The Statistical Reality of the Talent Drain in Modern Finance

Numbers don't lie, but they certainly can be depressing when you look at the Bureau of Labor Statistics data from the last few years. We are witnessing a demographic pincer movement where older CPAs are retiring at a clip that the younger generation simply isn't interested in matching. The math is simple: more people are exiting the revolving door than entering the lobby. But why? People don't think about this enough, but the pipeline for new talent has constricted by nearly 33 percent over the last decade. It’s not just that the work is hard—it has always been hard—it’s that the payoff no longer seems to justify the 150-hour credit requirement for licensure. I’ve seen brilliant graduates take one look at the starting salary versus the projected overtime during busy season and sprint toward data science or fintech instead. Can you really blame them for wanting a life outside of a spreadsheet?

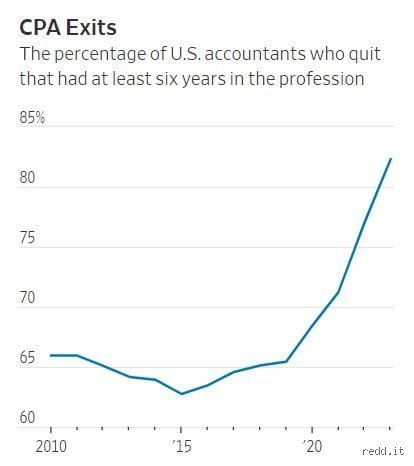

The Disappearing CPA and the 300,000 Person Gap

Between 2019 and 2021, the profession hit a wall. When we ask what percent of accountants quit, we have to acknowledge that the 17 percent drop in employed accountants during that window wasn't just due to natural attrition. It was a mass realization. The issue remains that the traditional "up or out" model of public accounting firms is increasingly viewed as "just out." Firms in major hubs like New York and Chicago are struggling to keep staff through their third year, which is the exact moment an associate becomes truly profitable. Which explains why your local mid-market firm is suddenly offering signing bonuses that look like professional athlete contracts. Yet, even with the cash, the vacancy signs stay lit.

Market Volatility and the Great Resignation Aftermath

The thing is, the pandemic acted as a massive chemical catalyst for a reaction that was already simmering in the breakrooms of every mid-tier firm in the country. Before 2020, you stayed. You gritted your teeth through the 80-hour weeks in February because that was the price of admission. Except that once everyone tasted the autonomy of remote work, the idea of returning to a cubicle to perform soul-crushing audit tie-outs became unbearable. As a result: the turnover rate for accountants spiked to levels that threatened the very stability of corporate financial reporting. It’s a mess.

Deconstructing the Attrition Mechanics: Why 20 Percent is the New Baseline

Where it gets tricky is differentiating between those leaving their specific firm and those abandoning the profession entirely. While what percent of accountants quit their current role might be high, a significant portion are just "firm-hopping" to secure a 20 percent raise and a better title. But a growing, more concerning slice of that pie is leaving for "Industry"—taking roles as internal controllers or FP&A managers where the hours are predictable and the stakes feel less like a life-or-death struggle with the SEC. It is a slow-motion migration that is draining the public sector of its institutional knowledge. Honestly, it’s unclear if the current education system can even keep up with the replacement rate required to keep the lights on.

The Burnout Threshold and the Busy Season Breaking Point

Busy season has always been the industry's rite of passage, a grueling marathon of caffeine and tax forms that tests the limits of human endurance. But the threshold has shifted. In a survey of over 1,000 accounting professionals, nearly 70 percent cited "work-life balance" as their primary reason for eyeing the exit. And because the remaining staff has to pick up the slack for those who left, a vicious cycle of compound burnout is created. Imagine being the last one left in a department of five, staring at a stack of audits that hasn't shrunk since January. That changes everything. You aren't just an accountant at that point; you're a disaster response worker without the cool uniform.

