The Hidden Machinery of Death and Taxes: What Actually Happens to a Legacy

People often conflate different types of levies because the financial industry does a terrible job of explaining them to the average grieving family. When someone passes away, their estate becomes a temporary legal entity. This entity is responsible for settling debts and satisfying the federal estate tax, which only triggers at a staggering $13.61 million exemption threshold per individual as of recent tax updates. That changes everything for 99% of Americans. If the estate owes money, the executor pays it out of the collective pot before cutting check number one to you.

The Critical Distinction Between Estate Levies and Inheritance Levies

Here is where it gets tricky for the average person sitting at a kitchen table surrounded by legal documents. An estate tax is levied on the entire pile of money before distribution, whereas an inheritance tax is slapped directly onto the person receiving the cash. I find it absurd that we allow a system where geography dictates your financial destiny so aggressively, yet that is our current reality. You might inherit a pristine farmhouse in one state completely scot-free, while a cousin across the state border gets hammered by local revenue departments. It is a game of geographic roulette.

Why Inherited Money Shuns the Standard Income Tax Bracket

Because the IRS already taxed that money when the deceased earned it. Double taxation is generally frowned upon in this specific legal niche, meaning your inherited wealth will not bump you into a higher bracket on your next April filing. But wait—did the money come from a standard checking account or a tax-deferred retirement vehicle? That single detail alters the entire landscape.

The State-Level Traps That Wealth Advisors Don't Think About Enough

While Washington leaves your inheritance alone, a handful of state capitals are far more predatory. As of right now, six states still enforce a distinct inheritance tax that targets the recipient directly. If your benefactor lived in Pennsylvania, New Jersey, Maryland, Kentucky, Nebraska, or Iowa, you are looking at a completely different financial forecast. And honestly, it's unclear why these specific states cling so desperately to these archaic systems when neighboring regions have abandoned them entirely.

The Exemption Matrix and How Bloodlines Alter Your Bill

State inheritance taxes are obsessed with nepotism. If you are a surviving spouse, you are almost universally exempt from paying a single dime. Direct descendants—think children and grandchildren—usually receive massive exemptions or incredibly low rates, often hovering around 1% to 4.5% in places like Pennsylvania. But what if you were merely a close friend or a favorite nephew? The state views you as a Class C or Class D beneficiary, and that is where the hammer drops. Nebraska, for instance, has historically charged up to 15% on distant relatives or unrelated heirs. Is it fair that a biological child pays nothing while a lifelong foster child gets taxed to the hilt? Experts disagree on the morality, but the statute books remain unyielding.

The Double Whammy Facing Maryland Residents

Maryland enjoys the dubious honor of being the only jurisdiction in the nation that implements both an estate tax and an inheritance tax. If an estate valued at $6 million passes away there, the state treasury dips its hand into the jar twice. First, the estate itself pays a mechanism tax, and then the non-exempt beneficiaries pay another round on their individual slices. It is a fiscal meat grinder. Anyone planning a legacy in Annapolis needs to be looking at sophisticated trusts immediately or risk watching a quarter of their life's work vanish into state coffers.

Tax-Deferred Accounts: The Retirement Asset Time Bomb

Cash under a mattress or money in a traditional savings account transfers cleanly, but traditional retirement accounts are an entirely different beast. If you inherit a traditional IRA or a 401k, you did not just inherit money; you inherited a future tax bill. The deceased built that nest egg using pre-tax dollars, meaning Uncle Sam has been waiting patiently for decades to get his share.

The SECURE Act and the Sudden Death of the Stretch IRA

The rules changed violently with the passage of the SECURE Act. Previously, if you inherited a traditional IRA, you could stretch out the required minimum distributions over your entire natural lifespan, minimizing the annual tax hit. No longer. Now, non-spouse beneficiaries must completely empty that inherited retirement account within a strict 10-year window. Imagine inheriting a $500,000 IRA while you are in your peak earning years. Forcing that money into your personal income stream over a single decade can easily push you into the 32% or 35% federal tax bracket. It can absolutely decimate the real-world value of the inheritance.

