrifices. That is a lie. The issue remains that macroeconomic shifts over the past four decades have fundamentally decoupled wage growth from the cost of basic societal entry tickets. According to data from the Bureau of Labor Statistics updated through recent quarters, the average American household allocates roughly 33.3 percent of its after-tax income solely to keeping a roof overhead. Add the mechanical costs of moving human bodies through geographic space, plus the volatile casino of medical billing, and you have consumed the vast majority of your paycheck before ever tasting a single crumb of food.

The Discretionary Distraction vs. Fixed Realities

People don't think about this enough: your streaming subscriptions are not the reason you cannot afford a down payment on a home. It is a comforting myth because it implies we possess granular control over our financial destinies. Yet, when the median home price in metropolitan areas like Austin, Texas or Denver, Colorado surged by unprecedented margins between 2020 and 2026, the structural game changed entirely. We are looking at a landscape where fixed, non-negotiable overhead commands absolute dominance over our wallets.

Why Averages Lie to the Middle Class

Here is where it gets tricky. Aggregate national data blends the billionaire in Aspen with the barista in Boston, smoothing out the terrifying peaks of actual lived experience. In high-cost-of-living areas, that nominal 33 percent allocation for housing frequently balloons to 50 percent or more. I find the conventional "50/30/20" budgeting rule—where half your income covers needs—to be utterly obsolete for anyone living in a major economic hub today. Experts disagree on whether this is a temporary inflationary hangover or a permanent structural reset, but honestly, it's unclear if standard middle-class salaries can ever truly recover their purchasing power without radical systemic intervention.

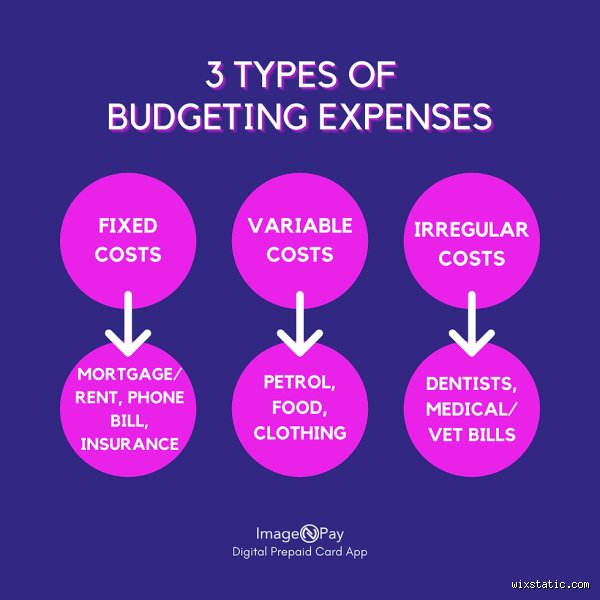

Housing: The Uncontested Champion of Income Depletion

Shelter is not merely a line item; it is a predatory financial vortex. Whether you are paying down a 30-year fixed mortgage or throwing capital into the bottomless pit of residential rent, housing represents the single largest transfer of wealth from individual labor to institutional capital. In 2024, Harvard's Joint Center for Housing Studies highlighted a staggering metric: a record 22.4 million renter households were classified as "cost-burdened," spending more than the traditional threshold of their earnings on rent alone. That changes everything for a generation trying to build equity.

The Mortgage Trap and the Rental Mirage

But wait, isn't homeownership the ultimate wealth builder? Except that the hidden friction costs of owning a piece of dirt—property taxes that compounding inflation drives upward, homeowners association fees that feel like localized extortion, and the inevitable 10,000-dollar roof replacement—frequently erase the paper gains realized by rising market values. Renting is no refuge either. Landlords in cities like Miami and Phoenix have weaponized algorithmic pricing software to squeeze every drop of consumer surplus out of tenants, creating a recurring expense that offers zero terminal value.