The Salary Stagnation Paradox in a High-Demand Field

You would think that with such high demand, salaries would have skyrocketed across the board, but the reality is more nuanced. While entry-level pay has seen a bump, the "middle class" of accounting—those with 5 to 10 years of experience—has seen their wages struggle to keep pace with inflation and the skyrocketing cost of the mandatory continuing education. Hence, the temptation to jump ship for a tech startup that offers equity and unlimited PTO becomes irresistible. Experts disagree on whether firms can actually afford to pay more without passing the costs onto clients who are already complaining about fees. It’s a classic stalemate where the only ones winning are the recruiters.

The Impact of Automation: Is Technology Pushing People Out?

There is a persistent myth that AI is coming for the accountants, but the irony is that it’s actually the lack of good technology that is driving people away. Most firms are still running on legacy systems that feel like they were programmed in the late nineties, requiring endless manual data entry that would make a Victorian clerk weep. When we examine what percent of accountants quit, we often ignore the "frustration factor" of being a highly educated professional forced to do the work of a mediocre macro. But the transition to AI isn't a silver bullet; it's a double-edged sword that requires even more training and specialized knowledge.

Manual Labor in a Digital Age

We're far from the promised land of "one-click audits." Instead, we are in a purgatory where accountants have to manage the automated tools while still performing the manual checks because the software isn't quite there yet. This "shadow work" adds layers of complexity without reducing the time spent on a task. Because of this, the cognitive load has never been higher. If you spend eight hours a day fighting with a stubborn ERP system, your desire to stick around for a decade to make Partner starts to evaporate pretty quickly. It’s not just about the money—it’s about the dignity of the work itself.

How Accounting Attrition Compares to Other High-Stress Professions

To put things in perspective, we should compare the accounting quit rate to other "prestige" industries like law or medicine. Lawyers typically see a turnover rate of about 18 percent, which is eerily similar to the financial sector, suggesting that any career involving billable hours is inherently prone to leak talent. However, the medical field, despite the immense physical toll, often retains staff longer due to the deep sense of vocational purpose. Accounting, unfortunately, often lacks that emotional hook. Nobody ever wrote a stirring drama about the heroic struggle to reconcile a bank statement (unless you count some very niche Ben Affleck movies). In short, the lack of a "social mission" makes it much easier for a disgruntled senior associate to walk away when things get tough.

Public Accounting vs. Corporate Finance Retention

The gap between public accounting and industry roles is widening into a canyon. While the percent of accountants who quit public firms is high, the retention in private corporate finance is remarkably stable. Once an accountant finds a "home" in a Fortune 500 company, they tend to stay for five to seven years, compared to the two-year average in public audit. This suggests the problem isn't the accounting work itself, but the environment in which it is performed. Firms are basically acting as expensive training grounds for the rest of the economy. They bear the cost of the training, only to lose the asset just as it begins to appreciate. It's a terrible business model, but one that the industry seems strangely committed to maintaining despite the mounting evidence of its failure.

Common mistakes and misconceptions

The prevailing narrative suggests that the Great Resignation was a temporary fever dream, a momentary lapse in judgment where CPAs suddenly decided they preferred baking sourdough to auditing balance sheets. Let's be clear: this is a fallacy. Many executives believe that if they simply toss a 5% raise at a senior associate, the attrition rates in public accounting will miraculously plummet back to pre-2020 levels. The problem is that salary is no longer the sole lever of retention. Because the cognitive load of modern tax law has evolved into a labyrinthine nightmare, a modest pay bump feels like a bandage on a severed limb. We often hear that young professionals lack "grit," which explains why older partners view high turnover as a character flaw in Gen Z rather than a structural failure of the firm. But if the work-life balance is a myth, can we really blame them for seeking the exit?

The lure of the private sector

One massive misconception is that leaving public accounting guarantees a 40-hour work week. It does not. While a controller role at a mid-sized tech firm might offer a 20% jump in base pay, the quarterly close still demands grueling hours. People assume the burnout among financial professionals is exclusive to Big Four environments, yet the private sector often trades variety for repetitive, high-stakes monotony. You might escape the billable hour, but you rarely escape the pressure of the bottom line.