The Radiant Exception of the Roth IRA Portfolio

Roth accounts are the holy grail of inherited wealth. Because the original owner already paid income taxes on the seed money, the distributions you take from an inherited Roth IRA are entirely tax-free. You still have to empty the account within that mandatory 10-year timeframe, but you can let the money compound aggressively until year nine, withdraw the entire balance in one massive lump sum, and pay exactly zero dollars to the IRS. It is the ultimate shield against post-mortem taxation.

Real Estate vs. Cash: The Miracle of the Step-Up in Basis

Suppose you don't receive cash at all, but rather a mid-century modern home in Los Angeles bought by your grandmother in 1974 for $45,000. Today, that property is worth $1.8 million. If she had sold it the day before she died, she would have faced a catastrophic capital gains tax bill. Because you inherited it, the tax code grants you a spectacular loophole known as the step-up in basis.

How a Date of Death Eraser Saves Thousands in Capital Gains

The IRS effectively erases fifty years of appreciation. Your new cost basis becomes the fair market value of the property on the exact date of your grandmother's passing—$1.8 million. If you turn around and sell the house a month later for that exact amount, your taxable profit is zero. You walk away with the full cash value without triggering capital gains. We are far from the days when heirs had to scrounge through ancient shoeboxes to find original purchase receipts, which explains why real estate remains one of the most resilient methods of transferring intergenerational wealth without enriching the government.

Common mistakes and dangerous misconceptions

The grand myth of the blanket tax exemption

You probably think a windfall from a deceased relative arrives completely pristine and untouched by the government. Except that reality is far more convoluted than late-night television legal dramas suggest. Everyone assumes that because the federal estate tax threshold hovers at a staggering $13.61 million per individual, they are entirely safe from the clutches of the taxman. It is a comforting thought. The problem is, this assumption conflates estate levies with inheritance levies, which are entirely separate beasts. While Uncle Sam might leave your lump sum alone, several local jurisdictions will happily chip away at your new wealth before the check even clears. If you inherit assets from a benefactor who resided in New Jersey or Pennsylvania, you might face a localized levy ranging anywhere from 1% to 16% depending on your exact familial relationship. Do beneficiaries pay taxes on inherited money? Yes, they absolutely do when state lawmakers decide to balance their budgets on the backs of grieving families.

Misunderstanding the step-up in basis trap

Let's be clear about investment portfolios and real estate. Many heirs believe the coveted step-up in basis wipes away every single penny of capital gains liability forever. It does not. If your late aunt bought stock for $10 and it was worth $100 on the day she passed, your new valuation benchmark becomes $100. But what happens if you lazily hold onto those shares for another six months while the market rallies, eventually selling them when the price hits $120? You owe Uncle Sam capital gains on that $20 bump. Neglecting to track the exact valuation fluctuation between the date of death and the actual date of liquidation constitutes a massive, costly blunder that sends panicked filers scrambling every single April.

The hidden plumbing of income in respect of a decedent

The ticking time bomb inside inherited retirement accounts

This is where standard financial planning advice frequently breaks down, leaving unsuspecting families exposed to aggressive IRS clawbacks. When you receive a traditional 401k or an Individual Retirement Account, you are not just inheriting cold cash; you are stepping into the tax shoes of the deceased. The IRS classifies this specific distribution as Income in Respect of a Decedent. Because the original account owner funded these vehicles with pre-tax dollars, someone eventually has to settle the bill. Under the strict rules governing modern estate distributions, most non-spouse heirs must completely empty these inherited retirement accounts within a rigid 10-year window. This forced liquidation can violently push your personal annual earnings into a much higher bracket. Imagine inheriting a $500,000 traditional IRA and being forced to pull out $50,000 annually while you are already at the peak of your earning career. The resulting fiscal hit can swallow nearly a third of the total windfall, which explains why wealthy families are aggressively pivoting toward Roth conversions before passing away.

