The myth of the blank check: How the French healthcare system actually views the ER

Expats and tourists frequently arrive in the Hexagon under the illusion that the Sécurité Sociale operates as a philanthropic, zero-cost paradise. It does not. The backbone of the French medical apparatus relies on a co-payment mechanism. While the state covers the lion's share of your medical expenses, a residual balance almost always lands on the patient. This structure is designed to prevent systemic abuse, yet it catches outsiders completely off guard.

Deconstructing the base rate and user fees

When you present yourself at a public hospital's urgences, you trigger a complex administrative mechanism. The state health insurance fund, known locally as l'Assurance Maladie, fundamentally handles 80% of the standard treatment costs for inpatient emergency stays. But wait, what about the remaining chunk? That is where things get complicated. The patient is legally responsible for the remaining 20% ticket modérateur, alongside a fixed daily hospital maintenance fee known as the forfait hospitalier, which currently sits at 22 euros per day.

The game-changing introduction of the Forfait Patient Urgences

To streamline the paperwork for non-admitted patients, the French government overhauled the entire billing framework. Enter the Forfait Patient Urgences (FPU), a flat fee introduced to simplify the system. If you visit the ER, receive treatment, and leave without being formally admitted to a hospital bed, you are slapped with a flat 19.61 euros charge. It sounds manageable, right? Except that if you do not possess a local insurance card, the hospital will bill you the true, unsubsidized cost of the medical acts, which easily spirals into the hundreds. And yes, they will track you down across international borders to collect it.

Navigating the triage: Technical costs behind those emergency room doors

Let us look under the hood of a real-world emergency scenario. Imagine you trip over a cobblestone near the Place de la Bastille and suspect a fractured ankle. You crawl into the nearest public facility, the Hôpital Saint-Antoine. The financial trajectory of your evening depends entirely on whether you have a small green piece of plastic called a Carte Vitale or a valid European Health Insurance Card (EHIC).

The stark divide between Euro-residents and global travelers

For a French citizen or a registered expat holding a Carte Vitale, the system works like clockwork. The Assurance Maladie communicates directly with the hospital database through a process called tiers-payant, meaning you do not advance the primary funds. But what happens if you are a tourist from Chicago or Tokyo? You pay upfront. The hospital billing department will generate a document called a Feuille de Soins, demanding full payment of the raw medical fees before you exit or via a subsequent invoice sent to your home address. Honestly, it's unclear why so many travel blogs gloss over this brutal administrative reality.

The hidden costs of diagnostics and specialist interventions

People don't think about this enough, but the flat FPU fee only covers the basic emergency consultation. The moment a physician orders an MRI scan, an ultrasound, or requires the expertise of an on-call orthopedic surgeon, the financial ledger expands. Each medical act is codified under a strict national tariff system, the Classification Commune des Actes Médicaux (CCAM). If you lack proper coverage, an evening involving blood work, a CT scan, and a temporary cast can easily accumulate a total bill of 450 to 800 euros. That changes everything for a budget traveler.

The safety nets: Mutuelles and international travel insurance policies

Where it gets tricky is understanding how locals actually achieve that legendary "free" healthcare status. They do not rely solely on the government. Instead, they use a mutuelle, a top-up private insurance policy that bridges the fiscal gap left by the state.

The symbiotic relationship between the state and the Mutuelle

A standard French mutuelle automatically absorbs the 19.61 euros FPU or the 20% ticket modérateur plus the daily forfait hospitalier. Consequently, the patient experiences a net-zero transaction at the point of care. I have seen countless foreigners look bewildered when a French friend walks out of an ER without opening their wallet; this private-public partnership is the exact reason why. Without this secondary insurance layer, you are fully exposed to those residual fees, which explains why having a robust policy is not just a good idea, it is a financial necessity.

Public hospitals versus private clinics: The emergency room fork in the road

Not all emergency rooms in France are created equal, and choosing the wrong door can decimate your vacation budget. The distinction between a public Hôpital and a private Clinique is paramount when it comes to billing practices.

The perilous world of dépassements d'honoraires

Public institutions adhere strictly to conventional state tariffs. Private clinics, however, frequently employ doctors who practice Secteur 2 medicine. What does this mean for your wallet? These practitioners have the legal right to charge dépassements d'honoraires, which are discretionary extra fees above the official state reimbursement rate. If you land in a private emergency clinic in the upscale 16th arrondissement of Paris, the physician might bill you 150 euros for a consultation that the state only values at 25 euros. The state insurance will still only reimburse 80% of that basic 25-euro rate. The issue remains: who covers the massive surplus? You do, unless your international insurance or premium mutuelle specifically covers uncapped private fees. We are far from a free system when these capitalistic elements enter the medical equation.

Common Myths and Misconceptions Surrounding French Urgent Medicine

The Illusion of the Blank Check

You trip on a Parisian cobblestone, fracture your ankle, and hitch a ride in an ambulance. Many expats blindly assume the state absorbs every single centime because of Europe's legendary welfare reputation. Let's be clear: this is a financial fantasy. While the medical act itself remains heavily subsidized, the system operates on a co-payment architecture. Is emergency care free in France? Not entirely, because the concept of the ticket modérateur requires patients to cover a slice of the pie, which usually hovers around twenty percent of standard hospital fees. If you lack supplementary insurance, that fractured ankle will trigger a paper invoice mailed directly to your residence.

