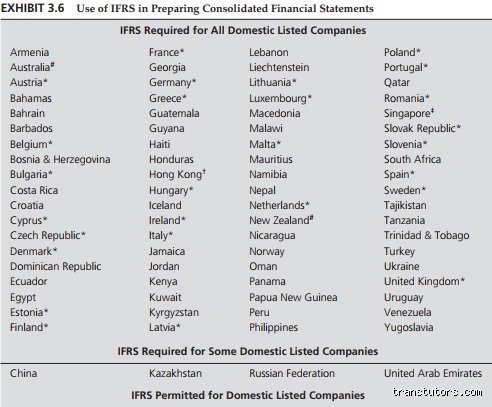

The Jurisdictional Boundary: Why the IASB Doesn't Actually Hold the Gavel

Here is where it gets tricky for most financial analysts. The International Accounting Standards Board (IASB) designs these pristine, theoretically beautiful standards, but they possess zero sovereign enforcement power. They cannot tell a single company in London, Tokyo, or Toronto what to do. Sovereign governments or local securities regulators—like the Financial Conduct Authority (FCA) in the United Kingdom or the Securities and Exchange Commission (SEC) in the United States—must explicitly adopt these rules into law. Consequently, the answer to which of the following entities are not permitted to use IFRS changes dramatically depending on whether your corporate headquarters sits in Delaware or Berlin.

The Concept of Public Accountability as a Line in the Sand

The IASB itself sets a internal boundary based on a specific characteristic: public accountability. If your entity issues debt or equity instruments on a public market, or if you hold assets in a fiduciary capacity for a broad group of outsiders—think commercial banks, credit unions, and insurance conglomerates—you are not just permitted to use full IFRS; you are usually forced to. But what about the local bakery chain with twelve locations? They lack this specific public profile. Because of this, the standard setters actively discourage, and in several jurisdictions legally prohibit, non-publicly accountable entities from using the bloated, complex full-scale version of the international framework, guiding them instead toward a stripped-down alternative.

The Great American Redline: U.S. Domestic Issuers and the SEC Gridlock

Let us look at the elephant in the financial room. The United States remains the most prominent holdout against full international integration, a situation that drives multi-national auditors absolutely insane. If you are a U.S. domestic registrant—a corporation incorporated in the United States and listing shares on the New York Stock Exchange (NYSE) or NASDAQ—you are strictly not permitted to use IFRS for your official SEC filings. Period. I find it fascinating that despite decades of Norwalk Agreements and convergence projects aimed at blending systems, the SEC still firmly demands U.S. GAAP (Generally Accepted Accounting Principles) from its homegrown corporate giants.

Foreign Private Issuers vs. The Homegrown Giants

But there is a hypocritical twist here that people don't think about this enough. A foreign company listing on an American exchange, like the German automotive titan BMW Group, can submit its financial statements using IFRS without any reconciliation to U.S. GAAP. This exemption was carved out by the SEC in November 2007 to maintain Wall Street's competitive edge. Yet, if Apple or Microsoft tried to hand over an IFRS-compliant ledger tomorrow? The SEC would reject it instantly. That changes everything for corporate structuring, forcing American multinationals to maintain dual-ledger systems if they operate heavy foreign subsidiaries.

The Massive Dollar Drain of Dual Reporting

The financial consequences of this regulatory stubbornness are staggering. Consider a massive American conglomerate operating across the European Union. Because the EU mandated IFRS under Regulation No 1606/2002 for all listed companies, the European subsidiaries must report upwards using international metrics. Meanwhile, the parent company back in California must translate those exact same transactions back into U.S. GAAP format for its quarterly 10-Q filings. We are talking about hundreds of millions of dollars spent annually on specialized accounting software and enterprise resource planning upgrades just to handle differing treatments of lease liabilities under IFRS 16 vs. ASC 842. It is an administrative nightmare that keeps big four accounting firms incredibly wealthy.

The Small Business Exclusion: When Full IFRS Becomes Legal Overkill

Away from the high-stakes drama of Wall Street, the question of which of the following entities are not permitted to use IFRS applies heavily to the engine room of the global economy: small and medium enterprises. In many European and Asian jurisdictions, an unlisted private company is statutorily barred from using the full version of the international standards for their statutory filings. Why? Because full international standards require complex valuations, such as calculating the fair value of biological assets under IAS 41 or assessing hyperinflationary adjustments under IAS 29.

The Absurdity of Forcing Small Firms into Global Molds

Imagine forcing a family-owned vineyard in Bordeaux to calculate the fluctuating fair value of its unharvested grapes every quarter using complex mathematical modeling. It is absurd. Local tax authorities don't want it, and the local bank extending a modest line of credit certainly doesn't need 300 pages of footnotes regarding derivative financial instruments. Hence, local corporate laws in countries like France or Germany mandate that these smaller, private entities must use local national accounting standards—such as the Handelsgesetzbuch (HGB) in Germany—rather than the international framework.

Evaluating the Alternatives: The IFRS for SMEs Framework

To fix this obvious disconnect, the IASB published a separate, scaled-down book of rules known as the IFRS for SMEs Standard. This is not just a shorter version of the main text; it is a completely distinct framework that strips out roughly 90 percent of the disclosure requirements. It completely eliminates complex topics like earnings per share calculations, interim financial reporting, and the asset-held-for-sale classification.

Who Can and Cannot Move Down the Regulatory Ladder?

The rules governing who can access this simpler framework are rigid. If an entity possesses public accountability, it is strictly not permitted to use the SME version, even if its actual asset size is tiny. Conversely, if a country has not explicitly adopted the SME standard into its national legal framework, local private companies cannot just decide to use it on a whim. For instance, in the United Kingdom, private entities generally use a localized variation called FRS 102, which incorporates elements of international concepts but remains distinct, meaning we're far from a truly unified global private standard. The issue remains that until regional regulators align their tax laws with these international simplifications, private businesses will continue to face fragmented reporting environments depending entirely on their geographic borders.

