The anatomy of a pharmaceutical giant losing its crown

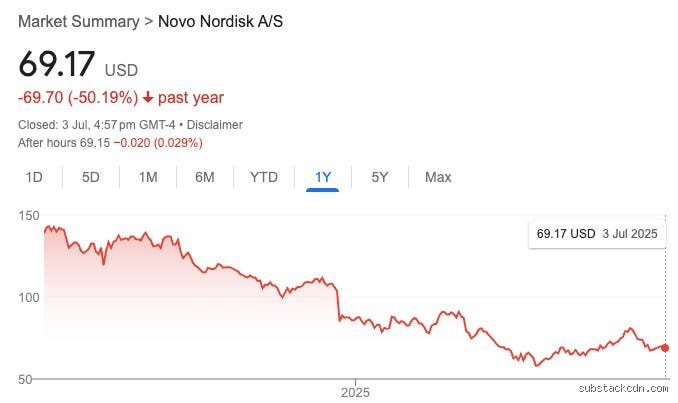

Not long ago, Novo Nordisk was comfortably sitting as the most valuable company in Europe, a crown jewel fueled by an insatiable global obsession with its blockbuster GLP-1 treatments. The thing is, markets are notoriously unforgiving when a hyper-growth story encounters a brick wall. Over the past year, shares have plummeted roughly 46% from their 52-week high of $81.44, leaving retail portfolios and institutional funds looking for answers. It gets worse.

The sentiment completely decoupled from reality. Investors treated obesity management as an infinite money printing machine, ignoring the basic laws of pharmaceutical lifecycles. When the company dropped its financial guidance for 2026, the market panicked. Adjusted metrics—which exclude a massive, one-off $4.2 billion reversal of U.S. 340B rebates—revealed that core revenue and operating profit are projected to drop by 5% to 13% at constant exchange rates. That changes everything. People don't think about this enough: a company trading at nosebleed earnings multiples cannot afford a flat year, let alone an outright contraction. The institutional exodus was instant, wiping out hundreds of billions in market value as the stock bottomed out near $40.52 in late March.

How the market miscalculated the GLP-1 hype cycle

Wall Street modeled the adoption curves of Ozempic and Wegovy as if they were software-as-a-service products rather than heavily regulated, politically sensitive biological therapeutics. They forgot that weight-loss drugs are subject to the same gravity as every other molecule. The immense demand caused widespread shortages, which accidentally created a thriving shadow market of compounded alternatives that chipped away at market share. Yet, the true destruction came from the realization that price realization per patient was falling off a cliff.

The pricing war and political headwinds squeezing margins

Where it gets tricky is the United States market, a goldmine that historically subsidized lower drug prices across Europe. The gravy train has derailed. In November 2025, Novo Nordisk was forced into an aggressive pricing agreement with the White House under the looming threat of sweeping import tariffs. This backroom deal severely reduced the list prices of Ozempic and Wegovy. And because the administration wielded its Most Favored Nation pricing framework like a sledgehammer, Novo's long-term margin profile was structurally broken.

The legislative pain did not stop there. The company is simultaneously locked in a desperate, uphill legal battle against the inclusion of semaglutide in the Inflation Reduction Act Medicare price negotiations. To expand insurance coverage and maintain volume, management effectively conceded defeat, planning to voluntarily slash Wegovy and Ozempic list prices by up to 50% starting in January 2027. Will volume save them? I have my doubts, and honestly, it's unclear if the broader market appreciates the sheer scale of the margin compression heading this way. The company's historic 2025 revenue of DKK 309 billion is expected to shrink to DKK 292 billion for the full year of 2026, a bitter pill for bulls to swallow.

International patent expirations create a multi-front war

While Washington squeezes margins domestically, international borders offer no sanctuary. Semaglutide is losing exclusivity at an alarming rate. Patent protections are actively expiring or being aggressively challenged in massive growth corridors like Brazil, Canada, and China. Local generic manufacturers are already hovering. This means that just as Novo Nordisk needs international volume to offset lower U.S. prices, cheaper regional copies will flood the market.

The REDEFINE 4 catastrophe and the pipeline problem

Every pharmaceutical downturn has its defining catalyst, a single moment where the narrative permanently fractures. For Novo Nordisk, that day was February 23, 2026. The stock plunged over 16% in a single trading session following the unblinding of the Phase 3 REDEFINE 4 clinical trial. The study was supposed to prove that CagriSema—a highly anticipated combination of semaglutide and cagrilintide—was the ultimate weapon to defend its obesity fortress. Except that it didn't.

The drug failed to demonstrate non-inferiority against its arch-rival's dominant therapy. It did not hit the projected 25% mean weight loss that analysts had already baked into their financial models. Goldman Sachs promptly slashed peak sales estimates for the combination by a staggering 65%, downgrading the stock to neutral. Is the pipeline broken? Not entirely, but it has certainly become a "show-me" story. The setback leaves Novo dangerously exposed to a single molecule, semaglutide, at a time when that exact molecule is under intense regulatory and competitive fire.

The manufacturing bottleneck and R&D cash burn

To compound the pipeline disappointment, capital expenditure is soaring. Novo Nordisk is pouring billions into building out manufacturing facilities to address past shortages and scale up its newly approved oral Wegovy pill. This creates a painful financial paradox: operating margins are compressing due to price cuts, while capital intensity is reaching historic highs. The cash burn required to stay competitive is eating into the free cash flow that previously supported aggressive stock buybacks.

