The Hidden Machinery of Dividend Taxation and Why Free Cash Isn’t Always Free

Let us get something straight right away because most retail investors get this completely wrong. Wall Street loves to pitch the dream of effortless, recurring wealth flowing into your brokerage account while you sleep. But the IRS views that incoming cash through a highly specific, fragmented lens. The government splits these payouts into two distinct buckets: qualified and ordinary. The distinction matters immensely because ordinary payouts face standard, aggressive income tax rates while qualified distributions enjoy massive, preferred treatment.

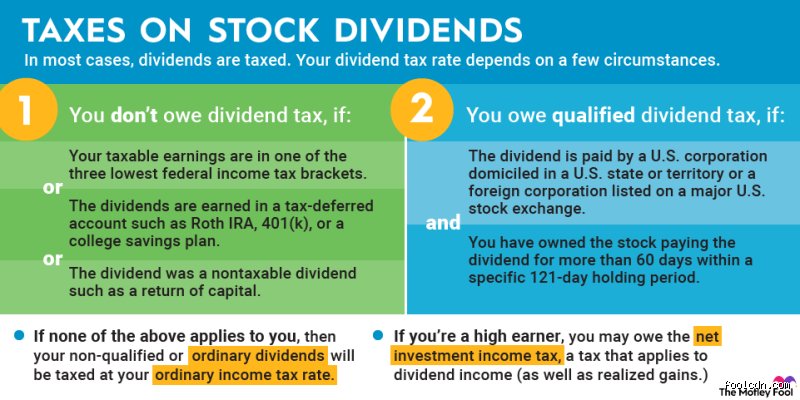

Decoding the IRS Rulebook for Qualified Distributions

To qualify for those coveted low rates, the underlying asset must meet stringent criteria. It has to be issued by a domestic corporation or a qualified foreign entity. Furthermore, you must hold the underlying stock for more than 60 days during a 121-day window that begins 60 days before the ex-dividend date. Miss that window by a single afternoon? That changes everything. Suddenly your tax-free dream evaporates into standard income brackets.

The Disappointment of Ordinary and Unqualified Payouts

Where it gets tricky is dealing with specialized investment vehicles. Real Estate Investment Trusts, commonly known as REITs, alongside business development companies, do not get the preferred treatment. Because these entities pass through their income directly to avoid corporate tax, the cash hitting your account is treated as ordinary income. In short, it is taxed just like the salary from your day job. If you are sitting in a high-bracket zip code like New York or San Francisco, ordinary payouts get chewed up fast by the taxman.

How Much Dividend Can I Earn Before Paying Taxes in the Current System?

The magic number relies entirely on your overall filing status and your standard deductions. People don't think about this enough, but your investment profits do not exist in a vacuum. The IRS stacks your capital gains on top of your normal salary. If your regular wages already push you past the threshold, every single cent of your dividend income faces immediate taxation.

Breaking Down the Zero Percent Tax Brackets

For individuals staring down the current fiscal year, the 0% tax rate applies up to a taxable income of $44,625. If you file jointly with a spouse, that ceiling doubles to $89,250. Yet, the issue remains that these numbers represent taxable income, not gross income. By utilizing the standard deduction of $13,850 for single filers, a person with zero other income could theoretically pull in nearly $58,475 in qualified payouts without triggering a federal tax bill. But honestly, it's unclear how many people actually live solely off unearned income without a side hustle or pension tipping the scales.

The Stacking Effect and the Adjusted Gross Income Trap

Imagine a real-world scenario involving an investor named Marcus in Austin, Texas. Marcus earns a modest salary of $40,000 as a graphic designer. He also holds a robust portfolio of blue-chip stocks yielding $10,000 in qualified distributions annually. You might think his investments are safe under the threshold. Except that the IRS counts the salary first, meaning the last $5,375 of his dividend income spills over into the 15% capital gains bracket. See how fast that tax-free threshold shrinks when real life interferes?

Advanced Threshold Tactics: Navigating the Net Investment Income Tax

When your portfolio starts generating serious wealth, the landscape shifts dramatically. You move past the basic brackets and enter a territory where stealth taxes lurk. The most prominent of these is the Net Investment Income Tax (NIIT), a 3.8% surcharge designed to fund healthcare initiatives. This is where conventional wisdom fails because the NIIT hits you regardless of whether your dividends are qualified or ordinary.

The High-Earner Danger Zone

Once your Modified Adjusted Gross Income breaches $200,000 for single filers or $250,000 for married couples, the rules change completely. That 3.8% levy stacks directly on top of your existing 15% or 20% capital gains rates. As a result: an investor in the highest tier could look at a federal tax rate of 23.8% on their corporate distributions. It is an aggressive bite out of your cash flow. I believe most wealth managers spend way too much time picking stocks and nowhere near enough time structuring portfolios to avoid this exact threshold trap.

The Structural Divide: Taxable Accounts Versus Sheltered Vehicles

Where you hold your assets determines your tax liability far more than what specific stock you buy. A regular taxable brokerage account subjects you to annual reporting via Form 1099-DIV. Every single payment received during the calendar year must be accounted for on Schedule B of your Form 1040, triggering immediate liability if you are past the limits.

