Let us be real for a second. We have all looked at those colorful retirement brochures with the silver-haired couples drinking wine on a porch and thought, "That will be me eventually." Except that for most of us, the math is actively working against that postcard fantasy. The global retirement landscape is fractured, stubborn, and increasingly broke, which explains why governments keep moving the goalposts. I used to think the system was logical; now I realize it is just a giant game of musical chairs where the music slows down every single decade. You cannot just coast into your sixties and expect a check.

Decoding the True Definition of Qualifying Years and Pensionable Service

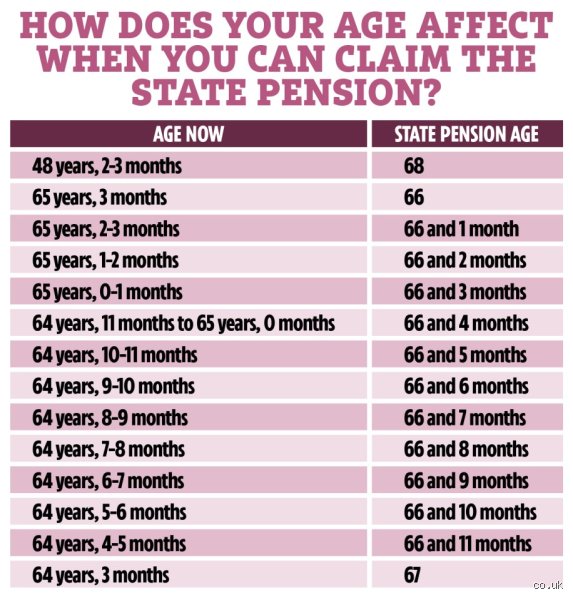

Before we even look at the calendars, we have to talk about what a year actually means to a government auditor. It is rarely 365 days of sitting at a desk. In the United Kingdom, for example, a qualifying year is built on National Insurance contributions. You either paid them through your payslip, or you received credits because you were raising kids or dealing with an illness. People don't think about this enough until they are 62 and looking at a massive shortfall.

The Trap of the Minimum Threshold

Where it gets tricky is the absolute baseline. If you do not hit the floor, you get nothing. Zero. In the British system, that floor is 10 qualifying years. If you work for nine years and 11 months, then decide to move to a beach in Spain without paying another dime, the state keeps your money. And honestly, it's unclear why more financial advisors do not scream this from the rooftops. You need that decade just to get a pro-rata sliver of the basic state pension. To get the maximum amount? That requires a staggering 35 years of immaculate record-keeping.

The Ghost Years That Disappear From Your Record

And then you have the gaps. A year spent backpacking through Asia or taking time off to care for an elderly relative might feel fulfilling, yet it leaves a crater in your pension history. These are what compliance officers call non-contributory periods. Unless you actively buy back those missing years through voluntary contributions, they sit on your record like blank spaces on a map, quietly dragging down your final payout when you eventually cross the finish line.

The American Scenario: Navigating the 40-Quarter Social Security Maze

Cross the Atlantic, and the vocabulary changes entirely, though the underlying bureaucratic headache remains identical. The United States does not care about your years. They care about your credits, specifically 40 Social Security credits.

How the Quarter System Actually Tallies Up

You can earn a maximum of four credits per year. Hence, the quick math tells you that 40 credits equals 10 years of work. But here is the kicker: the financial threshold to earn a single credit is remarkably low, meaning a part-time college job in Boston back in 2012 might actually count just as much as a high-powered corporate gig in Manhattan did last year. In 2026, you earn one credit for every 1,810 dollars of earnings. Once you hit 7,240 dollars for the year, you have maxed out your four credits for that calendar cycle. That changes everything for seasonal workers, but it also creates a false sense of security.

The 35-Year Calculation Engine

Because while 10 years gets you into the club, it will not buy you a drink at the bar. The Social Security Administration calculates your Primary Insurance Amount using your 35 highest-earning years, adjusted for inflation. What happens if you only worked for 25 years? The system plugs in a big, fat zero for those 10 missing years. Those zeros act like an anchor, dragging your average down into the mud. So, how many years do you need to claim a pension that actually covers your groceries? You need 35 full years of high-velocity earnings if you want to avoid the penalty of the zero-dollar placeholder.

The Early Retirement Penalty Slapped on Gen X

But say you want out early. You are tired, your back hurts, and you want to claim at 62. The government lets you, but they will slice your monthly check by up to 30 percent compared to waiting until your Full Retirement Age, which is now 67 for anyone born after 1960. It is a brutal mathematical haircut that lasts for the rest of your natural life.

The European Complexity: Where Contribution Lifetimes Dictate Reality

If you think the Anglo-American systems are rigid, the continental European approach is a whole different level of intensity. Here, they do not just look at a flat decade; they demand an entire lifetime of labor.

France and the Trimestre Battleground

Take France, a country that practically views retirement as a constitutional right, yet fiercely guards the treasury. The system here revolves around trimestres, or quarters. To secure a full, unpenalized state pension, workers must accumulate up to 172 trimestres, which translates to 43 years of active contributions. That is nearly half a century of labor. When the government pushed the legal retirement age from 62 to 64, it caused literal riots in the streets of Paris, which explains why pensions are the most volatile political third rail in Europe. If you enter the workforce late because you were pursuing a PhD, you might find yourself working until you are nearly 70 just to avoid a permanent discount on your Euro-denominated payout.

