The Jurisdictional Maze: Why Some Pesos Are Born Free

The thing is, people don't think about this enough: taxability in our country isn't just about how much you make, but where you make it and what "flavor" that money carries. Our National Internal Revenue Code (NIRC) operates on a schedular system, meaning different types of earnings are shoved into different buckets, some of which have holes in the bottom specifically designed to let money leak back into your pocket. Why do we assume the government wants it all? Because the paperwork is intimidating, honestly, and the nuances are often buried under layers of legalese that even seasoned accountants argue over during lunch breaks.

The Citizen vs. The Non-Resident Struggle

Here is where it gets tricky. If you are a Resident Citizen, you are taxed on worldwide income, which sounds quite oppressive until you realize that Non-Resident Citizens—those working as OFWs in places like Dubai or Singapore—are only taxed on income derived from sources within the Philippines. This means their foreign earnings are entirely non-taxable locally. It is a massive carve-out. But is it fair? I believe this distinction is the bedrock of our modern economy, acting as a silent subsidy for the heroism of migrant workers. Without this exemption, the flow of remittances would likely stutter, yet we rarely discuss it as a "tax break." It is simply the status quo, which explains why so many families can afford to build homes in the provinces without the BIR knocking on their newly painted doors.

De Minimis and the Art of the Small Benefit

We often ignore the "small things" because they feel like crumbs, but in the Philippine tax landscape, these crumbs are De Minimis benefits. These are facilities or privileges of relatively small value offered by an employer to promote the health, goodwill, contentment, or efficiency of employees. They are not considered part of your basic salary. As a result: they aren't subject to withholding tax. Think of your rice subsidy (2,000 pesos per month) or your laundry allowance (300 pesos per month). It sounds like pocket change, yet when you aggregate these across a 1,000-employee firm in Makati, we're talking about millions of pesos in legally shielded wealth. The issue remains that many HR departments are too lazy to structure these properly, leaving employees to pay taxes on what should have been an exempt benefit.

The 90,000 Peso Ceiling You Cannot Ignore

The 13th-month pay and other benefits—including Christmas bonuses and productivity incentives—are exempt from tax, but only up to a threshold of 90,000 pesos. Exceed that by a single centavo and that specific portion gets dragged into your taxable income pile. This isn't just a suggestion; it is a hard ceiling that changed drastically when the TRAIN Law was implemented in 2018. Before that, the cap was a measly 82,000 pesos, and even earlier, it was stuck at 30,000 pesos for decades (a timeframe where inflation basically turned that exemption into a joke). Have you checked your December payslip lately? If your total bonuses hit 95,000 pesos, only the 5,000-peso excess is taxed at your marginal rate, which is a nuance that confuses the life out of most people.

