The Illusion of the Eighty-Thousand-Dollar Price Tag

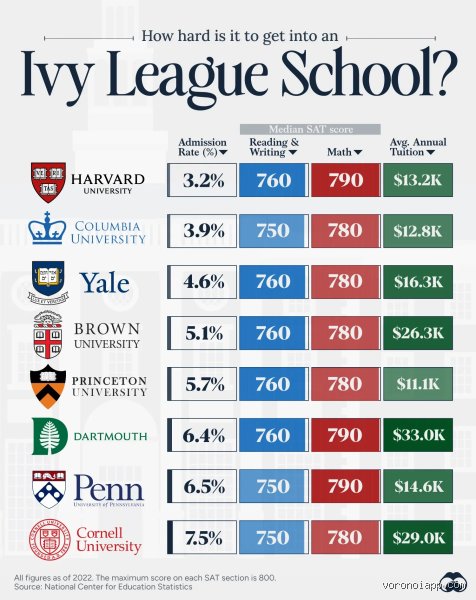

Let us be entirely honest here: looking at the official cost of attendance figures published by university bursars is a complete waste of your time. If you look at the raw data for the 2025-2026 academic year, Harvard College lists a base tuition of around $59,320, while Brown University sits closer to $74,650. But who actually pays that? Wealthy families who can afford to buy a superyacht without blinking, that’s who. The issue remains that the public conflates the retail price with the actual out-of-pocket net cost, missing the entire mechanisms of institutional wealth distribution.

Why Large Endowments Dictate True Affordability

The thing is, elite higher education does not operate on a standard capitalistic supply-and-demand curve. Ivy League universities are essentially multi-billion-dollar hedge funds that happen to run historic classrooms on the side. When Princeton boasts an endowment valuation floating near $34 billion, it does not need your tuition dollars to keep the lights on in Firestone Library. As a result: they can afford to undercut every public university in the nation for qualified applicants. I firmly believe that applying to an Ivy based on their list price is the single biggest strategic blunder an applicant can make. People don't think about this enough, but a school with a massive endowment can give you a better deal than your local state flagship ever could.

The Concept of Demonstrated Financial Need

Every single one of the eight Ivy League institutions has committed to a policy known as meeting 100% of demonstrated financial need. This sounds like bureaucratic marketing fluff, except that it is backed by legal institutional mandates. They calculate what your family can theoretically afford using a complex, invasive financial auditing process called the CSS Profile. If their formula decides your family can only contribute $2,000, then that is all you pay, whether the official sticker price is $95,000 or a million bucks. That changes everything, doesn't it?

Decoding Net Price: The Real Cost by Income Bracket

To truly find the cheapest Ivy League option, we have to look directly at the income thresholds where parent contributions drop to zero. This is where the separation between the ultra-wealthy Ivies and their slightly less-endowed peers becomes a massive chasm. It is a game of financial brinkmanship played with billions of dollars. Experts disagree on minor logistical definitions of assets, but the hard lines drawn by financial aid offices tell an undeniable story.

The Zero-Parent-Contribution Thresholds

Princeton shattered the old financial aid paradigms by dictating that families earning up to $150,000 per year with typical assets pay absolutely nothing for tuition, room, or board. Read that twice. You get a completely free ride at one of the world's most prestigious universities if your household sits comfortably in the American upper-middle class. Harvard and Yale recently retaliated by expanding their own zero-contribution benchmarks to $100,000 for the 2026 academic cycle, up from previous limits. Meanwhile, Dartmouth College and Brown University have established their free tuition baselines around the $125,000 mark, which sounds incredibly generous until you realize it only covers tuition, leaving you on the hook for thousands in room and board. See the subtle difference?

Middle-Income Aid Dynamics and the Sliding Scale

But what happens if your family earns more than the magic zero-dollar threshold? This is where it gets incredibly messy because the taper rate varies wildly between Ithaca, New York, and Cambridge, Massachusetts. At Harvard, families making between $100,000 and $150,000 are expected to contribute a sliding scale of 0% to 10% of their total annual income. In contrast, Cornell University, which handles the largest undergraduate student body of the group (over 15,000 undergrads), has to stretch its endowment much thinner. Consequently, a family earning $140,000 will likely face a significantly higher net price package at Cornell than they would at Yale or Princeton, which explains why the net price calculator is your only real friend in this journey.

