The Anatomy of the Rumour: Where Does the Forty Percent Figure Come From?

Go to any backyard barbecue in Calgary or a coffee shop in Halifax, and you will eventually hear someone complain that the government gobbles up nearly half of their salary. It feels true. When you watch federal tax, provincial tax, Canada Pension Plan contributions, and Employment Insurance premiums vanish from your bi-weekly pay stub, the psychological damage is real. But human perception is a terrible calculator.

The Fraser Institute Effect and Consumer Tax Indexing

Much of this specific statistical panic stems from annual reports published by right-leaning think tanks, most notably the Fraser Institute. Their "Tax Freedom Day" calculations regularly assert that the average Canadian family spends over 40% of its income on taxes, but here is where it gets tricky because they lump every conceivable levy into one giant bucket. We are talking about corporate taxes passed down to consumers, property taxes, gas taxes, liquor markups, and import duties. Is it a valid macro-economic metric? Perhaps. But it does not mean a mid-career graphic designer making $75,000 in Toronto is writing a check for $30,000 to the government. People don't think about this enough, resulting in a distorted view of personal liability.

The Psychological Weight of the Deductions Column

Look at your last pay statement. If you are an employee, your employer does the dirty work of withholding tax at source. Because you never actually hold that gross income in your hands, the missing chunk feels like a penalty rather than a staggered contribution. And because our brains focus on the highest numbers we see in news headlines—like the top combined marginal rate in Ontario hitting 53.53% for ultra-wealthy individuals—we mistakenly assume that percentage applies to the whole pie.

Marginal Versus Effective Rates: The Mathematical Reality Check

This is the hill where tax literacy either triumphs or dies a painful death. Canada employs a progressive taxation system, meaning your income is chopped up into distinct slices, and each slice is taxed at a progressively higher rate. You do not just hit a threshold and suddenly watch your entire salary get multiplied by a higher percentage. That changes everything.

How the Brackets Actually Stack Up in 2026

For the 2026 tax year, the federal government sets its lowest bracket at 15% for income up to roughly $55,000. If you earn $60,000, only the five grand above that initial threshold faces the next federal rate of 20.5%. Your provincial tax gets stacked on top of this through a similar tiered system. Let us look at a concrete example: a nurse in Vancouver named Sarah earning $90,000. Her top marginal rate might hover around 31%, meaning the next dollar she earns over time will be taxed at that amount. Yet, her average effective tax rate—the actual total tax paid divided by her total income—is only about 22%. We're far from it, that mythical forty percent boogeyman.

The Disappearing Act of Deductions and Credits

But wait, it gets even lower. Nobody talks about the non-refundable tax credits that every Canadian is entitled to claim. The Basic Personal Amount allows you to earn over $15,000 federally before you owe a single dime in federal income tax. Toss in Registered Retirement Savings Plan deductions, childcare expenses, and the Canada Workers Benefit for lower-income households, and the actual cash flowing toward Ottawa shrinks drastically. I analyzed a mock tax return for a single parent in Montreal earning $50,000; after provincial family allowances and federal carbon tax rebates are factored in, their net tax burden dropped to the single digits. Honestly, it's unclear why the public debate ignores these offsets so aggressively.

The Silent Accumulation of Consumption and Hidden Levies

Yet, the defenders of the 40% narrative are not entirely hallucinating, except that their grievance lies in consumption, not production. Income tax is merely the front door of the Canadian fiscal house. The side windows and back doors are where the remaining wealth quietly leaks out through daily living expenses.

The GST, HST, and the Retail Penalty

Every time you buy a coffee, a pair of boots, or a laptop, the cash register rings up an extra fee. In Atlantic provinces like Nova Scotia and New Brunswick, the Harmonized Sales Tax adds a whopping 15% to most transactions. Cook a meal at home? Basic groceries are zero-rated. Buy a pre-made salad at a convenience store? Pay up. This secondary layer of taxation is inherently regressive because a lower-income worker spends a far greater proportion of their paycheck on taxed goods than a corporate executive does, meaning their real-world consumption tax rate is disproportionately heavy.