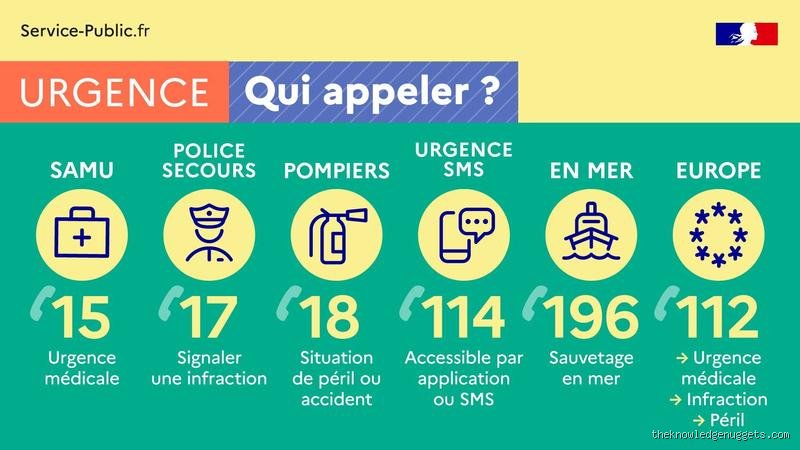

The Confusion Between SAMU and Private Transport

Dialing 15 or 112 connects you to the medical dispatch universe, but it does not guarantee a cost-free ride. People frequently conflate the public utility of SMUR responder vehicles with ordinary ambulance companies. The problem is that private transport companies operate under distinct tariff structures. Unless a regulator explicitly validates the absolute urgency of your transportation, you might face an unexpected bill. But what happens if you just call a taxi because you are panicking? You pay out of pocket, completely bypassing the national insurance coverage safety net.

The Forfait Patient Urgences: An Expert Perspective

The Flat-Fee Revolution You Need to Navigate

In recent years, the French healthcare apparatus introduced a mechanism called the Forfait Patient Urgences to streamline administrative bottlenecks. What does this mean for an uninsured traveler or an unregistered expat? If you visit an emergency department without being subsequently admitted to a hospital bed, a fixed fee of 19.74 Euros applies instantly. It sounds minuscule, yet it catches thousands of global wanderers off guard every month. This flat rate replaces the old, unpredictable percentage-making calculations for minor emergency consultations. It is a brilliant administrative shortcut, except that it forces individuals to pay on the spot via credit card or face collection agencies later. Which explains why carrying proof of your European Health Insurance Card or a private global policy matters even during casual weekend strolls. My professional advice is simple: always demand the Bulletin de Situation document before exiting the clinic doors, as this paperwork serves as your ultimate weapon for insurance reimbursement tracking.

Frequently Asked Questions Regarding Urgent Medical Fees

What happens if an uninsured non-EU tourist requires immediate life-saving surgery?

When a catastrophic medical event strikes a non-European Union citizen, French public hospitals prioritize biological stabilization over financial interrogation. Medical staff will perform complex procedures immediately without demanding an upfront credit card swipe. However, the administrative machinery grinds onward behind the scenes, culminating in a substantial invoice based on the Tarifs de Prestation framework. A three-day stay in an intensive care unit can easily skyrocket past 9000 Euros for individuals lacking proper coverage. As a result: the hospital billing department will aggressively pursue the patient or their home country insurance provider once the physical danger subsides.

How does the European Health Insurance Card alter the billing process for tourists?

Possessing a valid European Health Insurance Card simplifies the financial labyrinth significantly for continental travelers. This document proves you are integrated into another European state's social architecture, allowing French hospitals to communicate directly with your home country's bureaucracy. You will generally only need to clear the minor 19.74 Euros emergency flat-fee rather than confronting the massive primary medical bill. The issue remains that this card does not cover private clinic upgrades or repatriation costs if you need a specialized flight home. Is emergency care free in France for our neighbors? No, but it reduces the immediate monetary friction to the price of a modest bistro lunch.

Are victims of major public disasters or sudden labor contractions charged for services?

The French republic carves out strict, compassionate exemptions for specific critical categories within its medical legislation. Women who have reached their sixth month of pregnancy receive absolute 100 percent coverage for any sudden, urgent obstetric interventions. Similarly, individuals caught in legally recognized acts of terrorism or major industrial catastrophes face zero financial liability at the point of care. The state assumes total fiscal responsibility here, meaning the standard flat rates and co-payments dissolve completely. In short, the system acknowledges that certain societal traumas transcend ordinary consumer-based medical economics.

A Grounded Assessment of the French Safety Net

We routinely romanticize foreign healthcare frameworks until the reality of foreign administrative paperwork hits our mailboxes. France possesses an undeniably spectacular infrastructure that refuses to abandon human beings in moments of physiological terror, a stance I deeply admire. Yet, calling this setup entirely free is a linguistic lie that endangers your personal bank account. Do not let the comforting rhetoric of universal coverage trick you into traveling without robust financial protection. The system relies on precise bureaucratic documentation, and lacking it turns a minor medical mishap into a stressful accounting headache. Ultimately, you will be saved first, but you will absolutely be billed later.