Counting the Seven-Digit Elite: The Anatomy of Ultra-High Net Worth

To understand the sheer magnitude of this group, we have to establish what it actually means to hold thirty million dollars in private assets. In institutional finance, anyone crossing this specific threshold is designated as an Ultra-High-Net-Worth Individual (UHNWI). The thing is, regular multi-millionaires—the people with a comfortable five million in a brokerage account—are playing an entirely different game. When a family office tallies a client’s net worth to check if they qualify for this echelon, they calculate investable cash, private corporate equity, massive art collections, and primary residential real estate, minus any outstanding liabilities. People don't think about this enough, but liquid cash is rarely the largest component here.

The Realities of Asset Allocation

Where it gets tricky is that these fortunes are highly consolidated in private enterprises. It is a massive misconception that the ultra-wealthy keep their money sitting in commercial bank accounts waiting for market downturns. Instead, private equity holdings, commercial real estate portfolios, and heavily structured family trusts comprise the bulk of their balance sheets. Think about it: a tech founder in Austin might technically own a $35 million valuation in a privately held software firm, yet her actual liquid checking account holds less than half a million dollars. That changes everything when analyzing economic resilience because these assets are tied directly to corporate valuations rather than standard retail banking liquidity.

The Invisible Baseline of Global Capital

The global ultra-wealthy make up just about 1% of the total millionaire population, yet they control an utterly disproportionate share of the world's private capital. Honestly, it's unclear exactly how much shadow equity remains hidden in offshore structures, but conservative estimates from major wealth intelligence firms suggest this elite cohort holds more than $59.8 trillion in combined net worth. That massive concentration of purchasing power explains why high-end asset markets barely flinched when central banks hiked interest rates globally. The mainstream economy decoupled from the luxury asset tape years ago.

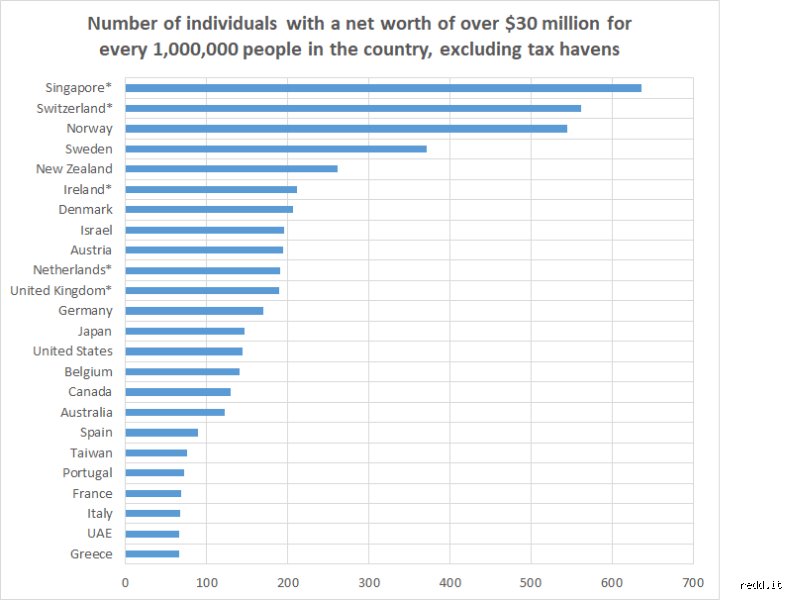

The Geopolitical Epicenters of Seven-Digit Fortunes

The geographical distribution of these individuals is radically uneven. The United States continues to dominate global wealth creation with an iron fist, currently boasting a staggering 251,000 UHNWIs within its borders. That massive pool means the US alone commands roughly 35% of the entire global ultra-wealthy population. But don't look away from Asia.

The Rising Empires of Private Wealth

Mainland China securely occupies the second place globally, tracking 121,000 individuals who have breached the thirty-million-dollar mark. Yet, the real shockwave is happening further south. India’s ultra-rich population has experienced an explosive 63% surge over the last five years, climbing steadily to 19,877 ultra-wealthy individuals in 2026. This phenomenal rate of wealth compounding in Mumbai, Delhi, and Bengaluru is completely altering luxury capital flows across the Asia-Pacific region. We are far from the days when European old money dictated the global markets.

The Resilient Old Guard of Europe

Europe still holds its ground, though its growth rates look remarkably sluggish compared to the fierce momentum of emerging Asian markets. Germany remains the undisputed economic powerhouse of the continent, hosting 38,200 ultra-wealthy citizens. The United Kingdom follows behind with 27,800, while France maintains an elite roster of 21,500 people crossing that $30 million mark. But these traditional hubs are facing structural headwinds—heavy domestic taxation, complex regulatory frameworks, and shifting corporate migration patterns are forcing many wealthy families to reconsider where they maintain their primary legal residences.