Excise Duties and Municipal Demands

Then come the specific penalties on modern existence. Drive a car to work in Vancouver? You are paying provincial fuel taxes, federal carbon taxes, and TransLink transit levies baked directly into the pump price. Own a modest bungalow in Winnipeg? Expect a annual property tax bill of $4,000 to keep the streetlights on and the snow plows moving. When you add up the provincial sales tax, carbon levies, sin taxes on cannabis and alcohol, and municipal assessments, the total chunk of change redirected to various levels of government starts crawling closer to that infamous forty percent mark for the middle class. Experts disagree on whether grouping these together is intellectually honest, but as a result: the consumer feels the pinch regardless of what the academic charts say.

Common Misconceptions Surrounding Canadian Taxation

The Marginal vs. Average Rate Trap

You look at a tax bracket, see 43%, and panic. Let's be clear: this is the single biggest blunder people make when calculatedly trying to figure out if Canadians pay 40% in taxes. Canada utilizes a progressive tax system. If your income ticks into a higher bracket, only the dollars within that specific sliver face the higher rate. Your first $53,359 of taxable income in 2026 is taxed at the lowest federal rate of 15%, regardless of whether you earn fifty thousand or five million. The problem is that psychological sticker shock blinds us to the blending effect. Your average tax rate—the actual math of total taxes divided by total income—is invariably lower than your marginal rate. To claim everyone drops nearly half their paycheck to the Canada Revenue Agency is a statistical illusion built on misunderstanding how brackets stack.

Ignoring the Interprovincial Chasm

Canada is not a fiscal monolith. A software engineer pulling in $150,000 in Vancouver faces a vastly different reality than an identical earner in Montreal. In Quebec, provincial brackets escalate rapidly, pushing the combined marginal rate past the 40% threshold much faster than in British Columbia or Alberta. Because of this provincial tug-of-war, blithely generalizing the tax burden of an entire subcontinent is absurd. The issue remains that national averages mask these massive regional discrepancies. Someone in Calgary might enjoy a flat 10% provincial rate up to $148,269, while an Ontarian navigates a completely different, surtax-laden labyrinth. Regional tax disparities distort national statistics profoundly.

The Hidden Reality of Consumption and Corporate Cost Shifting

The Value-Added Tax Invisibility

Income tax is only half the battle. What happens when you actually spend your remaining cash? Between the federal Goods and Services Tax (GST) and various Provincial Sales Taxes (PST), or the combined Harmonized Sales Tax (HST) which hits 15% in Atlantic Canada, consumption taxes quietly erode your purchasing power. And yet, these are rarely factored into the emotional debate over whether Canadians pay 40% in taxes. It gets worse when you account for hidden excise taxes on fuel, alcohol, and cannabis. You might boast a modest 22% average income tax rate, but your lifestyle choices might easily push your total government tribute past that mythical forty percent marker. Except that we rarely track our receipts with the same fury we reserve for our T4 slips.

The Strategy of Corporate Integration

For small business owners, the game changes entirely through a concept known as integration. The Canadian tax system is theoretically designed so that an individual earning money through a corporation pays roughly the same total tax as someone earning salary directly. Business owners utilize the Small Business Deduction to pay a low initial corporate tax rate, often around 9% to 12% depending on the province, on the first $500,000 of active business income. This allows for massive tax deferral opportunities. By leaving profits inside the corporation to reinvest, entrepreneurs cleverly dodge high personal tax brackets for decades, exposing the simplistic narrative of a universal 40% burden as highly incomplete.

Frequently Asked Questions

Do middle-class Canadians pay 40% in taxes on average?

No, the typical middle-class Canadian family does not forfeit 40% of their gross income directly to income taxes. According to baseline data from the Fraser Institute and Statistics Canada, an average Canadian family earning approximately $105,000 confronts an effective personal income tax rate closer to 12% to 15%. When you aggregate all forms of taxation, including carbon levies, property taxes, and the 13% HST found in Ontario, the total tax bill expands significantly. Even with these consumption taxes piled onto the ledger, the total effective rate for a middle-income household rarely touches the 40% threshold. Only when households climb into the top 10% of earners, typically crossing the $250,000 threshold, does the combined total tax rate genuinely begin to hover around or exceed that mark.

