The Analyst Identity: More Than Just a Entry-Level Title

People don't think about this enough, but the Analyst role isn't actually a "junior" version of what the Partners do. It is a completely different species of labor altogether. If a Managing Director is the architect of a bridge, the Analyst is the person counting every single rivet while hanging over a thousand-foot drop in a windstorm. In the private equity food chain, the hierarchy is rigid, almost Victorian in its discipline. You sit at the very base. But because these firms are often leaner than the massive bulge-bracket banks—sometimes employing fewer than 30 investment professionals—your "lowest" position still places you in rooms where the internal rate of return (IRR) on a 500 million dollar leveraged buyout is the only thing that matters. That changes everything about the pressure you feel on a Tuesday at 3:00 AM.

The Disconnect Between Glamour and Grunt Work

There is a persistent myth that private equity Analysts spend their days drinking expensive scotch and debating the merits of corporate strategy with CEOs. We're far from it. The actual day-to-day involves a relentless, almost numbing amount of data scrubbing and "cleanup" on target companies that have messy financial records. Honestly, it's unclear why some firms still insist on putting 22-year-olds through this specific brand of psychological warfare, but the industry consensus is that if you haven't bled over a waterfall calculation, you don't deserve to participate in the carry. The issue remains that the prestige of the "Buy Side" acts as a magnet, drawing in thousands of applicants for a handful of seats at firms like Blackstone, KKR, or Apollo. You aren't just an employee; you are an expensive, highly-calibrated piece of human software designed to find errors in a Three-Statement Model.

Deconstructing the Technical Gauntlet: What You Actually Do

The core of the lowest position in private equity revolves around the LBO (Leveraged Buyout) model. This is your lifeblood. You will spend months—yes, months—staring at a single Excel workbook until you can see the formulas when you close your eyes. Which explains why the burnout rate is so high. Yet, the technical mastery required at the Analyst level is staggering; you must understand debt schedules, PIK (Payment-in-Kind) interest, and complex tax structures better than the people actually signing the checks. Did you know that a single-cell error in a debt-scoping model can lead to a 50-basis-point swing in the projected return? That is the kind of mistake that gets you "managed out" before your first bonus cycle. And because the stakes are so high, the scrutiny is absolute.

Mastering the Art of Due Diligence

When a firm considers buying a company, the Analyst is the one who dives into the Virtual Data Room (VDR) to hunt for skeletons. This isn't just checking math. You are looking for customer concentration risks, analyzing EBITDA add-backs that look suspiciously like aggressive accounting, and coordinating with third-party consultants. It is a grind. But—and here is the sharp opinion most won't tell you—this "grunt work" is actually where the real investing is learned. While the Partners are out playing golf or networking with pension fund managers, the Analyst is the only person who truly knows the target company's unit economics. Experts disagree on whether this level of micro-management is necessary for growth, but in the trenches of a mid-market fund in Chicago or London, it is the only way to survive the investment committee meetings.

The "Point-One" Error Culture

Precision is not a suggestion; it is the currency of the realm. If you present a slide to a Principal and a decimal point is misplaced, your credibility evaporates instantly. This sounds like an exaggeration, right? It isn't. The lowest position in private equity requires a level of perfectionism that borders on the pathological because the entire business model is predicated on the efficient use of capital. Every dollar of dry powder—the unallocated capital a fund has—needs to be deployed with surgical accuracy. Hence, the "zero-error" mandate. It’s a brutal way to live, but it’s how the industry maintains its edge over the public markets.

The Economics of the Bottom Tier: Compensation and Costs

Let’s talk about the money, because that’s why anyone subjects themselves to this. A first-year Analyst at a top-tier private equity firm in 2026 can expect a base salary ranging from 120,000 to 150,000 dollars, with a bonus that can effectively double that figure. As a result: the Total Cash Compensation (TCC) for the lowest person on the totem pole often exceeds what a senior manager makes in almost any other industry. But where it gets tricky is the hourly rate. If you are working 100 hours a week, 50 weeks a year, that 250,000 dollar package suddenly looks a lot less impressive when compared to a software engineer at a FAANG company who logs off at 5:00 PM. I believe the trade-off is only worth it if you view those two years as an ultra-expensive, paid PhD in corporate finance. Otherwise, you’re just a very well-paid transcriptionist for spreadsheets.

