Let's be completely honest for a moment: the marketing hype would have you believe these firms are benevolent architects of a utopian future. We are far from it. Silicon Valley loves a good narrative, but what we are actually witnessing is a brutal, high-stakes turf war over infrastructure, where proprietary data loops create monopolies that are almost impossible to disrupt. If you control the silicon wafers and the hyperscale data centers, you control the cognitive surplus of the twenty-first century. It is that simple, yet the implications are dizzying.

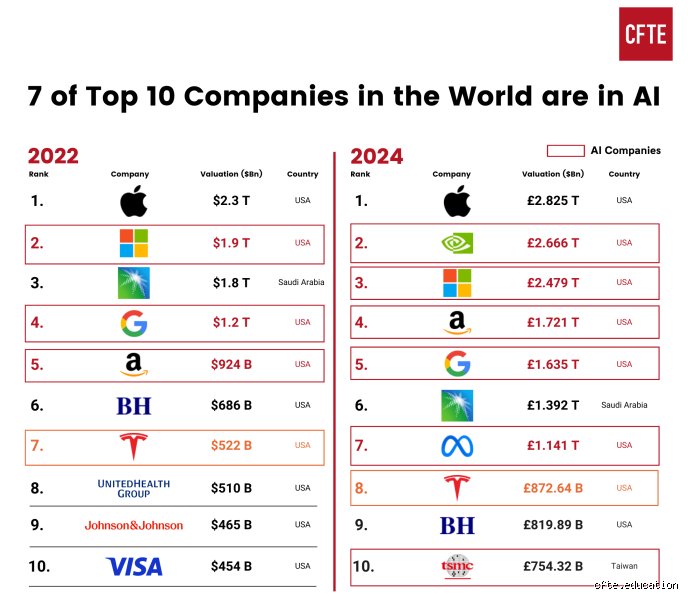

Beyond the stock market ticker: What does the term "7 AI companies" actually mean for global tech?

The transition from a mobile-first paradigm to an AI-native reality happened almost overnight, catching several legacy institutional players completely flat-footed. When Wall Street started grouping these specific entities together, it wasn't just because their stock charts looked identical. The thing is, these seven organizations possess something no startup can ever hope to replicate without billions in venture backing: unprecedented capital expenditure capacity to build foundational infrastructure. We are talking about custom undersea fiber-optic cables, dedicated nuclear power agreements, and proprietary silicon fabrication queues that stretch out for years.

The structural shift from consumer software to absolute cognitive monopoly

In the old days—if we can call 2018 the old days—tech companies made money by selling ads or renting cloud storage space by the gigabyte. But that changes everything when software begins to generate autonomous reasoning capabilities. The Seven are no longer mere platforms; they are rapidly becoming the systemic cognitive utility layer for global commerce. But who actually audits these systems when their internal neural weights are treated as closely guarded state secrets? Experts disagree on where corporate sovereignty ends and public interest begins, making this the defining legal quagmire of our generation.

Why data gravity and compute density create insurmountable barriers to entry

People don't think about this enough: AI models suffer from an insatiable hunger for both raw electricity and pristine, uncorrupted human data. This phenomenon, known in computer science as data gravity, means that the largest repository of information naturally attracts the most developers, which in turn generates even more telemetry data. Because Microsoft has Office, Alphabet has Search, and Meta has billions of social profiles, the flywheel spins faster for them than anyone else. The barriers to entry aren't just high; they are practically vertical.

The architectural engine room: How Microsoft, Alphabet, and Nvidia built the foundational stack

To truly grasp the mechanics of the 7 AI companies, we have to look closely at the foundational layer where the actual math happens. It is easy to obsess over shiny user interfaces, but the real power resides in the raw server racks. Nvidia transformed from a video game hardware vendor into a geopolitical kingmaker by locking down the market for graphic processing units. Their proprietary software ecosystem, CUDA, acts as a digital moat that prevents engineers from easily migrating their AI workloads to competing chips.

The semiconductor chokehold and the architectural dominance of CUDA

Have you ever wondered why every single tech giant behaves with absolute deference toward a single chip designer in Santa Clara? Because without Nvidia's H100 and Blackwell architectures, training a frontier model with over a trillion parameters becomes a mathematical impossibility within a reasonable timeframe. It's a terrifyingly narrow bottleneck. Microsoft and Alphabet understood this early, leading to an aggressive accumulation of hardware assets that resembles a digital arms race, reminiscent of the Cold War stockpile dynamics. Except that this time, the weapons are matrix multiplication clusters.