The Mechanics Behind the Recent Wealth Explosion

How did the world add over 162,000 ultra-rich individuals to the global roster in a mere five years? The answer lies in the dramatic transformation of private capital markets and alternative investments. While standard stock market indices experienced extreme volatility, the private markets where these individuals hold their core equities experienced unprecedented scaling. As a result: boutique tech enterprises, localized real estate syndicates, and specialized credit funds became massive engines of wealth acceleration.

The Decoupling of Trophy Real Estate

The elite real estate market has broken free from conventional economic gravity. Knight Frank’s Prime International Residential Index recorded a solid 3.2% average rise across 100 luxury markets worldwide last year. In cities like Tokyo, prime luxury real estate skyrocketed by an unbelievable 58.5% because a weak yen turned high-end developments into a massive dollar-denominated value play for international buyers. Dubai printed an equally astonishing 251% increase over a multi-year run, establishing itself as the undisputed capital of global super-prime migration. Wealthy families are hoarding trophy real estate as a critical vehicle for long-term wealth preservation, treating square footage in major metropolises like sovereign gold.

The Performance of the Luxury Investment Index

Collectibles have shifted from being mere hobbies to highly sophisticated, asset-backed collateral plays. The Knight Frank Luxury Investment Index stabilized dramatically after a period of broad correction, with museum-grade art surging by 13.6% over the last twelve months. Consider the historic auction prints in New York and Geneva this year—major single-owner collections hammered in at massive numbers, including standout modern masterpieces selling for over $230 million. High-end timepieces like Patek Philippe’s Nautilus models or rare Rolex references posted a 5.1% increase, demonstrating that when global liquidity expands, the supply of iconic luxury assets remains stubbornly finite. Private banks are now actively lending massive lines of credit against these physical collections, allowing the wealthy to access millions in liquidity without triggering capital gains taxes through an outright sale.

The Private Wealth Tier System: Where Do They Sit?

To truly grasp what a community of 713,626 ultra-wealthy people looks like, you have to break down the broader hierarchy of global affluence. It is easy to lump everyone with a high net worth into a single generic bucket, but the structural realities of someone holding two million dollars are worlds apart from someone managing thirty million. The global wealth pyramid is extraordinarily steep at the apex.

The Mass Affluent vs. The Ultra-Wealthy

The base of the global wealth pyramid holds tens of millions of people who belong to the mass affluent or standard millionaire classes. There are over 50 million individuals worldwide whose net worth sits somewhere between $1 million and $5 million. Except that these people are primarily dependent on mainstream primary residences, standard retirement portfolios, and corporate salaries. They are highly vulnerable to localized inflation, local property tax hikes, and traditional employment shocks. When you step over the line into the $30 million plus tier, those domestic economic worries completely vanish. You enter a realm where wealth becomes entirely institutionalized, managed by dedicated multi-family offices that deploy capital across multiple continents, currencies, and tax jurisdictions simultaneously.

The Elite Stratosphere of the Billionaire Class

If the UHNW class is exclusive, the billionaire cohort is an absolute statistical anomaly. There are currently just 3,110 billionaires on earth. According to recent data from Altrata’s Billionaire Census, these individuals make up a microscopic 0.7% share of the ultra-high-net-worth population, yet they control an outrageous 24% of the entire UHNW wealth stock. I find it fascinating that the line between a $30 million fortune and a $1 billion fortune is defined almost entirely by the nature of asset ownership. While the average ultra-wealthy individual might own a highly successful regional manufacturing firm or a lucrative chain of medical clinics, billionaires almost universally control massive, publicly traded multinational corporations or colossal private conglomerates. The volatility they experience is massive—roughly 10% of lower-tier billionaires worth between $1 billion and $2 billion drop out of the club every single year due to shifting equity prices—whereas fortunes built on private enterprise tend to remain incredibly stable over generations.

The Blind Spots: Common Misconceptions About the Multi-Millionaire Club

Most observers assume that tracking the ultra-wealthy is as simple as counting corporate stock filings. It is not. The first major error is the conflation of public equity with total net worth. When we ask how many people have over $30 million, the public imagination immediately conjures images of tech founders holding volatile shares. The problem is that a massive portion of ultra-high-net-worth individual (UHNWI) wealth is buried deep within private equity, commercial real estate, and sprawling family offices. These private holdings do not register on standard stock tickers, meaning public data represents just the visible tip of a very deep iceberg.