Common mistakes and misconceptions about IFRS eligibility

The myth of universal public accountability

Many practitioners assume that any company possessing public accountability must automatically deploy full IFRS. This is a trap. The problem is that the International Accounting Standards Board defines public accountability broadly, but local jurisdictions wield the actual veto power. For instance, a small regional credit union might hold public deposits, which technically triggers the criteria under international definitions. But what happens if the local central bank mandates a strict domestic prudential framework instead? The local rule wins every single time. You cannot just look at the London-based guidelines and assume they dictate reality on the ground in Ohio or Tokyo.

Confusing the SME standard with the full framework

Another frequent blunder involves treating the IFRS for SMEs Standard as a mere subset that anyone can adopt at will. This is where things get messy. Micro-entities and solo traders often view this scaled-down framework as a golden ticket to international prestige, except that it specifically bars entities with public accountability. If a business issues publicly traded debt, it is completely blocked from using the SME version. Which entities are not permitted to use IFRS in its simplified form? Any organization whose debt or equity instruments are actively traded on a public market, regardless of how small their actual balance sheet might look.

The assumption that domestic listing guarantees compliance

Do not confuse a domestic listing with a blanket permission to use international rules. Certain major economies deliberately lock their domestic listed entities out of the pure IFRS ecosystem. Consider the United States, where the Securities and Exchange Commission mandates US GAAP for domestic issuers. A homegrown Delaware corporation listed on the New York Stock Exchange cannot legally file pure international standards. It is forbidden. They must stick to local codification, demonstrating that listing status does not automatically grant a passport to international reporting templates.

A little-known aspect: The shadow ban of prudential carve-outs

When central banks overwrite international standards

Let's be clear about how sovereign banking regulations quietly sabotage financial reporting harmonization. Even when a nation claims full adoption, the central bank often quietly introduces prudential carve-outs that completely alter loan-loss provisioning. In these scenarios, a commercial bank might claim it follows international rules, yet its core credit calculations are dictated by local statutory decrees. Is it truly using the framework? Not really, because these forced modifications mean the final financial statements cannot include an unreserved statement of compliance with International Financial Reporting Standards. It creates a bizarre regulatory limbo where a bank looks like it is compliant, but the underlying numbers tell a completely different, highly localized story.

This hidden layer of restriction catches cross-border investors off guard. If a local regulator forces a bank to maintain a static 2% general provision on all commercial loans regardless of the forward-looking expected credit loss model, the integrity of the international framework collapses. As a result: the entity is effectively banned from claiming true compliance. The issue remains that sovereign capital requirements will always override theoretical accounting purity when a systemic financial crisis threatens a local economy.

Frequently Asked Questions

Can US-based private companies choose to file under international standards?

Yes, but this permission is highly conditional and depends entirely on the requirements of their specific financial stakeholders. While the AICPA recognizes the IASB as an official accounting standard setter, allowing private firms this option, which of the following entities are not permitted to use IFRS boils down to private contractual restrictions rather than federal law. If a syndicate of American banks demands US GAAP as a condition for a $50 million credit facility, the company is effectively blocked from using international rules. Furthermore, if that private entity decides to launch an initial public offering on an American exchange, the SEC will immediately reject their international filings. Thus, private adoption remains a fragile privilege rather than an absolute legal right in the American market.

How do US GAAP and international rules handle investment properties differently?

The divergence here is stark because the underlying valuation philosophies are fundamentally opposed. Under international rules, specifically IAS 40, an entity can choose to value its investment property using a fair value model, recognizing valuation changes directly in the income statement. US GAAP completely outlaws this approach for standard corporate entities, forcing them to use the historical cost model less accumulated depreciation. Because of this structural prohibition, an American real estate firm cannot simply pivot to international rules to inflate its asset base for domestic reporting purposes. This conceptual divide means that a portfolio worth $1.5 billion on a fair value basis might be locked at a historical cost of $900 million under domestic rules, forcing global analysts to completely rebuild the financial statements to achieve any semblance of comparability.

Are government-owned business enterprises allowed to utilize the international framework?

The answer depends entirely on whether the specific state-owned enterprise operates with a commercial profit motive or functions purely as a public service vehicle. Government business enterprises that sell goods and services to the public on a commercial basis were historically encouraged to use these standards, but pure public sector entities must use International Public Sector Accounting Standards instead. In jurisdictions like Canada, the transition rules explicitly delineated which crown corporations had to adopt international standards and which had to remain within the public sector accounting handbook. If an entity relies on continuous government appropriations to survive, representing over 60% of its annual operating budget, it is generally barred from using commercial international standards. This boundary ensures that public funds are tracked through accountability models designed for governance rather than market profitability.

A definitive perspective on the future of reporting boundaries

The dream of a single global accounting language is dead, or at least permanently stalled on the reef of national sovereignty. We must accept that political boundaries will always dictate financial reporting boundaries, regardless of how loud global investors clamor for uniformity. When a superpower like the United States refuses to cede regulatory control to an independent London board, it proves that accounting is ultimately an exercise in geopolitical power. Which entities are banned from using international standards is not a technical question for auditors; it is a political decision made by sovereign states protecting their domestic capital markets. Investors who blindly trust the "international" label without checking local regulatory overrides are bound to misprice risk. True comparability is an illusion, which explains why savvy analysts spend more time reading the fine print of jurisdictional reconciliations than the actual face of the financial statements. We will never see total harmonization, and honestly, pretending otherwise is just administrative delusion.