The Geography of Financial Despair

Consider the stark divergence between geographic realities. A mid-level software engineer in San Francisco might pull in 180,000 dollars annually, yet find themselves living in what amounts to genteel poverty because a basic two-bedroom bungalow commands a million-dollar premium. Meanwhile, that same relative purchasing power in Rust Belt markets like Cleveland, Ohio looks entirely different. And because our physical location dictates our access to high-paying labor markets, we find ourselves locked into an expensive geographic tax just to maintain the privilege of working.

Transportation: The Depreciating Liability We Refuse to Give Up

If housing is the silent anchor, transportation is the flashy, gas-guzzling engine of wealth destruction. It is the second pillar when evaluating what are the top 3 expenses. The American Automobile Association recently revealed that the average annual cost to own and operate a new vehicle has soared past 12,180 dollars. That is a breathtaking sum for an asset guaranteed to lose value the exact millisecond you drive it off the dealership lot.

The Auto Loan Crisis and the Illusion of Utility

We have normalized the 800-dollar monthly car payment. It is madness, really. Driven by cheap credit throughout the late 2010s and exacerbated by supply chain shocks that permanently altered manufacturer pricing strategies, consumers routinely sign up for 72-month or even 84-month loan terms. Because of this extended amortization, a significant percentage of drivers operate in negative equity, meaning they owe more on their vehicle than its actual intrinsic worth. Why do we willingly participate in this financial self-sabotage? Because our suburban infrastructure, designed around the sacred geometry of the interstate highway system, makes alternative options functionally impossible for the average commuter.

The Real Cost of Mechanical Mobility

Let us look beyond the monthly financing sticker price. The true drain comprises depreciation, comprehensive insurance premiums that have spiked due to complex vehicular technology, and volatile fuel costs. When a simple fender bender on a modern electric vehicle requires the wholesale replacement of an entire computerized sensor array, your local mechanic's bill transforms into a major financial crisis. We are far from the days when a wrench and some grit could fix the family sedan.

The Medical Monopoly: Why Healthcare is an Unpredictable Beast

Unlike shelter and transit, healthcare is an expense defined by its terrifying asymmetry. You can choose to live in a smaller apartment or drive a battered compact car, but you cannot negotiate with an inflamed appendix or a chronic autoimmune diagnosis. Hence, medical costs occupy a unique, psychologically corrosive space in the household budget. Even for individuals possessing employer-sponsored insurance, the out-of-pocket exposure remains immense.

Deductibles as the New Uninsured Margin

The rise of the High-Deductible Health Plan has effectively shifted the financial burden of wellness directly onto the shoulders of the consumer. It is a brilliant corporate strategy, except that it leaves families exposed to thousands of dollars in upfront costs before their insurance policy kicks in a single dime. As a result: many families choose to defer necessary medical interventions, a choice that inevitably leads to catastrophic health and financial outcomes down the road. A single trip to an out-of-network emergency room in a city like Chicago can result in a surprise bill capable of wiping out an entire year of diligent savings.

Common mistakes and dangerous blind spots

The obsession with minor line items

We lose sleep over five-dollar coffees. The problem is that skipping your daily latte does absolutely nothing when your mortgage consumes half of your take-home pay. People meticulously log every single organic avocado they purchase while completely ignoring the staggering interest rates on their depreciating assets. This hyper-focus on micro-expenses creates a false sense of financial righteousness. You cannot budget your way out of a catastrophic structural deficit caused by the top 3 expenses. Why do we self-flagellate over minor grocery bills? Because micromanaging a vegetable receipt feels easier than negotiating a salary increase or downsizing an oversized suburban home. Let's be clear: unless you fix the big three, your minor frugality is merely theater.

