The Hidden Architecture of Global Trade and Why We Get It Wrong

Most people look at international commerce and think of container ships stacked with cheap plastic toys or maybe bushels of wheat. But that changes everything when you actually audit the customs manifests because the macro-economy doesn't care about consumer trinkets; it cares about systemic reliance. The issue remains that we tend to view trade through a nostalgic, 20th-century lens of raw commodities, yet the modern landscape is fiercely technocentric. Where it gets tricky is drawing a line between what countries produce and what they actually monetize effectively on the open sea.

The Statistical Heavyweights of the Customs Ledger

If you aggregated every Harmonized System code recorded by customs agencies from Rotterdam to Singapore, a stark reality emerges. It turns out that a staggering 18% of all global trade value resides in just three highly specialized categories. This isn't a fluke. Because industrialized nations require massive energy inputs, complex computational power, and physical mobility, these sectors have become entirely non-negotiable. Analysts at the World Trade Organization noted that despite massive geopolitical friction in recent years, the absolute volume of these top-tier exports grew by 4.2% annually between 2021 and 2025.

Why Raw Materials Lose the Export Crowns

But wait, why isn't iron ore or crude oil occupying all three top spots? The thing is, unrefined goods possess massive volume but suffer from volatile, unforgiving price cycles. Refinement adds the margin. A barrel of crude is fine, but the real money—and the massive export valuation—lies in the ultra-low sulfur diesel and aviation fuel flowing out of hyper-complex mega-refineries. I firmly believe that nations clinging to purely extractive export models are essentially leasing their sovereignty to the states that actually process those goods. It is the value-added transformation that turns a basic resource into an economic superpower.

Hydrocarbons Transformed: Refined Petroleum and the Energy Paradox

Let's talk about the undisputed king of the shipping lanes. Even as talk of green transitions dominates boardroom presentations in Davos, refined petroleum products remain the lifeblood of global logistics, pulling in over $1.2 trillion in export value during the last fiscal cycle alone. Honestly, it's unclear when this dominance will truly wane—experts disagree wildly on the peak-demand timeline—but for now, the world runs on processed carbon. And the scale is mind-boggling.

The Geopolitical Shift in Refining Superpowers

Historically, the West refined what it consumed. Not anymore. Today, massive processing complexes like the Reliance Industries Jamnagar refinery in India—which churns out over 1.2 million barrels per day—have fundamentally rewritten the trade maps. India has become a net exporter of clean fuels to Europe, creating an ironic detour where Western nations buy processed oil from Asian hubs that originally sourced the crude from sanctioned territories. It is a dizzying shell game. As a result: traditional trade routes have stretched, driving up maritime insurance rates and making the physical transport of this specific export more lucrative than ever before.

The Margin Game: Crude Versus Distillates

People don't think about this enough, but a country like South Korea possesses virtually zero domestic oil reserves, yet regularly ranks as a global powerhouse in petroleum exports. How? By mastering the crack spread—the differential between the price of crude and the extracted refined products. Their state-of-the-art facilities in Ulsan slice and dice heavy sour crudes into high-value petrochemical bases and marine fuels. It is a high-stakes, low-margin game where a variance of just a few cents per gallon can mean the difference between a national trade surplus or a fiscal crisis.

The Silicon Imperative: Integrated Circuits as the New Currency

If petroleum is the muscle of the global economy, microchips are the central nervous system. Officially classified as electronic integrated circuits, these tiny slabs of silicon represent the single most complex manufactured goods in human history, commanding an export market worth $1.15 trillion. You cannot build a toaster, a ballistic missile, or a medical ventilator without triggering a transaction that routes through a handful of ultra-specialized facilities. It is a bottleneck of terrifying proportions.

The Monopolistic Anatomy of the Semiconductor Supply Chain

This is where the geography of what are the three main exports becomes incredibly concentrated. Taiwan alone controls over 60% of the total semiconductor market and a staggering 90% of advanced processor manufacturing, primarily through TSMC. Imagine if a single island produced nearly all the world's paper currency; that is the reality of silicon trade today. But the plot thickens when you realize they import the raw silicon wafers from Japan, utilize lithography machines manufactured exclusively by ASML in the Netherlands, and design the architecture in California. It is a hyper-globalized dance where a single misstep or a localized earthquake ripples across the globe instantly.