Hyperscalers and the proxy wars of venture capital funding

Where it gets tricky is the complex web of investments connecting these giants to ostensibly independent research labs. Microsoft's multi-billion-dollar alliance with OpenAI, cemented by massive cloud compute credits on the Azure platform, set a precedent that changed the industry forever. Alphabet responded in kind, deploying its massive balance sheet to secure a significant stake in Anthropic, the creators of the Claude models. These arrangements aren't standard venture capital deals; they are sophisticated compute-for-equity swaps designed to lock top-tier research talent into specific cloud ecosystems.

The sovereign data fortresses of Google DeepMind and Microsoft Research

And let's not overlook the sheer volume of intellectual property concentrated within Google DeepMind in London and Microsoft's global research hubs. These laboratories are publishing papers at a cadence that academic institutions simply cannot match, creating a massive brain drain from universities. The issue remains that when public research is privatized, society loses its ability to steer the direction of technological progress, leaving us entirely dependent on quarterly corporate earnings reports for scientific breakthroughs.

The consumer gateways: Meta, Apple, and Amazon deploying algorithmic models at scale

While the infrastructure players fight over liquid-cooled server racks, the consumer-facing tech titans are executing a completely different playbook centered around distribution. They don't necessarily need to win the race for raw artificial general intelligence; they just need to inject autonomous agents into the software you already use every single day. Meta chose a radically different path by open-sourcing its Llama models, a brilliant tactical maneuver that effectively commoditized the underlying software layer while keeping their massive social graph proprietary.

Open-source disruptive tactics versus walled-garden deployment strategies

Mark Zuckerberg's open-source strategy was a masterstroke of corporate judo that disrupted his rivals' subscription monetization models. By giving away the weights of high-performing models to independent developers globally, Meta decentralized the development cost while ensuring that the entire open-source community optimized their software to run efficiently on Meta's preferred architectures. Contrast this with Apple, which quietly integrated its own intelligence framework directly into the silicon of millions of consumer devices worldwide during its 2024 operating system rollouts, creating an impenetrable ecosystem edge. As a result: local on-device processing became a reality for the masses without sacrificing data privacy.

Retail logistics and the quiet automation of the AWS enterprise backbone

Amazon occupies a unique dual position within this elite septet. Through Amazon Web Services, they control over 31% of the global cloud infrastructure market, providing the compute backbone for thousands of enterprise AI applications. Simultaneously, their retail operations use predictive algorithms to orchestrate logistics across hundreds of fulfillment centers globally, optimizing supply chains before a consumer even clicks the purchase button. It is an industrial application of predictive mathematics that lacks the flashiness of a chatbot but possesses immense economic leverage.

The outliers and alternatives: Decoupling Tesla and evaluating the broader ecosystem

Then there is Tesla, the volatile wildcard of the 7 AI companies that defies traditional tech classification. Is it a car company, an energy grid coordinator, or an autonomous robotics laboratory? Elon Musk's enterprise treats vehicles as mobile, data-collecting edge devices, feeding millions of video hours into their Dojo supercomputing cluster in Austin, Texas to train their Full Self-Driving neural networks. It is a massive, real-world robotics experiment occurring right on public roads.

The physical embodiment of neural networks in robotics and autonomy

Tesla's strategy hinges on the belief that intelligence cannot be purely virtual; it must be embodied within a physical form factor to understand the chaotic reality of our world. Their development of the Optimus humanoid robot relies heavily on the exact same vision-based transformer models used in their automotive fleet. Yet, many traditional automotive analysts remain deeply skeptical of these valuations, arguing that solving vision-based autonomy is a far more distant goal than the company's marketing suggests. Honestly, it's unclear if their pure-vision approach can overcome edge-case anomalies without incorporating LiDAR sensor redundancy.