Underestimating the true cost of vehicle ownership

Most drivers calculate their transportation outlay solely by the monthly loan payment and occasional trips to the gas pump. Except that this math ignores the silent killer of wealth: sticker-shock depreciation. The moment you drive that shiny piece of metal off the dealership lot, your net worth plummets. Vehicles routinely lose 60% of their value within the first five years of ownership. Add in mandatory comprehensive insurance, registration fees, and the inevitable transmission failure. Suddenly, that reasonable three-hundred-dollar payment mutates into an eight-hundred-dollar monthly drain. We intentionally blind ourselves to these variables because a pristine vehicle feeds our fragile ego. Yet, ignoring these secondary automotive outlays is precisely how middle-class households trap themselves in perpetual paycheck-to-paycheck cycles.

Conflating tax refunds with financial health

An alarming number of professionals view a massive April tax refund as a triumphant financial victory. In reality, you just granted the government an interest-free loan for twelve months. When examining what are the top 3 expenses, taxes consistently rank near the pinnacle, but because the money is withheld before hitting our bank accounts, it remains psychologically invisible. Over 75% of individual taxpayers receive refunds annually, meaning millions of households voluntarily choke their monthly cash flow. You are celebrating the return of your own money while paying double-digit interest on credit card debt. It is a spectacular display of financial illiteracy.

The hidden tax of lifestyle creep

The phantom upgrade cycle

Every time your income moves upward, your baseline expectation of what constitutes a normal life shifts aggressively. This is the insidious mechanism of lifestyle inflation. As a result: your housing footprint expands, your vehicle gets sleeker, and your tax bracket intensifies. You do not feel any wealthier because your structural overhead expanded symmetrically with your new salary. The issue remains that the big three financial drains scale effortlessly alongside your success. To counteract this, experts recommend implementing a mandatory firewall. When you receive a raise, instantly route at least 50% of the net increase into automated investment vehicles before your brain can invent new needs. If you fail to intercept those funds, your fixed overhead will inevitably swallow them whole.

Frequently Asked Questions

What percentage of income should ideally go toward housing?

Traditional financial advisors love to parrot the classic 30% rule, but modern economic realities demand a much more nuanced calculation. Analysis of urban cost burdens reveals that over 42% of working professionals in major metropolitan areas now exceed this threshold just to secure a basic two-bedroom apartment. If your housing costs squeeze past this mark, you must aggressively compensate by slashing your secondary categories. Can you survive when your shelter consumes a massive portion of your paycheck? Yes, but only if you completely eliminate automotive debt and embrace a aggressively minimalist approach to transportation. The math simply does not work otherwise.

How can a remote worker optimize the top 3 expenses effectively?

Remote employment provides an unprecedented leverage point to fundamentally restructure your entire financial ecosystem. By untethering your income from a specific high-cost geographic node, you can immediately migrate to a lower-tax jurisdiction. This single geographical arbitrage move can instantly slash your state tax liability by up to 8% annually depending on your location. Furthermore, eliminating the daily corporate commute allows you to transition into a single-car household or discard vehicle ownership entirely. Which explains why remote workers who downsize their lifestyle aggressively see their savings rates double within a single calendar year.

Are taxes truly preventable, or are they just an inevitable burden?

While avoiding taxes completely is a myth reserved for illicit entities, legally minimizing your liability is well within your control. Failing to utilize tax-advantaged accounts like a 401k or a Health Savings Account is tantamount to leaving free cash on the table. Maximizing these vehicles can reduce your adjusted gross income by up to $23,000 or more depending on current federal limits. Most citizens passively accept their tax bill as an immutable act of God. In short, your tax burden is highly malleable if you stop treating financial planning as an annual chore and start treating it as a weekly strategy.

An uncomfortable truth about your money

Stop looking for magical investment shortcuts when your foundational structure is completely compromised. The data clearly demonstrates that housing, transport, and taxation dictate your ultimate financial destiny. You cannot out-earn reckless structural liabilities, nor can you save enough pennies to overcome an inflated mortgage. We must face the reality that true financial autonomy requires making drastic, deeply unpopular choices about where we live and what we drive. (And yes, your friends will probably judge you when you downsize to a older hatchback). Let's stop pretending that minor lifestyle tweaks will save us from systemic overspending. It is time to ruthlessly audit the big three or accept perpetual mediocrity.