The Bonus Trap and the Carry Dream

Most Analysts don't get carried interest—the share of the profits that makes private equity partners fabulously wealthy. You are strictly a "cash" employee. But the carrot dangled in front of you is the promotion to Associate, where you might finally get a sliver of the upside. The thing is, many firms operate on an "up or out" basis. If you aren't the top performer in your Analyst cohort, you won't get that promotion; instead, you’ll be encouraged to head to a top-ten MBA program (think Harvard, Stanford, or Wharton) and try to fight your way back in later. This creates a hyper-competitive internal environment where your best friend at the desk next to you is also your biggest rival for a single promotion slot. Is it healthy? Probably not. Does it produce the most financially literate professionals on the planet? Absolutely.

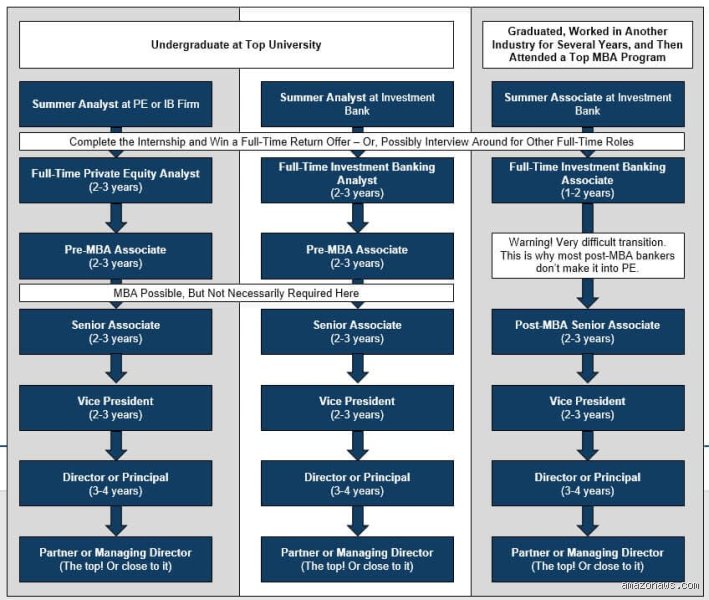

Hierarchy Hacks: Analyst vs. Associate vs. Intern

While the Analyst is technically the lowest full-time position, the Summer Intern is the true bottom of the ocean, though they are temporary. The jump from Analyst to Associate is the first major hurdle. In banking, an Associate might manage a group of Analysts, but in private equity, the lines are blurred. An Associate is expected to have "deal intuition," while the Analyst is expected to have "data mastery." The distinction is subtle but massive. An Analyst asks "How do I build this model?" while the Associate asks "Does this deal actually make sense for our fund's mandate?" Except that, in reality, both of them are usually just trying to finish the CIM (Confidential Information Memorandum) before the sun comes up. It’s a distinction of responsibility more than a distinction of labor.

The Regional Variations of Junior Roles

It is worth noting that the "lowest" role changes shape depending on where you are. In London’s Mayfair district, you might see "Junior Associate" used as the entry point for people coming straight out of undergraduate programs like LSE or Oxford. In the US, the Analyst program is more standardized. However, the rise of Growth Equity firms—which sit somewhere between Venture Capital and traditional PE—has introduced new titles like "Sourcing Analyst." These roles focus less on modeling and more on cold-calling founders. That is a different kind of hell. Imagine being a 22-year-old trying to convince a 50-year-old CEO of a successful manufacturing plant that they should sell 40 percent of their company to your firm. It requires a level of "hustle" that traditional LBO analysts often look down upon, yet it is increasingly becoming a common entry point into the sector.

The labyrinth of misconceptions surrounding the entry-level hierarchy

You probably think the lowest position in private equity is merely a stepping stone where high-fliers relax while capital multiplies. That is a fantasy. Many outsiders confuse the junior analyst role with a glorified internship, yet the reality involves a brutal initiation into fiscal architecture. The problem is that social media portrays these entry points as high-glamour networking hubs. It is actually a spreadsheet-driven purgatory. Let's be clear: you are not picking the companies; you are auditing the trash to find one gold coin. Because the stakes involve billions, the margin for error is effectively zero. A single mistyped cell in a discounted cash flow model can derail a deal, making the junior person the most stressed individual in the room.

The myth of the forty-hour work week

Young professionals often enter the fray believing they can balance a social life with leveraged buyout analysis. This is a comedic oversight. While the Vice President might leave at seven in the evening, the lowest position in private equity stays until the sun threatens to rise. Data suggests that first-year associates at mega-funds frequently clock 80 to 90 hours per week during active deal cycles. Is it sustainable for a human being? Hardly. Yet, the industry operates on this precise Darwinian filter. The issue remains that the workload is front-loaded onto the least experienced members of the team. As a result: the burnout rate for those in their first twenty-four months fluctuates between 15% and 25% depending on the fund’s assets under management.