The rising counter-weights challenging the Silicon Valley hegemony

But are these seven companies truly invincible, or are we ignoring the geopolitical shifts happening across the Pacific? In Europe and Asia, alternative ecosystems are emerging, driven by different regulatory environments and sovereign national priorities. French startup Mistral AI proved that lean, highly optimized teams could build models that compete directly with Silicon Valley's heavyweights at a fraction of the training cost. Hence, the assumption that only American hyperscalers can survive this transition is fundamentally flawed, especially as energy constraints begin to level the playing field globally.

Common mistakes and misconceptions about the AI elite

The "Magnificent Seven" conflation

You cannot simply copy and paste the Wall Street stock index into a serious discussion about architectural artificial intelligence. Investors obsess over Nvidia, Microsoft, Alphabet, Meta, Apple, Amazon, and Tesla. But let's be clear: this financial grouping does not perfectly map onto the technical vanguard actually driving frontier model breakthroughs. Some of these titans rely heavily on partnerships rather than internal foundational research, which explains why assuming market cap equals cognitive supremacy is a mistake. The real answer to who are the 7 AI companies requires looking past the stock ticker to see who actually commands the raw compute and the researchers writing the core algorithms.

The illusion of static dominance

The leaderboard changes every Tuesday morning. People treat the current crop of infrastructure kings as if they have secured permanent monopolies, yet historical precedent suggests otherwise. The issue remains that building massive data centers with 100,000 liquid-cooled GPUs creates a moat, but algorithmic efficiency could shatter it overnight. A small lab optimizing sparse transformers might completely bypass the need for a sovereign power grid. Because of this architectural volatility, assuming the current dominant tech oligarchs will hold the crown forever ignores how fast software can adapt when hardware costs skyrocket.

The compute asymmetric war: an expert perspective

The hidden compute-sovereignty cartel

Forget the sleek user interfaces you play with on your phone. The real battle determining who are the top AI enterprises is fought in the energy sector and real estate development. The true power players are building a closed ecosystem where compute is the ultimate currency, trading processing time for equity in promising startups. This asymmetric warfare leaves traditional software companies stranded without infrastructure. If you want to identify the true rulers of this domain, ignore their marketing press releases and track their long-term nuclear energy purchase agreements and fiber-optic investments instead. (We are witnessing the industrialization of cognition, after all.)

Frequently Asked Questions

Is open-source software capable of destabilizing the current market leaders?

Open-source models have narrowed the capability gap drastically, yet they face a structural ceiling regarding capital-intensive training runs. Meta surprised the industry by spending an estimated $500 million on compute for Llama 3, proving that open weights require corporate patrons. True decentralized communities cannot easily crowdsource the massive cluster coordination needed for trillion-parameter systems. As a result: open-source operates as a highly disruptive follower rather than the absolute bleeding edge of frontier discovery. The problem is that while fine-tuning is cheap, training from scratch remains a billionaire's sport.

How much electricity do these frontier models actually consume during training?

The scale of energy consumption is moving from localized server strain to national grid anxieties. Frontier clusters now require dedicated power installations, with a single advanced cluster consuming up to 150 megawatts of electricity during a multi-month training cycle. This footprint equals the energy usage of small cities. Tech firms are actively buying up nuclear power capacity to ensure uninterrupted operations. Except that public infrastructure was never designed to handle localized computational demands of this magnitude without causing regional blackouts.

Will synthetic data solve the impending human content exhaustion crisis?

The internet is running out of high-quality human text, forcing developers to feed models data generated by other algorithms. This approach creates a massive risk of model collapse, where subtle errors compound until the output degrades into complete gibberish. Advanced labs are circumventing this by using reinforcement learning loops where models critique each other, which works well for mathematics and coding but fails for nuanced cultural understanding. Will we eventually find ourselves locked in an echo chamber of machine-authored culture? The absolute limit of synthetic training data remains one of the most guarded secrets in the entire tech industry.

A definitive stance on the future of cognitive monopolies

We are drifting toward an unprecedented era of centralized intellectual infrastructure controlled by an incredibly narrow oligopoly. The romantic notion of a brilliant garage startup completely upending the entire paradigm without massive institutional backing is dead. This transition means society will soon rent its fundamental reasoning capabilities from a handful of corporate gatekeepers. We must stop evaluating these entities merely as software vendors or high-performing stocks on an index. They are building the foundational cognitive utilities of the twenty-first century, and their decisions will govern human productivity for generations. Do you honestly believe a democratic society can function smoothly when its collective intelligence is private intellectual property?