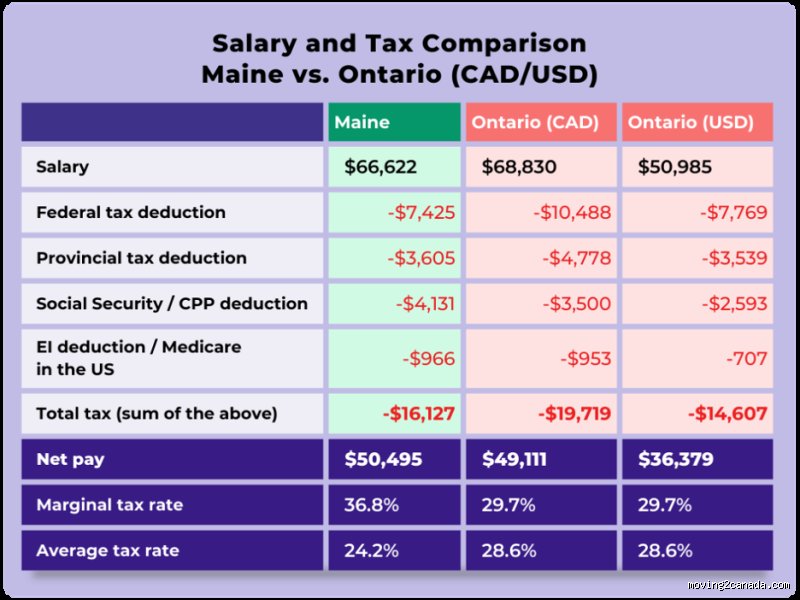

How does the Canadian tax burden compare directly to the United States?

The comparison is highly nuanced because Americans face state taxes, local sales taxes, and massive out-of-pocket healthcare premiums that Canadians largely avoid. A high earner in California or New York can easily see a combined marginal tax rate surpassing 50%, which rivals or exceeds the top brackets in provinces like Quebec and Nova Scotia. Conversely, low and middle-income Americans often enjoy lower federal brackets and a larger standard deduction than their northern neighbors. Do Canadians pay 40% in taxes while Americans pay significantly less? Which explains why looking only at statutory rates is deceptive; when you calculate the mandatory private health insurance costs that act as a de facto tax in the United States, the net financial disposable income gap between the two nations shrinks considerably for the average citizen.

Can you legally reduce your effective tax rate below the top brackets?

Absolutely, because the Canadian tax code provides robust mechanisms specifically engineered to lower your taxable income footprint. By maximizing your Registered Retirement Savings Plan (RRSP) contributions, you can deduct up to 18% of your earned income from the previous year, capped at $33,610 for the 2026 tax year, directly lowering your marginal exposure. Furthermore, utilizing a Tax-Free Savings Account (TFSA) ensures that investment growth and subsequent withdrawals remain entirely shielded from the Canada Revenue Agency. Parents can also leverage the Canada Child Benefit, which provides tax-free monthly payments based on adjusted family net income. Through diligent long-term planning and savvy utilization of these legislated deductions, even high-earning individuals can systematically depress their effective tax rate well beneath the dreaded 40% benchmark.

Beyond the Numbers: The True Value of the Canadian Fiscal Contract

Fixating blindly on a arbitrary forty-percent figure misses the entire philosophical point of the Canadian economic experiment. We must acknowledge that taxation is not merely money extracted into a void; it is a direct purchase of societal infrastructure. Are we getting a raw deal when our healthcare systems are straining under historic administrative backlogs? Perhaps, but we must also account for subsidized university tuitions, robust parental leave benefits, and clean public spaces that would otherwise demand private financing. As a result: evaluating the system requires looking at net utility rather than raw percentages. We cannot reasonably complain about the price of admission while simultaneously enjoying the safety net that prevents catastrophic financial ruin during medical emergencies. In short, the system is undeniably expensive, but it represents a deliberate cultural choice to prioritize collective stability over unbridled individual accumulation.