The Price per Gram Explosion

Consider an unexpected comparison: a kilogram of refined petroleum costs pennies, while a kilogram of high-end 3-nanometer microchips is worth significantly more than its weight in pure gold. This extreme value density alters how the product moves. While oil sluggishly traverses oceans in mammoth tankers, microchips fly in the cargo holds of commercial airliners, wrapped in anti-static film and guarded like crown jewels. Hence, when air freight capacity collapsed during recent global disruptions, the semiconductor export metrics plummeted, starving automotive factories thousands of miles away and proving just how fragile this digital infrastructure really is.

Wheels of Commerce: The Resilient Empire of Passenger Vehicles

The third pillar holding up the global trade triad is the automotive sector. Specifically, passenger vehicles accounted for roughly $830 billion in international trade last year. Unlike microchips, cars are massive, heavy, and logistically nightmarish to move across continents, yet the global demand for specific brand prestige and engineering excellence keeps the Ro-Ro (Roll-on/Roll-off) vessels completely packed. It is an industry in the throes of a violent mutation.

The Electric Disruption and the Rise of New Giants

For decades, the automotive export hierarchy was a predictable, somewhat stuffy club dominated by Germany, Japan, and Detroit. Except that the sudden, aggressive pivot to electric powertrains completely shattered those legacy legacy structures. Look at China: in less than a decade, they went from an automotive import-dependent market to overtaking Japan as the world's largest vehicle exporter, shipping over 5.2 million vehicles in 2024 alone. This wasn't achieved by beating western firms at the traditional internal combustion engine game, but by monopolizing the lithium-iron-phosphate battery supply chain internally, allowing them to underprice European competitors by up to 30% in open markets.

Trade Barriers and the Globalization Backlash

But the expansion of car exports isn't happening in a vacuum. Because automotive manufacturing is historically tied to national pride and massive domestic employment, the surge of foreign vehicles has triggered a wave of aggressive protectionism. We are seeing tariff walls rising across the Atlantic—tariffs that mock the very idea of a free global market. This friction forces manufacturers to pivot from exporting completely built-up units to shipping "knock-down kits" for local assembly, blurring the lines of what constitutes a pure export and showing how politics can forcefully bend economic realities.

Common mistakes and dangerous misconceptions

The trap of the static snapshot

Most trade analysts stare at trade sheets like they are looking at a fixed monument. The problem is that global trade flows behave more like mercury. If you ask a room of novice macroeconomists what are the three main exports of any given developing nation, they will likely recite data from five years ago without blinking. Except that supply chains mutate overnight when regional conflicts or sudden tariff updates disrupt the old order. Relying on outdated annual reports is the fastest way to miscalculate market penetration and lose capital.

Confusing gross value with domestic value added

Let's be clear: a country might ship billions of dollars in high-tech smartphones, but if it merely screws together imported microchips and screens, the economic reality is completely different. We often conflate massive top-line export numbers with genuine national wealth creation. A nation might boast that its top outbound shipments are luxury automobiles, yet ninety percent of the components cross three borders before final assembly. This statistical illusion masks the true vulnerability of a nation's manufacturing core and tricks policymakers into false confidence.

The diversification myth

Are more categories always safer? Not necessarily. Politicians love to scream about expanding their trade portfolios, yet they ignore the structural realities of resource-dependent economies. When a state attempts to forcibly pivot away from its historical strengths, it often wastes billions on artificial industries that cannot compete on the global stage. What are the primary export items of a country? They are the products of decades of infrastructure development, not something you can change with a simple legislative decree.

Unlocking the hidden leverage: The intermediate goods trap

Why the hidden components rule the world

Everyone focuses on the shiny finished products that load into container ships. But you need to look closer at the invisible plumbing of international commerce. The real power in contemporary trade belongs to the nations that control specialized intermediate goods, like specialized chemical catalysts or precision industrial valves. If you control the unglamorous component that every single factory requires, you possess far more geopolitical leverage than the country assembling the final consumer gadget.

