Let us look at how the machinery actually functions under the hood. When a publicly traded company distributes cash to its backers, the market automatically adjusts the equity value downward by roughly the exact amount of that coupon on the ex-dividend date. This is not a glitch; it is basic math because cash is leaving the corporate balance sheet. The dividend stripping strategy hinges entirely on this predictable, engineered volatility. An arbitrageur enters the fray at the eleventh hour, snaps up shares at the inflated pre-dividend price, pockets the cash distribution, and dumps the position into a falling market. What looks like a clumsy, immediate trading loss on paper is actually a calculated play to transform high-tax ordinary income into a highly useful, tax-deductible capital deficit.

The Mechanics Behind the Trade: How Investors Arbitrage the Corporate Calendar

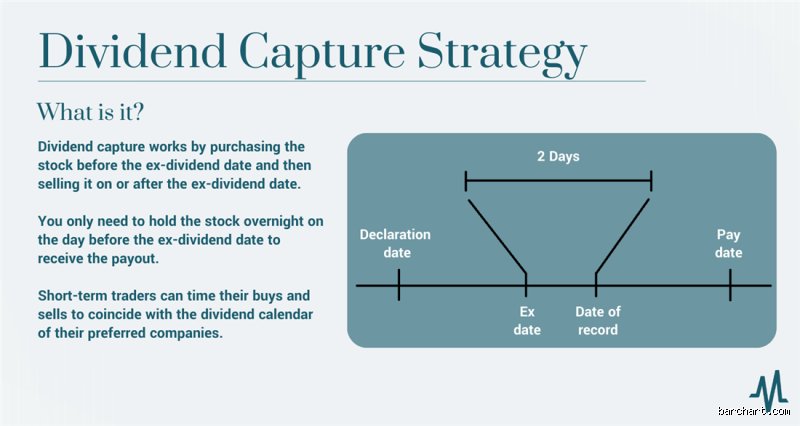

The entire playbook relies on a tight, four-stage corporate timeline that governs every single cash distribution. First, the board announces the payment size. Then comes the record date, which determines who actually owns the underlying security. But where it gets tricky is the ex-dividend day, falling exactly one business day prior to the record date due to modern settlement clearing cycles. If you buy on that day or later, you miss out on the payout. The final piece is the actual payment date, which often lags by several weeks.

The Critical 48-Hour Settlement Window

Timing is everything here, and being late by even a few seconds ruins the trade. The strategic buyer must execute the purchase at least one full day before the ex-dividend date. Because of this structural setup, the trader secures a legal right to the incoming cash flow. But why go through this frantic dance? The answer lies in asymmetric tax treatment, yet this assumes the price drop mirrors the dividend perfectly, which rarely happens in chaotic, live markets. And honestly, it's unclear why more retail investors don't realize that transaction friction can eat these slim margins alive.

Capturing the Yield While Engineering a Capital Loss

Imagine a blue-chip firm trading at $100 per share that declares a massive $4 special distribution. The dividend stripping strategy requires buying the stock at $100. On the ex-dividend morning, the stock price naturally gaps down to $96 to reflect the cash extraction. The trader sells immediately at $96, booking a clear $4 capital loss per share. Meanwhile, they receive the $4 cash payment a few weeks later. On paper, the gross economic profit is exactly zero dollars. However, the clever part is how those two distinct financial events are treated by the internal revenue service of various jurisdictions.

The Tax Arbitrage Playbook: Turning a Trading Deficit into Fiscal Advantage

The real magic happens when you look at the mismatched tax rates applied to different types of investment returns. In many Western jurisdictions, capital losses can be used to aggressively wipe out capital gains realized from other profitable ventures, like selling a piece of real estate or a startup company. If you are sitting on a massive, taxable short-term capital gain, creating a synthetic loss through this equity maneuver can neutralize your fiscal liability significantly. People don't think about this enough, but tax codes are inherently uneven. I believe that ignoring these structural loopholes is akin to leaving money on the table, though the legal boundaries are constantly shifting beneath our feet.

