The Evolution of Wealth Tiers: Shifting Beyond the Millionaire Next Door

Wealth is a moving target. Decades ago, having seven figures meant you had arrived, but inflation, global asset bubbles, and the explosive growth of tech equity have severely diluted that old benchmark. Honestly, it's unclear where the middle class ends and true affluence begins anymore, but $100 million leaves no room for ambiguity. The financial industry classifies anyone with $1 million in investable assets as a High Net Worth Individual (HNWI). But let's be real: in cities like New York or London, a couple of million dollars just buys a nice two-bedroom apartment and a comfortable retirement. That changes everything when we look at the actual data. If you scale up to $30 million, you enter the Ultra High Net Worth territory, which explains why the financial elite needed a new term for the nine-figure club.

Enter the Centimillionaire Era

The term centimillionaire has become the definitive marker for this specific class of capital. According to the 2024 Henley Global Citizens Report, there are only around 29,300 people worldwide who hit this mark. Think about that for a second. In a world of eight billion people, this group is an statistical anomaly. I believe we look at wealth backward by focusing on millionaires, when the real shift in societal influence happens precisely when you cross into the nine-figure zone. It is a club populated by founders who executed massive liquidity events, hedge fund partners, and families who have successfully preserved multi-generational dynasties through sophisticated estate planning.

What Does 0 Million Look Like? The Anatomy of Nine-Figure Purchasing Power

Where it gets tricky is understanding how this money behaves in the wild. A net worth of $100 million behaves nothing like a regular bank account. If you follow a conservative 4% withdrawal rule, this fortune spits out $4 million in annual income without ever touching the principal. People don't think about this enough: at this level, your money makes more money than most CEOs earn through actual labor. But how is that capital deployed? It isn't sitting in a checking account; instead, it is highly illiquid, tied up in private equity, commercial real estate, and sophisticated derivative strategies designed to hedge against market downturns.

The Realities of the Nine-Figure Lifestyle

Let's look at a concrete example. Imagine an investor named David who sold his logistics company in Chicago in 2025. After paying the capital gains tax, he walks away with exactly $100 million. If he buys a $15 million penthouse in Miami and a $25 million superyacht, he has already burned through 40% of his capital. The issue remains that maintenance costs for luxury assets—often pegged at 10% of the purchase price annually—will rapidly erode his remaining cash. That is why smart centimillionaires operate differently. They treat their wealth like a corporation. They don't buy yachts; they charter them through corporate structures to write off the expenses against their investment income.

The Burden of Asset Protection

Wealth shields you from regular bills, yet it exposes you to an entirely different class of threats. When your name shows up on public wealth registries, you become a walking target for frivolous lawsuits, complex tax audits, and extortion. As a result: security ceases to be a luxury and becomes an operational line item. This involves hiring specialized legal counsel, setting up asset-protection trusts in jurisdictions like South Dakota or the Cayman Islands, and implementing military-grade cybersecurity for family members. You aren't just managing money anymore; you are governing an institution.

Family Offices and the Institutionalization of Personal Fortune

When assessing if $100 million qualifies as high net worth, the defining operational threshold is whether you require a single-family office. This is where conventional retail banking stops and bespoke institutional management begins. A single-family office is a dedicated company whose sole mission is to manage the financial and personal affairs of one wealthy clan. Historically, the rule of thumb was that you needed at least $100 million to justify the overhead of hiring your own dedicated team of attorneys, accountants, and investment analysts. But today, because of rising compliance costs, that barrier has crept closer to $250 million, forcing many nine-figure families into multi-family offices instead.

The Mechanics of Wealth Preservation

Why do you need an army of professionals? Because the math of preserving $100 million across generations is brutal. Inflation eats away at purchasing power, while taxes threaten to chop off huge percentages every time assets pass to heirs. The primary objective shifts from aggressive growth to aggressive preservation. Portfolio managers at this level aren't chasing the hot stock of the week; they are looking for uncorrelated assets, such as forestry land, private credit, and venture capital allocations that can survive a systemic market meltdown.

How 0 Million Compares to Other Wealth Brackets

To truly grasp this scale, we need to contrast it with surrounding tiers. A family with $5 million is wealthy by any reasonable metric, but they are still vulnerable to black swan events like catastrophic medical crises or severe market crashes. They still worry about tuition fees and interest rates. But at $100 million? We're far from it. Those daily financial anxieties completely evaporate, replaced by macroeconomic concerns like global currency fluctuations and sovereign tax policy changes. Yet, if you compare a centimillionaire to a billionaire like Elon Musk or Jeff Bezos, the gap is still yawningly wide. A billionaire can lose $100 million on a bad weekend investment and barely notice it on their balance sheet.

The Relative Nature of Affluence

Context dictates everything. If you live in a rural community in the Midwest, $100 million makes you the most powerful economic force in the region. You could buy up main street, fund local hospitals, and dictate local politics. Except that if you move that same fortune to Monaco or the billionaires' row in Aspen, you suddenly look quite ordinary. You might find yourself berthing your modest 130-foot vessel next to a Russian oligarch’s 400-foot megayacht, feeling oddly middle-class in a playground designed for the hyper-rich. Wealth is entirely relative, which is why the psychological pursuit of the next tier never truly stops, even when the numbers defy human imagination.

Common Misconceptions Surrounding Ultra-High Net Worth Status

The Illusion of Infinite Liquidity

You see the nine-figure digit and assume cash flows like an open hydrant. The problem is that wealth at this scale rarely sits in a checking account. Imagine owning a dominant regional logistics enterprise valued at ninety million dollars. Your paper valuation screams elite status, yet your actual checking account holds a relatively modest three hundred thousand dollars. Liquidating those shares to buy a superyacht triggers massive tax events and risks stripping you of corporate control. Let's be clear: paper wealth does not equal immediate purchasing power, which explains why many centi-millionaires frequently utilize complex debt structures just to fund daily luxury operations.