The No-Loan Policy Revolution

We are far from the days when graduating from an elite institution meant carrying a secondary mortgage worth of debt on your back. The introduction of the no-loan financial aid package changed the entire landscape of American higher education permanently. But do not mistake this for pure altruism; it is a cutthroat customer acquisition strategy designed to steal top-tier talent away from Stanford and MIT.

How No-Loan Policies Actually Work

When a university says they have a no-loan policy, it means your financial aid award contains strictly institutional grants—which are essentially free money that never needs to be repaid—alongside a minor federal work-study component. Harvard, Princeton, Yale, and Penn have completely eliminated student loans from their financial aid equations for all admitted undergraduate students who qualify for aid. But wait, here is the catch that nobody warns you about: if your calculated parent contribution is $15,000, and you do not have that cash sitting in a checking account, you might still have to take out private loans to bridge the gap. The university did not include a loan in your financial package, yet you ended up with debt anyway. It is a masterful piece of semantic misdirection that leaves many families feeling blindsided when the actual bill arrives in August.

Comparing the True Costs of the Big Three vs. The Rest

If we are forced to declare a definitive winner in the battle of affordability, we must look at the structural divide between the "Big Three" (Harvard, Yale, Princeton) and the remaining five members of the ancient athletic conference. The financial gap is real, measurable, and highly consequential for your wallet.

The Financial Dominance of Princeton, Harvard, and Yale

Because Princeton has the highest endowment-per-student ratio in the entire world, they can consistently offer the most aggressive aid. Their average annual net price for students receiving financial aid hovers around an astonishing $18,685, which is cheaper than attending an in-state public university in many parts of New Jersey or Pennsylvania. Harvard is right there in the trenches with an average net price of roughly $18,037 after grants are factored in. Honestly, it's unclear down to the exact dollar which one wins on any given day because your family's unique asset mix (like owning a small business or a home in an expensive zip code) will shift the calculations drastically. Yet, the overarching rule remains absolute: the historical prestige of HYP comes with the deepest pockets.

The Disadvantage of the Lower-Endowment Ivies

At the other end of the spectrum, you have institutions like Columbia University and the University of Pennsylvania. Do not get me wrong; they are extraordinarily wealthy corporations compared to almost any other school on Earth, except that they operate in expensive urban environments and possess smaller endowments relative to their student enrollments. Columbia's base cost of attendance for 2025-2026 neared $96,260 once New York City living expenses were tacked on. While they meet full need, their formulas for what constitutes a "typical asset" tend to be noticeably more stringent than Princeton's. Hence, a middle-class family will almost always find themselves paying a few thousand dollars more per year to walk across the quad in Upper Manhattan than they would to stroll through the gothic arches of New Haven.

Common Myths Surrounding Ivy League Affordability

The Sticker Price Illusion

You stare at the published cost of attendance and your jaw drops. Rightly so, because crossing the $90,000 annual threshold feels like buying a luxury sports car every twelve months. But here is the twist: nobody with financial need actually pays that sum. Families panic when they see Dartmouth or Brown listed among the priciest institutions on Earth, yet these universities operate on a completely different financial plane than standard state schools. The problem is that baseline advertising focuses entirely on the gross cost, which scares away brilliant applicants from low-income brackets before they even look at the net price calculators.

The Merit Scholarship Mirage

Let's be clear: you will not receive a sports scholarship at Harvard, nor will Yale hand you a cash prize for your flawless SAT score. A widespread misconception assumes that being the valedictorian unlocks institutional merit aid within this elite circle. It does not. The Ancient Eight banned merit-based awards decades ago to maintain a level playing field among admitted overachievers. Every single penny distributed comes strictly through need-based analysis. If your household pulls in a massive corporate revenue, you pay full freight, regardless of whether you invented a new form of renewable energy in your garage.