The Holding Period Hurdle and Anti-Avoidance Rules

Regulators are not stupid, which explains why they built massive legal speed bumps to stop institutional abuse of this loophole. In the United States, for instance, the Internal Revenue Code enforces strict holding period requirements under Section 246(c). To qualify for preferential tax rates on that incoming cash, you must hold the equity for more than 60 days within a specific 121-day window surrounding the ex-dividend date.

Common mistakes and misconceptions when chasing dividends

Falling into the high-yield trap

Yield-chasing ruins portfolios. Retail players often spot an equity boasting a 14% annual payout and instantly trigger a buy order, convinced they discovered a secret money machine. The problem is that equity prices collapse by the exact magnitude of the distribution on the ex-dividend date. If a stock trades at $100 and yields $10, it opens at $90. You have not generated wealth; you merely restructured your capital while triggering an immediate tax liability.

Ignoring the strict settlement timeline

Timing is everything, yet amateurs consistently miscalculate the transaction mechanics. To execute a successful dividend stripping strategy, you must own the underlying asset before the ex-dividend date, not the record date. Why does this distinction trip up so many traders? Because brokerage clearing houses utilize a T+1 or T+2 settlement protocol. If you purchase shares on the ex-date itself, the cash distribution belongs entirely to the seller, leaving you holding an asset that just dropped in market value.

Misjudging the friction of transaction costs

Friction burns alpha. Executing this playbook requires high-frequency turnover across substantial positions. But let's be clear: entry fees, exit commissions, and the inescapable bid-ask spread eat your margins alive. If you scrape a gross profit of 0.80% on a position but burn 0.45% in execution friction, your net risk-adjusted return becomes pathetic.

---

The structural arbitrage: A sophisticated alternative approach

Exploiting the options market mismatch

Institutional desks rarely execute a dividend stripping strategy using straight equity. Instead, they weaponize deep-in-the-money put options to hedge the downside volatility of the underlying asset during the distribution window. By buying the equity and simultaneously purchasing a put option with an identical strike price, professionals lock in a floor price.

Cum-ex variations and regulatory crackdowns

The global landscape changed because European tax authorities cracked down hard on structural dividend arbitrage schemes. The historical

cum-ex scandal costing treasuries over $60 billion proved that systemic exploitation of withholding tax loopholes carries severe criminal risks. Modern practitioners avoid synthetic duplicate claims entirely. Today, sophisticated operators focus strictly on cross-border tax treaty asymmetry, utilizing contract-for-difference derivatives to capture distributions in jurisdictions where domestic withholding rates stand at 0% while foreign entities face a 30% haircut.

---

Frequently Asked Questions about dividend capture tactics

Is the dividend stripping strategy legally permitted across global financial markets?

Legality depends entirely on your jurisdiction and your specific holding period. In the United States, the Internal Revenue Service enforces

Section 246c of the Internal Revenue Code, which dictates that you must hold common stock for more than 60 days during a 121-day window surrounding the ex-dividend date to claim the preferential 15% or 20% qualified dividend tax rates. If you hold the asset for less time, the distribution gets taxed at ordinary income rates which can top 37%, rendering the entire quick-flip trade unprofitable. European regulators are even more aggressive, frequently reclassifying ultra-short-term dividend arbitrage positions as tax evasion rather than legal avoidance.

How does market volatility impact the success of this short-term trading setup?

Macro volatility completely breaks this trade. During bearish market regimes, the systemic downward pressure on an index can easily swamp the predictable price drop seen on the ex-dividend morning. For instance, if a company distributes a 2% payout but the broader S&P 500 drops 3.5% on the same trading day due to an unexpected macroeconomic report, your hedged position will collapse far beyond the distribution value. As a result: your anticipated arbitrage vanishes into a net capital loss.

What size account is required to make dividend capture techniques viable?

You need serious capital to make this endeavor worth your time. Due to the tiny margins available per trade, executing a dividend stripping strategy with an account balance under $2