The "Deal Maker" delusion

Another frequent error is the assumption that a private equity analyst spends their day in intense negotiations with CEOs. Except that your actual day consists of "cleaning" data in Excel and formatting PowerPoint decks. You are a digital janitor. You are not at the table; you are the one making sure the table is perfectly level and the documents on it have no typos. But the prestige attached to the firm name often blinds candidates to this clerical reality (which is quite ironic given the Ivy League tuition they paid). In short, the prestige is a trailing indicator, while the labor is a leading reality.

The hidden leverage of the lowest position in private equity

If you want to survive the pre-MBA associate gauntlet, you must master the art of the "shadow portfolio." Expert advice dictates that the most successful juniors don't just process what is given to them. They anticipate the questions of the Investment Committee before those questions are even whispered. This requires a level of intellectual aggression that most undergraduates simply do not possess. The problem is that technical skills are now a commodity. Everyone knows how to calculate a weighted average cost of capital. The true differentiator is your ability to interpret the narrative behind the numbers. Which explains why the most resilient analysts are often those with a background in liberal arts combined with a rigorous financial self-education, rather than pure finance majors who think in templates.

The power of the data room

Let's be clear about the value of being at the bottom. You are the only person who has actually read every single document in the virtual data room. This creates a temporary information asymmetry where the person in the lowest position in private equity actually knows more about the target company’s liabilities than the Senior Partner. If you leverage this correctly, you become the indispensable nervous system of the deal. The issue remains that most juniors are too terrified to speak up when they find a red flag. Success in this industry requires the audacity to tell a Managing Director that their favorite deal is a sinking ship based on a footnote in a lease agreement. That is where real careers are forged.

Private Equity Career FAQ

What is the typical starting salary for an entry-level analyst?

Total compensation for the lowest position in private equity varies wildly based on firm size and geography. In major hubs like New York or London, a first-year analyst at a top-tier firm can expect a base salary between $100,000 and $125,000. However, the performance bonus often ranges from 50% to 100% of that base, leading to a total package exceeding $200,000. Data from 2024 recruitment surveys indicates that total comp has risen by 8% annually to combat talent poaching from tech firms. This sounds lucrative, but when calculated against the hourly rate of a 90-hour week, the numbers lose their luster. As a result: the effective hourly wage is often comparable to that of a senior manager in a less volatile industry.

Can you enter private equity directly from undergraduate studies?

Historically, the path required two years in investment banking, yet the landscape is shifting toward direct-entry analyst programs. Firms like Blackstone and KKR have pioneered these tracks to capture elite talent before it gets "tainted" by the culture of sell-side banks. Competition is staggering, with some firms receiving over 2,000 applications for a single slot. The technical interview process is a grueling gauntlet of modeling tests and case studies designed to break your spirit. If you lack a 3.8 GPA and a relevant internship, your chances are statistically negligible. In short, while the door is open, the threshold is higher than it has ever been in financial history.

Is an MBA required to move up from the lowest position?

The "two-and-out" rule used to be the iron law of the industry, where associates were forced to leave for business school after two years. Today, many middle-market and even some mega-funds offer A-to-A promotions, which allow a direct leap from Associate to Senior Associate without a $200,000 degree. But the choice is often a gamble on your long-term carried interest potential. An MBA provides a safety net and a network that purely internal promotion cannot replicate. Which explains why roughly 60% of senior partners at the top 50 global firms still hold a degree from a top-three business school. The problem is that the opportunity cost of leaving the workforce for two years is now higher than it was a decade ago.

The unfiltered reality of the private equity grind

The lowest position in private equity is a high-stakes trade of your youth for a seat at the world's most exclusive table. We must admit that this trade is not for everyone, and frankly, it shouldn't be. You are essentially a human calculator with a premium brand name attached to your LinkedIn profile. The industry doesn't want your creativity; it wants your precision and your silence. Yet, if you can withstand the compounded stress and the isolation of the data room, the financial upside is unparalleled in any other legal profession. My stance is simple: don't do it for the money, because the money isn't enough to compensate for the lost sleep. Do it because you have a pathological obsession with how capital structures are built and destroyed. That is the only way to survive the bottom without losing your soul.