The Semantic Trap of Safety and Defining What Investment Has No Risk Actually Means

People don't think about this enough, but the word "risk" is a linguistic chameleon that changes colors depending on who is looking at it. To a retiree, risk is the terrifying prospect of a 20% market dip in October; to a hedge fund manager, risk is merely the standard deviation of historical returns. When we ask what investment has no risk, we are usually searching for nominal price stability, which is the comfort of knowing that if you put $1,000 into a box today, you will see $1,000 when you open it tomorrow. But the thing is, even that box has a cost. If the price of bread doubles while your money sits in that "safe" box, you have actually lost half your wealth without ever seeing a red candle on a chart. It is a subtle, creeping theft.

The Inflationary Tax on Stagnant Capital

Let's get real for a second. Is a mattress full of hundred-dollar bills a zero-risk investment? Hardly. While you avoid the volatility of the S&P 500, you are guaranteed to lose value over any significant time horizon due to the Consumer Price Index (CPI) trends. In 2022, for example, the US inflation rate spiked to 9.1%, meaning anyone holding "safe" cash effectively took a nearly 10% haircut on their buying power. This is the nuance that many traditional advisors gloss over because it's easier to sell a "low-risk" bond fund than to explain the complex decay of the dollar. And that changes everything when you realize that "safety" is often just a slow-motion disaster.

The Sovereignty Paradox and Credit Risk

We often point to U.S. Treasury Bills (T-Bills) as the ultimate answer to what investment has no risk because they are backed by the "full faith and credit" of the United States government. This assumes the government will always have the ability to tax its citizens or print more currency to meet its obligations. Yet, the issue remains that even the most stable empires face fiscal headwinds. Remember the 2011 S&P downgrade of U.S. debt? It was a wake-up call that sent shockwaves through the Treasury market, proving that even the foundations of global finance have cracks. Honestly, it's unclear if we can maintain this level of debt indefinitely without some form of structural adjustment, which explains why "risk-free" is a relative term, not an absolute one.

Deconstructing the Technical Mechanics of "Risk-Free" Government Assets

When the Federal Reserve adjusts the federal funds rate, currently sitting in the 5.25% to 5.50% range as of early 2024, the ripple effects redefine the landscape of what investment has no risk for the average Joe. You might look at a Certificate of Deposit (CD) offering 5% and think you've found the holy grail of finance. But where it gets tricky is the liquidity lock-up. If you need that money for a medical emergency but it's tied up in a 24-month term, the "risk" manifests as a penalty fee or the inability to capitalize on a better opportunity. We are far from a world where you can have high returns, instant liquidity, and zero volatility all at once.

The Role of the FDIC in Creating Synthetic Certainty

The Federal Deposit Insurance Corporation is the primary reason Americans feel comfortable sleeping at night with their money in a checking account. By insuring deposits up to $250,000 per depositor, per insured bank, the government creates a safety net that effectively removes the risk of bank runs for the middle class. Yet, this insurance is only as strong as the legislative will to fund it. During the Silicon Valley Bank collapse in March 2023, the government had to step in with extraordinary measures to prevent a systemic meltdown. Was the investment in those accounts "no risk" before the intervention? Only because the regulators decided, in the heat of the moment, to change the rules of the game to favor the depositors.

Series I Savings Bonds and the Inflation Hedge

I believe the Series I Savings Bond is perhaps the most honest attempt at a zero-risk instrument for the retail investor. It combines a fixed rate with a variable inflation rate that adjusts every six months. Because the principal value cannot decline, it offers a unique protection against the very inflation risk I mentioned earlier. But—and there is always a "but" in finance—you are limited to a $10,000 annual purchase. This cap makes it an irrelevant tool for institutional players or high-net-worth individuals, which highlights a recurring theme: true safety is often rationed or hidden behind red tape.

The Opportunity Cost of Playing It Too Safe

The obsession with finding what investment has no risk often leads to a phenomenon known as cash drag. If you had invested $10,000 in the Nasdaq-100 at the start of 2023, you would have seen a return of over 50% by the end of the year, whereas a "safe" money market fund would have netted you a modest 4% to 5%. As a result: by choosing the path of no risk, you are actively choosing the risk of underperforming the market so significantly that you can never actually retire. It is the ultimate irony of modern finance.

