The Legal Maze: Why Would Someone Have a K1 Visa for a Fiancé?

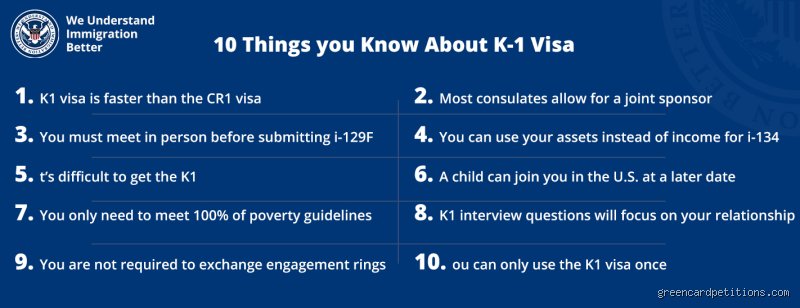

Let's look at the romantic—yet aggressively bureaucratic—side of this acronym. The U.S. Department of State issued 26,184 K-1 visas in fiscal year 2023, a massive rebound from the travel freezes of the pandemic era. Why do people choose this route? It exists for one specific purpose: allowing a foreign citizen to enter the United States to marry their U.S. citizen petitioner within a strict, non-negotiable 90-day window.

The Fast Track That Insiders Know Isn't Actually That Fast

People don't think about this enough, but the K-1 visa is a psychological roller coaster. Take Sarah Miller and her partner Alejandro, who moved from Bogotá to Miami in June 2024; they chose the K-1 assuming it was the absolute quickest way to reunite. Yet, with current I-129F petition processing times at the California Service Center hovering around 6 to 10 months, that changes everything. Is it a shortcut? Hardly. It merely shifts the waiting period from outside the U.S. borders to inside them, forcing the foreign spouse to wait months for an Employment Authorization Document before they can legally earn a single dollar.

The Freedom to Plan an American Wedding

But the issue remains that some couples simply refuse to marry abroad. Because of local laws in places like Germany or Indonesia—where getting hitched as a foreigner involves mountains of certified translations—bringing the partner to a local courthouse in Ohio seems vastly simpler. Except that it isn't, given the sheer volume of financial data required for the Form I-864 Affidavit of Support. But if your dream involves a wedding cake on American soil before the legal knot is tied, the K-1 remains the undisputed, legally sanctioned vehicle.

The Financial Puzzle: Why Would Someone Have a K1 Tax Form?

Now, let’s pivot sharply away from romance to the cold, hard world of pass-through taxation. If an accountant hands you a Schedule K-1 (Form 1065 or Form 1120-S), it means you have a stake in an entity that does not pay its own income taxes directly to Uncle Sam. Instead, profits, losses, deductions, and credits pass right through the business entity straight to you, the individual investor.

The Reality of the Passive Investor

The thing is, millions of everyday Americans hold these forms without ever stepping foot in a corporate boardroom. Have you ever bought shares in a publicly traded partnership, perhaps an oil and gas master limited partnership like Enterprise Products Partners? If you did, come March, you will receive a K-1. Honestly, it's unclear why the IRS insists on making these forms so structurally opaque, but if you own even 0.01% of a real estate syndicate that bought an apartment complex in Phoenix back in 2022, you are legally hitched to this document.

The S Corporation and the Small Business Hustle

Where it gets tricky is for the hands-on entrepreneur. If you and two buddies started a boutique marketing agency in Austin, registering it as an S Corp to avoid double taxation, you must file a Form 1120-S. Consequently, the business generates a Schedule K-1 for each of you by March 15. This form details your specific share of the ordinary business income. And that income must be reported on your personal Form 1040, specifically on Schedule E, regardless of whether the business actually distributed that cash to your personal bank account or kept it to buy new camera gear.

Tax Implications: What Happens When That Schedule K-1 Lands on Your Desk?

Receiving this form changes your entire tax filing timeline, usually for the worse. Most taxpayers expect to file by April 15 and call it a day, but K-1 forms are notorious for arriving late, sometimes creeping into mailboxes in late September.

The Inevitability of the Tax Extension

We are far from the days of simple W-2 filing when this form enters the mix. Because partnerships have until March 15—or September 15 if they request an extension—to distribute these forms, individual investors are frequently forced to file a Form 4868 to extend their personal filing deadline. I highly recommend expecting this delay. It is a standard rite of passage for anyone dipping their toes into private equity or hedge funds. Experts disagree on whether pass-through entities are truly more efficient than traditional C Corporations under current tax brackets, but the administrative headache is undeniable.

The Phantom Income Trap

Here is a scenario that catches people off guard: you are allocated $25,000 in taxable income on line 1 of your S Corp K-1, yet the company chose to reinvest all its profit into a new warehouse. You owe taxes on money you never saw. As a result: your personal cash flow takes a direct hit to pay for corporate growth. This dynamic is a frequent source of litigation among minority shareholders in closely held businesses who suddenly find themselves writing massive checks to the IRS without the distributions to back them up.

Choosing the Path: K-1 Visa Versus the CR-1 Marriage Visa

Returning to the immigration side of the coin, couples often agonize over whether to pursue the K-1 fiancé visa or get married abroad first and file for a CR-1 Spousal Visa. The decision is rarely clear-cut.