Frequently Asked Questions

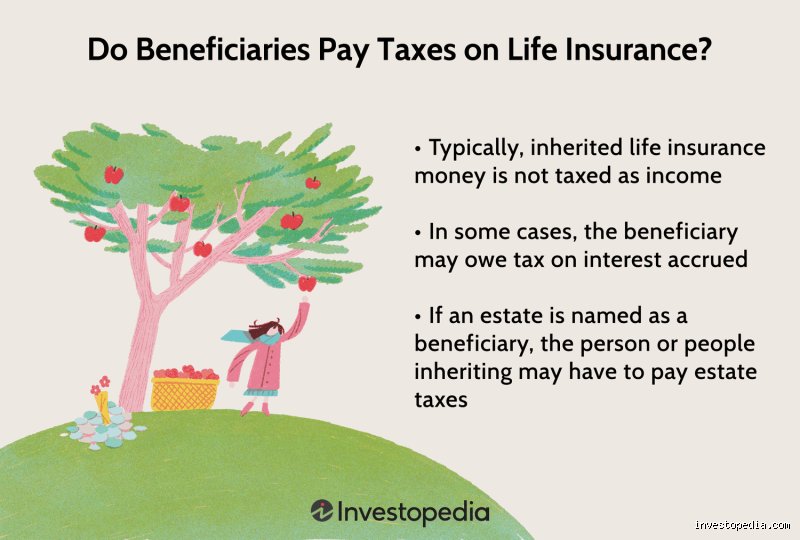

Do beneficiaries pay taxes on inherited money from life insurance policies?

Generally speaking, life insurance proceeds bypass the standard probate process and land in your bank account entirely free of federal income liability. This remains true whether the payout is $50,000 or a massive $5 million settlement. The issue remains, however, when the insurance payout experiences a prolonged delay and the underlying insurance company elects to pay out accumulation interest on the principal amount while the paperwork is being painstakingly processed. In that specific scenario, the baseline death benefit remains pristine, yet you must report that extra interest income on Form 1099-INT. Furthermore, if the policy owner made the critical mistake of naming their own estate as the beneficiary rather than an individual, the entire payout gets dragged back into the broader estate valuation pool, potentially triggering steep estate taxes at the state level.

Are foreign inheritances taxed by the internal revenue service?

The United States government does not directly levy an inheritance tax on international assets transferred from a non-U.S. citizen who lived abroad. But did you honestly think the government would let a massive influx of foreign wealth go completely unnoticed? If you receive a foreign windfall that exceeds a total valuation of $100,000 within a single calendar year, you are legally obligated to file Form 3520. Failing to submit this purely informational disclosure document carries an incredibly punitive penalty of 5% of the total inheritance value for each month the form is late, maxing out at a brutal 25% penalty. Therefore, while you technically will not owe direct income tax on that foreign wire transfer, your failure to report the transaction can result in the government seizing a massive portion of your newly acquired money through administrative fines.

How does inheriting a house affect your annual tax filing status?

Simply inheriting the physical keys to a residential property does not trigger an immediate income tax event for the lucky recipient. But property taxes do not magically pause because the owner passed away, meaning you instantly inherit the ongoing local property tax obligations as the new titleholder. If you decide to transform the property into a functioning rental, you must report every dime of rental income while simultaneously leveraging depreciation deductions to offset your liabilities. Should you choose to sell the residence immediately, you utilize the fair market value at the date of death as your baseline cost basis, effectively eliminating most capital gains liabilities unless the local real estate market skyrockets during the probate period.

A definitive strategy for the modern heir

Navigating the complex aftermath of a legacy transfer requires far more than mere gratitude and a trip to the local bank branch. We must stop pretending that receiving wealth is an entirely passive, risk-free endeavor in our current fiscal landscape. The modern tax code is explicitly engineered to capture leakage at every generational handoff. If you sit on your hands and blindly assume everything is exempt, you will eventually receive a very unpleasant, highly aggressive automated letter from the IRS. Waiting until next April to audit your inherited liabilities is a recipe for financial disaster. Take a proactive stance right now by ring-fencing your windfall until an independent professional verifies your exact local exposure. (Your future solvency will thank you for this momentary paranoia.) True wealth preservation is not about how much money lands in your lap; it is about having the strategic foresight to prevent the state from clawing it away.