The Uniform Financial Aid Package Fallacy

Assuming that all elite institutions calculate your family contribution identically is a massive blunder. Ivy League schools use the Institutional Methodology to dissect your assets, which explains why your expected family contribution can swing by $10,000 between Princeton and Columbia. One campus might heavily weigh your home equity, while another completely ignores it. As a result: a family earning $130,000 might find one university vastly superior in generosity compared to its direct rival up north.

The Hidden Lever: Asset Treatment and the True Path to Cheap Ivy Education

How Intangible Wealth Dictates Which Ivy League is the Cheapest

Everyone talks about income brackets, yet the real battleground for affordability happens deep within the asset ledger. Princeton famously stands out because it completely excludes primary home equity from its financial aid calculations. If your parents bought a modest home in California thirty years ago that skyrocketed in value, Columbia or Penn might expect your family to borrow against that paper wealth. Princeton shrugs it off. This specific policy variance is often the deciding factor when determining which Ivy League is the cheapest for middle-class homeowners who are asset-rich but cash-poor.

Consider the profound impact of institutional endowment size per student. Harvard and Yale sit on mountains of capital that allow them to absorb unusual financial circumstances without blinking. Did your family face massive, uninsured medical bills last year? The wealthier endowments possess the bureaucratic flexibility to write off those expenses during a financial aid appeal. The issue remains that smaller-endowment Ivies simply lack the liquidity to be quite as loose with their discretionary fee waivers, making the ultra-wealthy trio the structural champions of radical affordability.

Frequently Asked Questions

Which Ivy League is the cheapest for families earning under 0,000?

Princeton University claims the crown for this specific demographic by eliminating the parent contribution entirely for families with typical assets earning below $100,000. Under this aggressive framework, qualifying students receive full coverage for tuition, room, board, and miscellaneous personal expenses. Harvard follows a nearly identical model, requiring a zero-dollar contribution from families making under $85,000, while scaling up gently for households making slightly more. Data shows that which Ivy League is the cheapest relies heavily on these specific income cutoffs, where Princeton's generous $100,000 threshold currently leads the pack. Consequently, approximately 25 percent of Princeton undergraduates pay absolutely nothing to attend.

Can international students benefit from these generous financial aid policies?

Only a select group of five Ivy League institutions extend full need-blind admission policies alongside comprehensive financial aid to international applicants. Harvard, Princeton, Yale, Dartmouth, and Bowdoin (a non-Ivy clone in policy) guarantee to meet 100 percent of demonstrated need for global students without letting their financial status harm their admissions chances. The remaining campuses, including Penn and Cornell, practice need-aware admissions for international students, meaning asking for money can actively tank your acceptance probability. Are you willing to gamble your admission chances just to compare aid packages? This creates a massive divide where the wealthiest trio remains the most viable option for low-income international scholars looking for zero-loan guarantees.

How do Ivy League costs compare to top-tier public universities for out-of-state students?

An out-of-state student attending UC Berkeley or the University of Michigan will often pay significantly more than they would at an elite private institution. Public universities rarely offer substantial need-based aid to non-resident students, pushing the annual out-of-state cost past $75,000 with very few institutional discounts available. Conversely, because which Ivy League is the cheapest depends on massive endowments rather than state tax allocations, low-to-middle-income students routinely find Ivy packages cheaper than their local state flagship. In fact, families earning under $150,000 usually pay a fraction of the price at Yale compared to what a typical out-of-state public university would demand through federal Parent PLUS loans.

The Verdict on Elite Affordability

Stop looking at the sticker price because it represents a fictional boogeyman designed for billionaires. The data screams a clear truth: Princeton consistently edges out its peers as the most financially generous institution for the vast majority of working and middle-class families. We must discard the archaic notion that elite education is inherently an exclusionary financial trap. Except that you must be proactive, run the net price calculators early, and refuse to let baseline tuition figures dictate your academic destiny. In short: the wealthiest schools have turned prestige into a surprisingly affordable commodity, provided you can clear the astronomical hurdle of getting accepted.