The True Cost of Adjustment of Status

While the K-1 gets your partner to the United States faster than a spousal visa, it carries a hidden financial sting. Once the 90 days are up and the vows are exchanged, you must file Form I-485 to adjust their status to a permanent resident. The filing fees alone represent a significant chunk of change, currently sitting at $1,440 for most applicants since the April 2024 fee hikes. Compare that to the CR-1 visa process, where the spouse enters the country as an automatic green card holder, bypassing this secondary mountain of paperwork entirely.

The Freedom to Work and Travel

Consider the lifestyle constraints. A CR-1 immigrant can immediately apply for a Social Security number and start working the week they arrive in Chicago or Seattle. On the flip side, a K-1 holder sits in a state of legal limbo for months, unable to drive in many states, unable to work, and unable to leave the country without risking the abandonment of their application. Yet, if a couple is separated by a war zone, a sudden job loss, or restrictive local marriage laws overseas, the swift entry provided by the K-1 outweighs every single one of these logistical nightmares.

Common mistakes and widespread misconceptions

The phantom double taxation trap

You rip open the envelope, glimpse the numbers on your Schedule K-1, and instantly panic because you assume Uncle Sam intends to tax this entire sum twice. The problem is, many passive investors do not realize that partnerships function as flow-through entities. You are not paying a second layer of corporate tax. Think of it as a direct pipeline where profits slide straight onto your personal Form 1040. Because the entity itself evades entity-level income tax, the numbers represent your proportional slice of what has already transpired under the hood. Yet, beginners frequently misreport these figures by duplicating them on Schedule E alongside standard rental income, triggering immediate, automated IRS flags.

Confusing actual cash distributions with taxable allocations

Let's be clear: paper wealth does not equal liquid cash in your checking account. You might get allocated a hefty $45,000 share of ordinary business income on paper while receiving exactly zero dollars in actual physical payouts. Why does this disconnect happen? Well, the general partners might decide to hoard that cash to purchase new equipment or pay down outstanding real estate debt. You owe tax on that phantom income regardless of your empty pockets. Conversely, receiving a physical check does not mean you have incurred an immediate tax liability; it might just be a non-taxable return of capital reducing your tax basis. If you confuse these two concepts, your cash flow projections will suffer a catastrophic collision with reality.

Advanced tactical maneuvers and expert insights

The hidden weapon of basis tracking

Can you guess what the single biggest audit trigger is for unsuspecting partners? It is deducting losses that exceed your actual economic risk. Tracking your inside and outside basis is entirely your responsibility, except that the partnership rarely computes this tedious calculation for you. When a syndication experiences a massive depreciation write-off, you can only use that loss to offset other passive gains if your basis remains comfortably above zero. But what happens if your outside basis drops to negative territory? The IRS will retroactively disallow those juicy deductions, slap you with a 20% accuracy-related penalty, and send an unwelcome bill. Smart operators maintain an independent, multi-year spreadsheet tracking every single contribution and distribution because relying solely on the promoter to protect your financial blind spots is an absolute fool's errand.

Frequently Asked Questions

Does receiving a K-1 automatically delay your annual tax filing?

Yes, preparing a complex tax return before late spring becomes nearly impossible when you hold these specific investments. While standard corporate forms arrive in late January, complex partnerships frequently push their reporting deadlines to March 15 or utilize automatic extensions that drag out until September 15. Real estate syndications require months to calculate cross-state allocations and finalize depreciation schedules, which explains why individual investors are routinely forced to file Form 4868 for an extension. Statistically, roughly 65% of multi-state partnership investors fail to file their personal returns by the traditional April deadline. Consequently, you must budget extra funds for your CPA to handle the multi-stage filing process and accept that your financial life will remain in limbo for months.

Can international investors hold these assets without massive complications?

Foreign nationals can certainly purchase stakes in domestic ventures, but the administrative burden escalates dramatically. The core issue remains that non-resident aliens face strict withholding rules under Section 1446, forcing the managing partnership to withhold a flat 37% of effectively connected income for foreign individuals. This mechanism ensures the government collects its due before the capital leaves domestic soil, meaning international partners rarely escape the American tax net. Furthermore, foreign investors must secure an Individual Taxpayer Identification Number and file a non-resident US tax return solely to claim their withholding credits. As a result: international capital face complex regulatory friction that routinely erodes the net yield of the underlying investment.

How does a Schedule K-1 impact your ability to qualify for a traditional mortgage?

Underwriters view fluctuating business income with extreme suspicion and will dissect your personal liquidity with a microscope. Traditional lenders look at your standard wages to establish stability, whereas partnership income requires them to analyze two full years of historical entity filings to calculate a dependable average. If your document shows large paper losses due to accelerated depreciation, the lender's automated underwriting software might erroneously conclude that your income is insufficient, even if your bank account is overflowing with cash. You will generally need to provide the complete partnership agreement alongside your individual schedules to prove you possess sufficient capital control. In short, your mortgage approval process will inevitably morph into a grueling, paper-heavy interrogation.

A definitive verdict on flow-through complexity

We need to stop pretending that alternative investments are a friction-free pathway to wealth. The logistical nightmare of dealing with fragmented tax documents represents the literal price of admission for superior asset classes. If you desire the outsized returns of private equity or the tax-shielding benefits of commercial real estate, you cannot simultaneously demand the simplistic elegance of a single traditional document. The administrative headache is not a flaw in the system; it is the exact mechanism that enables sophisticated tax avoidance. True financial sophistication requires you to embrace this complexity, pay the premium for an elite accountant, and aggressively pursue the structural advantages that ordinary W-2 employees will never access.