Misreading the 150-hour rule impact

There is a loud contingent claiming that the 150-credit hour requirement for licensure is the only reason people are fleeing. This is a reductive take. While the extra year of tuition acts as a formidable barrier to entry, it doesn't explain why mid-career managers—who have already jumped through that hoop—are resigning in droves. The issue remains that we are over-focusing on the pipeline while ignoring the leak in the bucket itself. Firms that fixate solely on recruitment while ignoring long-term staff retention strategies are essentially pouring water into a sieve.

The hidden psychological cost of the billable hour

Have you ever tried to quantify your worth in six-minute increments for a decade? It is a dehumanizing exercise that transforms human creativity into a commodity. A little-known aspect of this crisis is the "phantom ticking clock" syndrome, where accountants feel guilty for every moment spent not actively producing a work paper. This psychological erosion is a primary driver for why accountants quit their jobs even when the compensation is objectively high. (It is hard to enjoy a high salary when you are too mentally taxed to spend it.) As a result: the industry is facing a quiet exodus of its most empathetic leaders, leaving behind a vacuum of "grinders" who lack the soft skills to mentor the next generation.

The "Boomerang" strategy: An expert pivot

The smartest firms are stoping the frantic search for new grads and are instead building "alumni networks" with teeth. Instead of treating a resignation as a betrayal, we should view it as an external internship. By keeping the door wide open, firms are seeing a small but significant percentage of "boomerang" employees return after two years in industry. These returnees bring back specialized knowledge and, more importantly, the realization that the grass isn't always greener, which effectively lowers the turnover statistics in accounting firms over a five-year cycle. You must stop burning bridges; start building off-ramps that lead back home.

Frequently Asked Questions

What is the average annual turnover rate for large accounting firms?

Recent data indicates that the annual turnover rate in Big Four firms typically hovers between 15% and 20%, though some specialized departments have seen spikes as high as 25% in the last fiscal year. This means that a team of 100 people could lose a quarter of its workforce every twelve months, necessitating a constant, expensive cycle of recruitment and training. Small to mid-sized firms often fare slightly better with 10% to 12% attrition, but they lack the massive HR budgets to absorb these losses. In short, the industry is perpetually in a state of rebuilding its foundational middle management.

Why are so many CPAs leaving for non-accounting roles?

The analytical rigor required to pass the CPA exam is highly transferable, making accountants prime targets for roles in data science, operations, and strategic consulting. Tech companies frequently poach experienced tax professionals not for their knowledge of the tax code, but for their ability to manage complex data sets under extreme pressure. Which explains why we see a 30% increase in accountants pivoting into "FinTech" or "Product Management" roles where the pay is often 1.5 times higher. The profession is no longer just competing with other firms; it is competing with the entire digital economy for the same logical minds.

Does remote work help reduce the percentage of accountants quitting?

The evidence is mixed, but leaning toward "no" if the workload remains unchanged. While 70% of accountants express a preference for hybrid or remote models, the lack of physical boundaries often leads to "leaking" work hours where the laptop stays open until 10 PM. Remote work solves the commute, yet it exacerbates the isolation that contributes to occupational burnout. Firms that offer remote work without reducing the billable hour requirement often see no significant improvement in their retention metrics. Physical location is a secondary concern to the sheer volume of work that needs to be processed.

The verdict on the industry exodus

The accounting profession is currently undergoing a brutal, necessary Darwinian shift that will leave only the most adaptable firms standing. We cannot continue to treat human capital as a renewable resource that will magically replenish itself despite rising resignation trends. The data is a screaming siren: if the industry doesn't kill the billable hour and embrace radical automation, the talent pool will dry up entirely. My stance is that we are witnessing the end of the "sweatshop" era of public accounting, and frankly, it is about time. The firms that survive will be those that prioritize meaningful career architecture over raw productivity. Except that most partners are still too busy staring at last month's realization rates to see the iceberg ahead.