Eli Lilly and the shifting duopoly dynamics

We cannot discuss Novo's fall without looking across the Atlantic at Eli Lilly. The duopoly that once controlled the metabolic space has tilted heavily in one direction. Lilly's tirzepatide brands, Zepbound and Mounjaro, have systematically outpaced Wegovy and Ozempic in both clinical efficacy and weekly prescription growth rates, allowing Lilly to become the first trillion-dollar healthcare giant while Novo slid down the rankings.

But the issue remains that the market is treating this as a zero-sum game where Novo loses everything. That is a mistake. Nuance matters here, and the conventional wisdom that Novo is structurally dead ignores their massive first-mover advantage in oral delivery systems. Their oral Wegovy pill achieved an impressive 170,000 patients within its first month in the U.S., with early data showing that 80% of those users were completely new to GLP-1 therapies. Hence, the market expansion is real, but Novo is being forced to transition from a high-price luxury monopoly to a high-volume, low-margin utility provider. We are far from the days of easy triple-digit gains. As a result: the stock is no longer a momentum darling, but rather a deeply complex value reset that will take years to play out.

Common misconceptions about the sudden slide

Retail investors look at the charts and panic, assuming the weight-loss gold rush has collapsed. The problem is they mistake a necessary valuation correction for a structural demise. Everyone assumed that Eli Lilly and Novo Nordisk would permanently split a bilateral monopoly without friction. Market saturation arrived faster than expected because manufacturing bottlenecks finally eased. But that is only half the story.

The trap of the weight-loss bubble narrative

Why is Novo Nordisk crashing? Media pundits scream that the anti-obesity craze was a transient fad. This is pure nonsense. The correction is not driven by a sudden national desire to stop using Wegovy. Instead, it stems from unrealistic initial valuations. When a stock trades at an astronomical price-to-earnings multiple, perfection is already priced in. Any minor hiccup, such as a slight discount in insurance reimbursement rates, triggers an avalanche. Yet, novice traders continue to dump shares because they confuse a falling stock price with a failing business model.

Misunderstanding the pricing pressure dynamics

Another fallacy involves global distribution. People see high demand and assume profits must scale linearly. Except that the American healthcare system is a labyrinth of pharmacy benefit managers demanding massive rebates. Novo Nordisk had to slash its net price for Wegovy in the United States by over 35% since launch to maintain preferred formulary placement. Copycat compounded semaglutide formulas also flooded online telehealth platforms, chipping away at market share. As a result: the top-line revenue growth looks spectacular while the net margins suffer a quiet, painful squeeze.

The hidden catalyst: Oral peptide vulnerability

While the public obsesses over weekly injections, institutional analysts are staring at a completely different scoreboard. The real threat to the Danish pharmaceutical giant is the brutal reality of oral bioavailability.

The metabolic tax of pill-based formulations

We all want a magic weight-loss pill. Novo Nordisk poured billions into developing an oral version of amycretin and high-dose semaglutide. But let's be clear: getting a fragile peptide past human stomach acid requires a monstrous amount of active pharmaceutical ingredient. It takes roughly 20 times more raw material to produce one oral dose than a single injection. When supply chains are already strained to their absolute limits, dedicating precious manufacturing capacity to an inefficient pill is an operational nightmare. (Amgen and Viking Therapeutics are meanwhile developing nimbler, small-molecule alternatives that bypass this exact roadblock).

Frequently Asked Questions

Is the current drop in Novo Nordisk shares a permanent trend?

Absolutely not, because this volatility reflects a classic sector rotation rather than an existential crisis. Institutional funds are merely harvesting profits after a staggering 400% run-up over four years to reallocate capital into depressed tech or energy sectors. The company still controls roughly 43% of the global GLP-1 market, maintaining a massive cash cushion. Did anyone actually believe a trillion-dollar valuation could be sustained without a single quarterly contraction? The issue remains that retail sentiment fluctuates wildly, while the underlying clinical pipeline for cardiovascular and NASH indications remains incredibly robust.

How much market share is Novo Nordisk losing to Eli Lilly?

The competitive landscape shifted dramatically when Zepbound secured broad regulatory approval and demonstrated slightly higher average weight loss percentages in clinical trials. Consequently, Novo Nordisk surrendered approximately 6% of its dominant market share in the premium obesity segment over the last twelve months. This fierce rivalry forced both titans into an aggressive price war that eroded the premium valuation multiples investors grew accustomed to. Which explains why the stock experienced a sharp, sudden repricing even as total sales volume hit record highs.

Will generic competition make Wegovy irrelevant anytime soon?

The core patents protecting semaglutide do not expire in major Western markets until the early 2030s. However, the immediate danger stems from the regulatory loopholes allowing compounding pharmacies to manufacture custom batches during official drug shortages. Tens of thousands of patients migrated to these cheaper alternatives, costing the company an estimated 1.2 billion dollars in lost revenue this year alone. Because the FDA will eventually remove semaglutide from the official shortage list, this specific revenue drain is temporary. But the reputational damage and the normalization of off-brand alternatives will linger for years.

A definitive verdict on the Danish giant

Stop looking at the daily ticker symbols expecting a linear trajectory to the moon. What we are witnessing is not the death of an empire, but the violent maturation of an entire therapeutic class. It is highly ironic that a company is suffering a market rout precisely when it is producing more life-saving medication than at any other point in human history. We must admit that the era of effortless, triple-digit annual gains for this specific equity is officially over. Do you buy the panic, or do you recognize a generational buying opportunity disguised as a corporate disaster? This pullback is a healthy, albeit painful, recalibration that separates speculative tourists from long-term investors. Novo Nordisk will survive this turbulence, and it will likely emerge stronger once the market remembers that obesity remains a chronic, global pandemic requiring decades of treatment.