The Lifestyle Inflation Trap

Many assume a hundred million dollars guarantees permanent financial safety. Except that maintenance costs for mega-assets scale exponentially. A sixty-foot luxury vessel demands roughly ten percent of its purchase price annually in crew fees and upkeep. Toss in a multi-property global real estate portfolio across London, Aspen, and Miami, and suddenly your fixed yearly burn rate hits four million dollars. Because market downturns cut asset values ruthlessly, an aggressive lifestyle can erode this specific tier of wealth within two generations. Is $100 million a high net worth if your annual overhead forces you to sell assets during a recession? Hard investments require constant liquidity injection, making cash flow management an ongoing battle even for the ultra-wealthy.

The Hidden Machinery: Bespoke Sovereign Structuring

Why Standard Wealth Management Fails at Nine Figures

Once your capital crosses the fifty-million-dollar threshold, traditional retail private banking becomes entirely obsolete. You move squarely into the realm of single-family offices and bespoke sovereign wealth strategies. This is not about picking mutual funds; it is about aggressive jurisdictional engineering. Ultra-high net worth individuals use private placement life insurance (PPLI) to wrap global hedge fund investments, legally wiping out annual tax liabilities. (Wealthy families often treat tax avoidance as a competitive sport.) As a result: the focus shifts entirely from generating market-beating returns to erecting impenetrable asset protection fortresses. True financial titans at this tier care less about gaining another five percent and far more about shielding their core empire from frivolous litigation, political instability, and aggressive global tax authorities.

Frequently Asked Questions

How many individuals worldwide actually possess a net worth of 0 million or more?

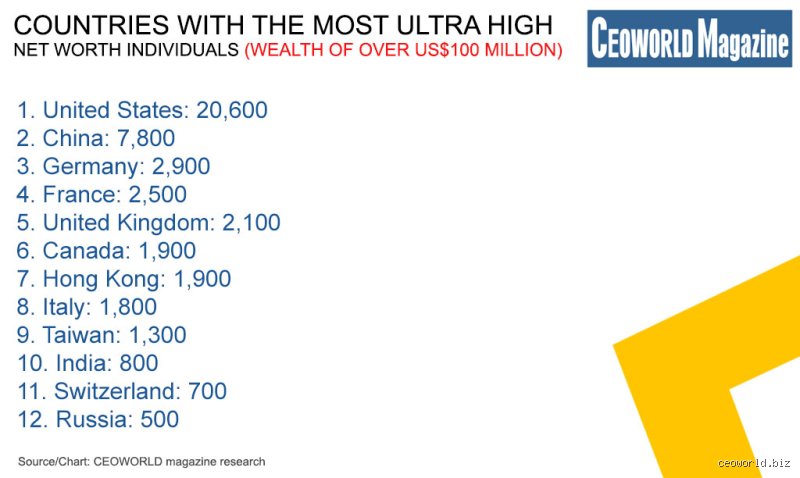

Data from global wealth intelligence firms indicates that roughly twenty-nine thousand individuals globally have achieved centi-millionaire status. This rarefied group represents a mere fraction of the broader millionaire population, anchoring them in the top 0.001 percent of global wealth holders. The United States claims the lion's share of this demographic, hosting over twelve thousand of these ultra-wealthy residents. Mainland China and the United Kingdom follow as distant runners-up in total concentrations. Therefore, when evaluating if is $100 million a high net worth, the global data confirms it places you in an extraordinarily exclusive economic elite.

Can a 0 million fortune withstand multiple generations without active business income?

Statistically, ninety percent of wealthy families see their entire fortune vanish by the third generation. Without active corporate revenue, a hundred-million-dollar pool exposed to a standard four percent annual inflationary drain and wealth fragmentation among heirs depletes rapidly. If an original patriarch leaves the money to four children, who then pass it to twelve grandchildren, the individual capital pools shrink significantly. Furthermore, bad investment decisions and estate taxes ranging up to forty percent in major economies can easily decimate the remaining principal. Success requires shifting from an entrepreneurial growth mindset to an institutional preservation strategy managed by dedicated professionals.

What does a typical asset allocation look like for an individual with a 0 million net worth?

Institutional family offices typically allocate roughly twenty-five percent of their total capital into private equity investments. Real estate holdings usually command another twenty percent, focusing heavily on prime commercial properties and multi-family residential complexes. Public equities receive a twenty-five percent allocation, while hedge funds and venture capital capture approximately fifteen percent of the remaining portfolio. The final slice rests in liquid cash equivalents and physical tangible assets like fine art or precious metals. This diversified framework ensures steady yield generation while buffering the core fortune against catastrophic macroeconomic collapses.

A Definitive Verdict on Nine-Figure Wealth

Let us cast aside the academic debates and state the reality plainly: a nine-figure fortune represents unadulterated economic power. To question its magnitude is pure financial cynicism, yet we must acknowledge its inherent vulnerabilities. This tier of capital transforms money from a mere medium of exchange into a complex geopolitical instrument. It buys supreme geographic mobility, unparalleled systemic leverage, and the ability to influence markets directly. Yet, the issue remains that wealth is never static; it is either actively defended or it slowly decays. We firmly believe that while a hundred million dollars secures absolute personal freedom, maintaining it requires treating the money itself as a full-time enterprise. In short, it is an undeniable fortune, provided you do not mistake paper valuation for financial immortality.