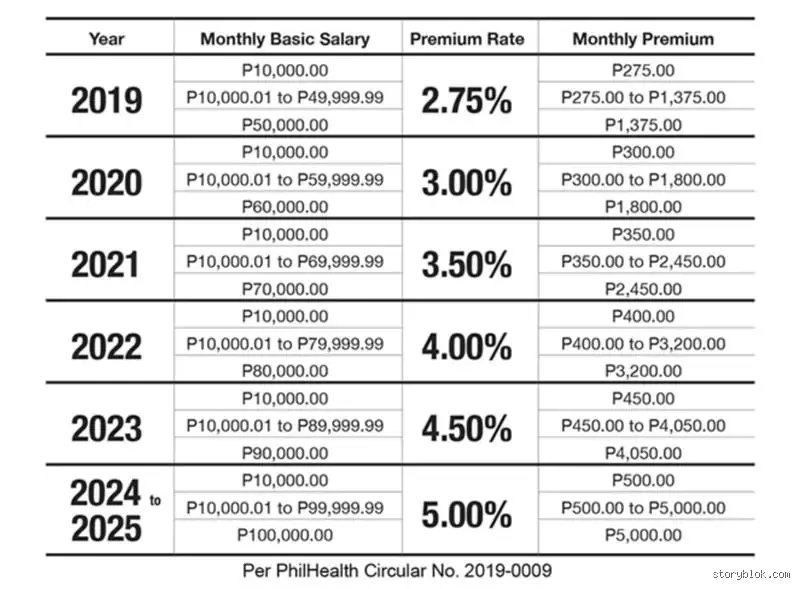

The Sanctuary of Social Security and Insurance

Mandatory contributions are the unsung heroes of your net pay. Your SSS, GSIS, PhilHealth, and Pag-IBIG contributions are deducted from your gross income before the tax calculation even begins. Furthermore, the benefits you receive from these institutions—like a maternity leave benefit or a disability pension—are 100% tax-exempt. Because the law views these as social safety nets rather than "profit," they remain sacrosanct. This applies to life insurance proceeds too. When a beneficiary receives a payout after a loved one passes away, the BIR does not view that as taxable income; it is considered a return of capital or a compensatory payment for loss, which changes everything for a grieving family trying to find their financial footing.

Statutory Exemptions: When the Law Plays Favorites

Passive income usually gets hit with a 20% final withholding tax, but there are loopholes wide enough to drive a jeepney through if you know where to look. For instance, interest income earned from long-term deposits or investments (with a maturity of five years or more) is completely exempt for individual taxpayers. If you park your money in a five-year Time Deposit at a local bank like BDO or Metrobank, you keep every bit of interest. But—and there is always a "but"—if you pre-terminate that investment in the fourth year, the bank is required to claw back a portion of that tax. It’s a game of patience. Most people are too impatient to wait half a decade, hence the government rarely loses much revenue on this front.

Prizes, Awards, and the Myth of the "Free" Win

We love a good success story, especially when it involves an Olympic gold medalist or a local hero. Under the NIRC, prizes and awards made primarily in recognition of religious, charitable, scientific, educational, artistic, literary, or civic achievement are non-taxable. But there is a catch: the recipient must have been selected without any action on their part to enter the contest, and they must not be required to render substantial future services. If you win a raffle at the mall, you’re paying 20%. If you win a Nobel Prize or a government-sanctioned award for heroism, you keep the lot. It is a distinction that feels arbitrary until you realize the law is trying to separate "luck" from "merit," though experts disagree on whether a lottery win should be treated more harshly than a scientific breakthrough.

The Minimum Wage Earner’s Shield

Let’s be blunt: Statutory Minimum Wage Earners (SMWE) are the most protected class in the Philippine tax code. Their basic wage is exempt. Their holiday pay is exempt. Their overtime pay, night shift differential, and hazard pay? Also exempt. This is a massive departure from the old system where a little bit of overtime could ironically push a worker into a higher tax bracket and leave them with less take-home pay than if they hadn't worked the extra hours at all. We're far from a perfect system, but this specific protection ensures that those at the base of the economic pyramid aren't taxed into further poverty. It is a zero-rated existence that provides a slim but vital margin for survival in a high-inflation environment like Manila.

Retirement Pay: The Final Tax-Free Hurrah

Retirement is the ultimate goal, and the tax code gives you one last parting gift if you play your cards right. Retirement benefits received under Republic Act No. 7641 or those received by officials and employees of private firms in accordance with a reasonable private benefit plan maintained by the employer are exempt. However, the requirements are strict: you must be at least 50 years old and have served that same employer for at least 10 years. And you can only avail of this tax-free retirement once in a lifetime. You can't hop from one company to another, collecting tax-free retirement checks every decade; the BIR tracks this with the tenacity of a bloodhound because, let’s face it, that would be a legendary loophole.

Common Pitfalls and the Myth of Universal Exemption

The Deceptive Allure of Gross Compensation

You might assume that because your paycheck feels light, the Bureau of Internal Revenue is ignoring your side hustles or specific allowances. The problem is that many taxpayers conflate de minimis benefits with substantial salary components. Let’s be clear: once those small perks for "health, goodwill, and efficiency" exceed the strict thresholds set by the Department of Finance, they transform into taxable compensation. If your rice subsidy climbs past 2,500 Pesos per month, the surplus becomes part of your 90,000 Peso ceiling for 13th-month pay and other benefits. But wait, what happens when you hit that 90,000 limit? Every single centavo beyond that threshold is sucked into the taxable whirlpool regardless of how much you need it for rent. You cannot simply label a large bonus as "hazard pay" to dodge the taxman because the law demands specific sector-based qualifications for such exemptions.