Volatility is Not the Enemy

Why do we fear a 5% drop in a stock price more than a 5% loss in purchasing power over three years? The human brain is wired to react to immediate volatility (the tiger in the bushes) rather than gradual decay (the slow leak in the water tank). But volatility is often just the price of admission for long-term growth. When you strip away the noise, the search for what investment has no risk is frequently a search for emotional comfort rather than mathematical efficiency. We crave the flat line on the graph, ignoring that a flat line in biology usually means the patient is dead.

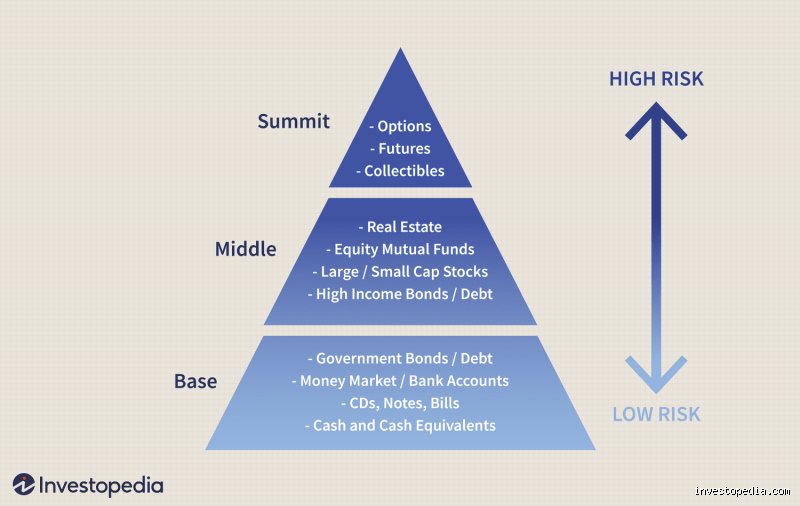

Standard Deviation vs. Permanent Loss of Capital

It is helpful to distinguish between "price risk" and "business risk." A share of a blue-chip company like Microsoft or Berkshire Hathaway might fluctuate wildly in price during a week of earnings reports, but the underlying business remains a cash-generating machine. On the other hand, a speculative "no-name" crypto token might have zero volatility for months because no one is trading it, only to go to zero overnight. In short, the absence of movement does not equal the absence of danger. You have to look at the underlying mechanics of how the value is generated—or if it is generated at all.

Comparing High-Yield Savings Accounts to Money Market Mutual Funds

In the current high-interest-rate environment, the battle for the title of what investment has no risk often comes down to these two contenders. A High-Yield Savings Account (HYSA) is a direct liability of the bank, whereas a Money Market Mutual Fund (MMMF) is a pool of short-term debt instruments like commercial paper and Treasury bills. One is insured by the FDIC; the other is not. Which explains why, during periods of extreme stress, investors flee the latter for the former, even if the yield on the fund is slightly higher. But does the average person understand the difference? Probably not, and that lack of understanding is a risk in itself.

The Breaking of the Buck

There is a rare but terrifying event in the world of money market funds known as "breaking the buck," where the Net Asset Value (NAV) falls below $1.00. This happened to the Primary Reserve Fund during the 2008 Financial Crisis following the Lehman Brothers collapse. Suddenly, an investment that was perceived to have no risk was returning 97 cents on the dollar. It was a glitch in the Matrix of safe investing. While regulations have tightened significantly since then to prevent a recurrence, the historical precedent serves as a grim reminder that "stable" is a temporary state of being.

Yield Chasing in a Volatile World

We see it every time interest rates rise: people move their money from 0.01% big-bank savings accounts to online-only platforms offering 4.5% or more. This is a rational move, yet it introduces operational risk. Can you access your money if the app goes down? How fast is the wire transfer if you need a down payment for a house tomorrow? These logistical hurdles are the "hidden" risks of chasing the safest possible yield in a digital-first economy. As a result: the quest for the perfect, risk-free asset usually ends in a compromise between convenience, returns, and the psychological peace of mind that comes with a government guarantee.