Because who actually holds the cards when a crisis hits? It is never the entity holding the final, easily replaceable retail commodity. It is the hyper-specialized monopoly provider. The issue remains that these vital components are frequently buried deep inside the broader trade data, hidden under generic industrial classifications. If we fail to map these micro-dependencies, we remain blind to the true choke points of the global economy.

Frequently Asked Questions

Which industrial sectors currently dominate global outbound trade volumes?

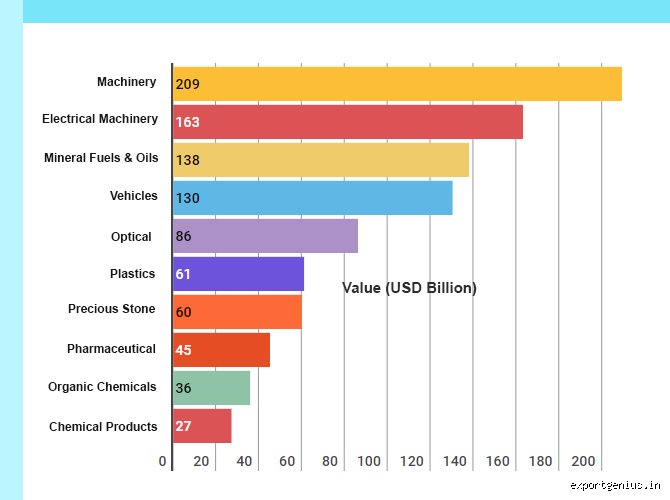

Machinery and transport equipment consistently command the highest share of international trade values, hovering around thirty-eight percent of total global shipments according to recent enterprise trade logs. This massive category is immediately followed by mineral fuels and lubricants, which fluctuate wildly based on crude pricing but routinely capture roughly fifteen percent of cross-border value. Chemical products and manufactured materials round out the dominant trio, capturing a combined twenty-two percent market share. Smaller categories like agricultural goods and textiles struggle to compete with these heavy industrial sectors in terms of pure financial footprint. As a result: the nations dominating these specific segments wield immense macroeconomic influence over international supply networks.

How do fluctuating currency values impact what are the three main exports of a nation?

When a domestic currency depreciates significantly against the US dollar, local outbound goods become instantly cheaper for international buyers, which explains why volume spikes frequently follow sharp devaluations. However, if those primary outbound goods rely heavily on imported raw components, the profit margins evaporate instantly. This creates a volatile feedback loop where raw material costs cancel out any competitive pricing advantages gained on the open market. Did you think a weaker currency was a magical shortcut to trade dominance? In short, currency volatility reshapes the profitability of shipments far faster than factories can adjust their production lines.

Can a nation successfully alter its primary outbound commodities within a single decade?

Radical economic pivots are exceptionally rare but entirely possible with aggressive, state-directed industrial policy, as demonstrated by South Korea's historical leap from textiles to semiconductors. Modern transformations require sustained capital investments exceeding twelve percent of annual gross domestic product over consecutive years to build the necessary infrastructure. Most modern states fail this transition because political cycles interrupt the long-term funding required to scale up advanced industrial complexes. Consequently, the vast majority of nations find their top shipment categories locked in place for thirty to fifty years. (Though a sudden discovery of lithium or rare earth elements can rewrite a nation's trade profile almost overnight).

An honest reckoning on trade dependencies

Stop looking at trade data as a scorecard where the biggest exporter wins the game. The obsessive quest to determine what are the three main exports of our trading partners misses the entire point of modern economic warfare. Vulnerability matters infinitely more than volume. We must acknowledge that true economic resilience does not come from selling massive quantities of easily substituted goods to a single dominant neighbor. It is time to champion aggressive supply chain independence, even if it means sacrificing short-term corporate profits for long-term national security. We can no longer afford to let naive free-market theories blind us to the dangerous dependencies that threaten our economic survival.