Misunderstanding the Passive Income Trap

Many Filipinos believe that all "gifts" are exempt from the standard income tax regime, which is technically true but practically misleading. Except that the Donor’s Tax exists to catch what the income tax misses. If you receive a property or a significant cash windfall exceeding 250,000 Pesos within a calendar year, you aren't paying income tax, yet you are likely liable for a 6% donor’s tax. It is a common misconception to think "non-taxable" means "no paperwork required." In short, failing to report these transactions can lead to surcharges that make the original tax look like pocket change. We often see people forgetting that interest income from long-term deposits is only exempt if held for at least five years. Pull that money out at four years and eleven months? As a result: you are slapped with a 20% final withholding tax immediately.

The Strategic Edge: Leveraging Statutory Exclusions

Maximizing Personal Equity and Retirement Account (PERA) Contributions

Wealth preservation is not just about earning more; it is about keeping what you already have through the Personal Equity and Retirement Account Act. While most employees focus on their basic SSS or GSIS contributions, the PERA provides a 5% tax credit on contributions up to 200,000 Pesos for locally employed individuals. Overseas Filipino Workers get double that capacity. The issue remains that the Philippines has a very low adoption rate for this vehicle. Why would you leave money on the table when the investment income earned within the PERA remains completely exempt from all taxes? (And yes, that includes the 20% final tax on interest and the 10% dividend tax). It is perhaps the most underutilized tool in the entire Philippine tax code for building a nest egg that the government cannot touch upon withdrawal at age 55.

Frequently Asked Questions

Is the income of an Overseas Filipino Worker (OFW) entirely tax-exempt?

Yes, but specifically for income derived from sources outside the Philippines as per the National Internal Revenue Code. If an OFW operates a business or owns a rental property within Philippine borders, that specific local income remains subject to the standard 20% to 35% graduated rates. The data shows that while the foreign-sourced earnings of over 1.8 million OFWs are protected, many run into trouble by not registering their local side-businesses properly. You must maintain proof of your overseas employment to satisfy BIR auditors if they question your sudden influx of capital. In short, your physical absence from the country secures the exemption for your foreign salary but offers no shield for your local investments.

Are separation pay and terminal leave pay taxable in all circumstances?

The taxability of separation pay hinges entirely on the voluntariness of the severance. If you are laid off due to retrenchment, redundancy, or a terminal illness, the entire amount is exempt from income tax regardless of the total figure. However, if you resign voluntarily to pursue a better opportunity, your terminal leave pay is treated as part of your gross compensation. Which explains why terminal leave pay for government employees is handled differently than in the private sector, often enjoying broader exemptions under specific judicial rulings. You should ensure the employer files the necessary BIR certification for "involuntary separation" to keep your hard-earned payout intact.

What happens to the tax status of 13th-month pay if it exceeds 90,000 Pesos?

The law provides a very specific 90,000 Peso ceiling for the total of your 13th-month pay and other benefits like productivity incentives. If your total "other benefits" reach 100,000 Pesos, the 10,000 Peso excess is simply added to your taxable income for the year. This means it will be taxed at your applicable marginal rate, which could be as high as 35% for high earners. Because this threshold is static and not indexed to inflation annually, more middle-class earners find themselves crossing this limit every year. As a result: your "non-taxable" bonus is often smaller than the gross amount promised in your contract once the accounting department finishes its year-end computations.

The Final Verdict on Tax-Free Earnings

Navigating what income is not taxable in the Philippines is not a pursuit for the lazy or the uninformed. We must stop viewing the BIR as a monolith that takes everything and start seeing the tax code as a set of rigid boundaries that actually protect certain assets. Let's be clear: the 90,000 Peso exemption and the OFW status are the strongest shields available to the average Filipino. It is frankly ironic that people spend hours complaining about high VAT while ignoring the legal loopholes like PERA contributions or the five-year long-term deposit rules. My stance is simple: if you aren't actively structuring your income to meet these exemptions, you are effectively volunteering to pay a "cluelessness tax." We cannot expect the government to point out every saving opportunity for us. The burden of financial literacy sits squarely on your shoulders, and the rewards for carrying that weight are measured in thousands of Pesos saved annually.