The Mirage of Liquid Cash

Do you honestly believe these individuals keep millions sitting passively in a standard checking account? Let's be clear: paper wealth is distinct from liquidity. A real estate tycoon might control a portfolio valued at $45 million, yet their actual cash reserves could be less than $500,000. Because their capital is aggressively deployed across illiquid commercial developments, their daily purchasing power relies heavily on lines of credit. And this distinction matters immensely when calculating global wealth brackets, as a sudden real estate downturn can instantly evaporate someone's UHNWI status on paper while leaving their physical lifestyle entirely unchanged.

Geographic Counting Discrepancies

Different wealth intelligence firms utilize wildly contrasting methodologies to track how many people have over $30 million globally. Knight Frank might flash one figure, while Wealth-X offers an entirely separate calculation. Why? The issue remains that some models rely heavily on primary residence values, whereas other algorithms completely discount residential real estate to focus purely on investable assets. If a pent-house owner in Manhattan holds a $32 million property but carries a $10 million mortgage, does he belong in the club? Depending on which analyst you ask, the answer changes completely, which explains the frustrating statistical variance across major wealth reports.

The Shadow Machinery: What Everyone Misses About UHNW Growth

The general public obsesses over luxury spending habits, but the true engine of the $30 million cohort is institutional-grade tax optimization. It is not about earning more; it is about losing less. Once a family crosses the threshold into ultra-high-net-worth territory, they stop interacting with retail banks. Instead, they build bespoke legal structures designed specifically to shield assets from inflation and fiscal policy. How many people have over $30 million largely depends on how successfully those individuals navigate international trust laws and jurisdictional boundaries.

The Sovereign Shifting Strategy

The truly wealthy do not tie their destiny to a single flag. They purchase geographic optionality. Through citizenship-by-investment programs, an investor might hold a passport from Malta, keep their core capital in a Swiss trust, and operate a holding company registered in the Cayman Islands. (This tri-continental setup is actually standard practice among old-money European dynasties.) As a result: trying to pin down exactly how many people have over $30 million within a specific nation becomes a bureaucratic nightmare. Wealth migrates silently to wherever the regulatory climate is most hospitable, leaving national tax agencies perpetually guessing.

Frequently Asked Questions

Which cities house the highest concentration of individuals with over million?

New York City consistently claims the global crown, boasting a staggering population of over 17,000 UHNWIs navigating its financial districts. Tokyo and London follow closely behind, with Tokyo holding approximately 11,000 individuals within this elite bracket despite Japan's sluggish economic growth. The surprise contender is Singapore, which has seen its ultra-wealthy population surge by over 13% in recent years due to massive capital inflows from mainland China. Yet, the question of how many people have over $30 million in these urban hubs is shifting rapidly as tax-friendly states like Florida lure billionaires away from traditional northern strongholds.

How does inflation affect the total number of ultra-wealthy people globally?

Inflation acts as a bizarre double-edged sword for the global ultra-wealthy demographic. On one hand, persistent inflation devalues fiat currency, meaning a net worth of $30 million today buys significantly less than it did two decades ago. Conversely, because these individuals predominantly own hard assets like prime real estate, energy infrastructure, and corporate equities, their nominal net worth often skyrockets during inflationary periods. Consequently, the absolute number of nominal multi-millionaires increases artificially, even if their actual purchasing power has remained stagnant. This asset inflation explains why global wealth reports continue to show rising numbers of UHNWIs despite widespread economic anxiety among the middle class.

What percentage of these multi-millionaires inherited their wealth versus creating it?

The prevailing narrative suggests that the ultra-wealthy are merely riding on the coattails of ancestral trust funds. Modern data tells a radically different story, revealing that roughly 64% of individuals with fortunes exceeding $30 million are entirely self-made. Another 23% fall into a hybrid category, combining an initial inheritance with aggressive entrepreneurial expansion to multiply their family's baseline fortune. Only about 13% of the current global UHNWI population relies solely on purely inherited legacy wealth without actively managing or growing the enterprise. This data proves that modern ultra-wealth is overwhelmingly driven by technological disruption, venture capital success, and global market scale rather than mere dynastic inertia.

The Reality Behind the Numbers

Counting the world's multi-millionaires is ultimately an exercise in tracking moving targets across a borderless financial grid. We can obsess over the precise metrics, but the obsession misses the broader geopolitical point. The explosive growth of this elite tier signals a permanent divergence between the asset-owning class and the wage-dependent populace. It is no longer about hard work; it is about capital efficiency. True economic resilience belongs exclusively to those who own the infrastructure of global commerce. Unless systemic regulatory frameworks shift globally, this concentration of wealth will accelerate, leaving the rest of the world to watch the numbers climb from afar.