The Absolute Immunity of Retiring Accounts

Contrast that with placing high-yield assets inside a Traditional IRA or a 401k structure. Within these tax-deferred shells, you can accumulate thousands of dollars in annual payouts without paying a dime in real-time taxes. The downside? When you eventually withdraw those funds in retirement, the IRS taxes the distributions as ordinary income, completely stripping away the qualified status advantage. We are far from a perfect solution here. Experts disagree heavily on whether it is wiser to exploit the 0% capital gains rate now in a taxable account or take the upfront deduction in a retirement wrapper. But if you hold a Roth IRA, the story changes completely because qualified distributions from a Roth are entirely tax-free after age 59 and a half, presenting the ultimate loophole for aggressive income investors.

Navigating the Trapdoor: Common Dividend Tax Misconceptions

Many retail investors operate under the comforting illusion that tax authorities only look at the final number on a year-end statement. The problem is, tax compliance is rarely that accommodating. How much dividend can I earn before paying taxes depends entirely on your total financial footprint, not just your brokerage account.

The "Free Money" Illusion of DRIPs

You automatically reinvest your payouts, so you haven't technically touched the cash, right? Wrong. Except that the IRS—and most global tax authorities—views a Dividend Reinvestment Plan (DRIP) as a two-step transaction. First, you received the cash. Second, you purchased more shares. Because you never pocketed the physical dollars, you might assume it is a non-taxable event. It isn't. Every single automated fractional share purchase triggers a taxable event in the year it occurs. This remains true even if your account balance never leaves the brokerage platform. Failing to track these micro-transactions leads to a massive headache when calculating your adjusted cost basis later.

Confusing Gross Payouts with Net Returns

Let's be clear: a 1099-DIV form does not care about your sentimentality. Investors frequently look at their net deposits and calculate their liability from that deflated figure. They completely overlook the fact that foreign withholding taxes might have already chewed through the headline amount. If a Swiss company retains 35% of your payout at the source, your baseline calculation is warped from the start. You must report the gross amount. Consequently, you might owe domestic taxes on money that never even reached your local bank account, unless you correctly claim a foreign tax credit.

The Accumulation Share Secret: An Expert Workaround

If the friction of annual taxation irritates you, a structural shift in your portfolio might be the antidote. Most investors default to distributing funds. They want to see the cash hit the ledger. Yet, choosing accumulation units (often labeled as "Acc" in fund prospectuses) alters the entire tax equation for specific jurisdictions.

The Power of Structural Deferral

Why trigger an annual tax bill when you can let the underlying fund handle the heavy lifting? In an accumulation fund, the dividends are directly rolled into the fund's net asset value (NAV) without being distributed to shareholders. In certain tax jurisdictions, this transforms what would have been an annual income tax liability into a long-term capital gains liability down the road. You effectively defer your tax obligation until the moment you sell the shares. This allows the money that would have gone to the government to compound for decades. Are you willing to trade immediate cash flow for exponential long-term growth? For high earners, this strategy completely changes the answer to how much dividend earnings are tax-free by shifting the goalposts entirely.

Frequently Asked Questions

Does the standard deduction shield my dividend income from federal taxes?

Yes, the standard deduction can protect your investment income, but only if your total aggregate income falls below the specific annual threshold. For a single filer, if your combined wages, interest, and dividend distributions remain under the standard deduction limit, you will owe nothing. The issue remains that ordinary dividends are taxed at standard income rates, meaning they eat into this deduction space alongside your salary. Qualified dividends, however, enjoy a 0% tax rate if your total taxable income stays below the threshold. This means a single filer can technically receive thousands in qualified payouts entirely tax-free, provided their other income streams do not push them into the next bracket.

How do municipal bond dividends differ from corporate stock payouts regarding taxes?

Municipal bonds operate in an entirely different regulatory atmosphere than standard corporate equities. When you receive distributions from a municipal bond issued by your home state, that income is generally exempt from both federal and state income taxes. Which explains why high-net-worth individuals flock to these instruments to lower their overall tax brackets. Corporate dividends, on the other hand, enjoy no such sweeping historical exemptions and are always subject to federal oversight. As a result: municipal payouts allow you to maximize your cash flow without constantly recalculating your tax-free thresholds. However, the yields on these bonds are typically lower to reflect their privileged tax status.

Can I use capital losses to offset the taxes I owe on my dividend income?

You cannot directly use capital losses to cancel out qualified dividend income in an unlimited fashion. Net capital losses are primarily used to offset capital gains realized during the same tax year. If your losses exceed your gains, you can only use a maximum of $3,000 of those excess losses to offset ordinary income, which includes your dividend distributions. Any loss beyond that specific threshold must be carried forward to subsequent tax years. In short, you cannot simply wipe out a massive dividend tax bill by selling a bunch of losing stocks at the end of December.

The Final Verdict on Dividend Optimization

Stop treating tax optimization as a passive game of waiting for the right forms to arrive in the mail. Maximizing tax-free dividend income requires an aggressive, intentional asset location strategy that most retail investors are simply too lazy to implement. Relying solely on basic exemptions is a fool's errand that guarantees you will overpay the government. (And let's face it, the state isn't going to send you a thank-you note for your financial ignorance). Real wealth generation requires you to aggressively utilize tax-advantaged accounts like IRAs or ISAs while structurally adjusting your portfolio toward qualified distributions. We must acknowledge that tax codes are inherently fluid, meaning what works perfectly today might be completely obsolete by the next legislative cycle. Take a definitive stance on your portfolio structure right now, lock in your allocations, and stop letting preventable taxes erode your compounding machine.