Germany and the Rule of the Points

Germany operates on a slightly different philosophy but with equal rigor. Their statutory insurance system requires a minimum of five years of contributions for a basic old-age pension, but the standard retirement age is creeping steadily toward 67. The Germans use a system of Entgeltpunkte, or pension points, tied directly to how your income compares to the national average each year. It is an algorithmic approach where time spent working is inextricably linked to economic performance, leaving very little room for sentimentality or early exits.

Global Benchmarks: How Countries Stack Up on the Timeline

To see how wildly these rules diverge, we have to look at the global spectrum. The number of years you need to claim a pension is entirely a product of geography and local birth rates.

The Comparison Matrix

Look at Australia. Their system is built on the Age Pension, which relies on residency rather than direct employment taxes. You must have been an Australian resident for at least 10 years, with at least five of those years in one continuous block. It is a completely different philosophical approach compared to the French model. Meanwhile, Canada uses a dual system: the Old Age Security, which requires 10 years of residence after the age of 18, and the Canada Pension Plan, which requires at least one valid contribution from your earnings. The variation is dizzying, as a result: a global worker can easily end up with a fragmented patchwork of micro-pensions spread across three continents, none of which quite add up to a livable wage on their own.

The Demographic Timebomb Forcing the Shift

Why is this happening everywhere? Because people are living longer and having fewer babies. The dependency ratio is collapsing. In the 1950s, there were several workers supporting every single retiree; today, we are far from it. This structural shift is why governments are quietly tweaking the algorithms, turning the knobs behind the scenes so that the answer to how many years do you need to claim a pension keeps ticking upward, year after miserable year.

Common retirement misconceptions and traps to avoid

The myth of the universal 10-year rule

You probably think a single decade of labor guarantees a golden handshake from the state. It does not. While the US Social Security system requires 40 credits, which usually translates to ten years of covered employment, crossing the Atlantic changes the entire calculus completely. Try applying that logic in France. There, you need up to 43 years of contributions to dodge a permanent haircut on your payouts, depending on your birth year. The problem is that workers conflate the minimum threshold to receive anything at all with the requirement to secure a liveable, unreduced check.

Assuming your international years vanish

Migrant workers often panic needlessly. They assume their transient career paths mean abandoning cash left behind in foreign coffers. Except that bilateral totalization agreements rescue these fragmented histories. If you split your life between London and Chicago, the US and the UK will tally your combined service to help you qualify. But don't celebrate just yet. Each nation computes its actual cash distribution based solely on the specific weeks you spent within its borders, meaning you might need to manage multiple micro-pensions across various time zones during your twilight years.

The hidden leverage of voluntary contributions

Buying back time when your timeline falls short

What happens if you discover you lack the requisite tenure? You can actually write a check to erase your past laziness or career gaps. Many European systems, alongside the British National Insurance framework, offer a mechanism called voluntary Class 3 contributions. Let's be clear: this requires immediate liquidity. Spending several thousand dollars today to plug a five-year hole from your chaotic twenties might seem painful, yet the long-term mathematical payoff often eclipses traditional market investments. It is the ultimate bureaucratic cheat code for those wondering how many years do you need to claim a pension when their official record looks like Swiss cheese.

Frequently Asked Questions

Can I claim a pension if I only worked 5 years?

In most developed Western economies, a five-year stint leaves you empty-handed regarding state funds. Germany, for instance, enforces a strict five-year minimum qualifying period (Wartezeit) before you can touch a single eurocent of statutory retirement cash. If you fall short by even one month, the system locks you out completely. However, certain enterprise-level corporate plans vest much faster, sometimes requiring only two years of continuous service under specific domestic labor laws. As a result: short-term workers must rely heavily on private investments or totalization treaties rather than national safety nets.

Do periods of unemployment or parental leave count toward my timeline?

Yes, but the administrative nuances will make your head spin. Many progressive states grant credited contributions during certified spells of sickness, mandatory military service, or child-rearing. Take Sweden, where the system actively injects fictional earnings into your account during your child’s first four years. But because these credits are tied to national averages, they rarely match the fiscal weight of a high-flying corporate salary. And if you fail to register your unemployment correctly with the local bureau, those empty months will permanently damage your average lifetime earnings calculation.

What happens to my pension years if my employer went bankrupt?

Your hard-earned history does not simply evaporate into thin air when corporate boards fail. In the United States, the Pension Benefit Guaranty Corporation steps in to protect and pay out defined benefit plans up to statutory caps, ensuring your service years remain valid. Across the United Kingdom, the Pension Protection Fund performs a nearly identical rescue mission for stranded workers. The issue remains that these government lifeboats might not honor the extravagant top-tier bonuses or specific early-retirement promises your original boss guaranteed. (Nobody ever said corporate insolvency was completely painless.)

A definitive verdict on your retirement timeline

Stop looking for a magic, universal number because it simply does not exist in modern demographics. Relying on lazy assumptions about how many years do you need to claim a pension will guarantee financial ruin. You must aggressively audit your specific national requirements today rather than waiting for a government letter that arrives far too late. Bureaucrats designed these systems to reward lifelong conformity, not nomadic flexibility. We must take radical ownership of our employment records by archiving every payslip like weapons for an inevitable future dispute. Complacency is an expensive luxury you cannot afford when aging states are actively moving the retirement goalposts under our feet.