The Mirage of the Zero-Volatility Trap

The Nominal Value Fallacy

The problem is that most retail savers mistake a static balance for a preserved fortune. You open your banking application and see the same digits staring back at you. This feels like safety. Psychological anchoring leads us to believe that if the number does not shrink, the risk is zero. Except that your purchasing power is a melting ice cube in a summer heatwave. Let's be clear: inflation risk is the silent thief that professional analysts fear far more than a temporary market dip. If the Consumer Price Index (CPI) climbs by 3.4 percent while your "safe" account yields 0.05 percent, you are effectively losing wealth. You are not standing still; you are sprinting backward on a treadmill. And yet, the human brain craves the dopamine hit of a stable green number. Because we are hardwired to avoid immediate loss, we ignore the slow-motion car crash of eroding value.

The Liquidity Illusion

Many investors flock to Certificates of Deposit (CDs) or structured notes thinking they have found what investment has no risk. But what happens when life throws a wrench in your gears? The issue remains one of opportunity cost and accessibility. If you lock your capital into a 5-year fixed-term vehicle and an emergency arises, the penalties often cannibalize your entire interest gain. In some cases, the "early withdrawal fee" can even bite into your principal. Is it truly risk-free if you cannot touch your own money without a haircut? Which explains why liquid assets often carry lower yields; you are paying a premium for the right to change your mind. It is a classic trade-off that many ignore until the car breaks down or the roof leaks.

The Hidden Vector: Counterparty and Sovereign Fragility

The Myth of Perpetual Solvency

We often treat government backing as a divine guarantee. We assume that a sovereign entity will always have the printing press or the tax authority to make us whole. Historically, this is a bit of a gamble, isn't it? While a U.S. Treasury bond is considered the global "risk-free rate," the 2023 banking jitters proved that even "safe" bonds can cause systemic havoc if interest rates pivot too fast. If a bank holds long-dated "risk-free" debt while depositors demand their cash today, the bank collapses. As a result: the safety is systemic, not individual. You must look beyond the instrument and peer into the plumbing of the institution holding it. Even the most fortified balance sheets have cracks. (Sometimes those cracks are just hidden by complex accounting). To believe any human institution is immortal is the height of financial irony.

Frequently Asked Questions

Is there a specific mathematical definition for a risk-free rate?

In the halls of academia and high-frequency trading firms, the 13-week T-bill is the gold standard for what investment has no risk. As of mid-2024, these yields hovered around 5.25 percent, providing a temporary sanctuary for those fleeing equity volatility. Analysts use this figure as the baseline for the Capital Asset Pricing Model (CAPM) to determine if other assets are worth the gamble. But even this math ignores the tax man, who will happily take up to 37 percent of those gains depending on your bracket. If you earn 5 percent but lose 2 percent to inflation and 1.5 percent to taxes, your real return is a measly 1.5 percent.

Do high-yield savings accounts carry any hidden dangers?

The primary danger is not the loss of principal but the reinvestment risk inherent in floating rates. Banks can slash your APY overnight without a moment's notice if the Federal Reserve decides to pivot toward a dovish stance. During the 2008-2015 era, many savers watched their yields plummet from 4 percent to near 0.1 percent in a agonizingly short window. This forces you to either accept poverty-level returns or move your money into speculative markets at exactly the wrong time. You are essentially a passenger on a ship where the captain can change the speed and direction while you are asleep in your cabin.

Can gold be considered a zero-risk investment for long-term holding?

Gold is frequently touted as the ultimate hedge, but its price action is notoriously volatile in the short term. In 2011, gold peaked near 1,900 dollars before embarking on a brutal multi-year slide that saw it drop below 1,100 dollars by 2015. That represents a nearly 40 percent drawdown, which is hardly the definition of safety for someone needing cash quickly. While it serves as a store of value over centuries, it pays no dividends and costs money to store or insure. It is a bet on chaos rather than a guarantee of growth, making it a speculative insurance policy rather than a risk-free asset.

The Verdict on Absolute Safety

Stop hunting for the financial unicorn because it does not exist in this or any other economy. Every allocation of capital involves a trade-off between the certainty of the present and the uncertainty of the future. We must accept that "risk-free" is a marketing slogan designed to soothe the anxious minds of the middle class. If you choose total stability, you are opting for the guaranteed risk of wealth stagnation. My position is firm: the only true safety is found in diversified resilience rather than a single "safe" fortress. In short, the most dangerous move you can make is trying to avoid every possible danger until your capital withers into irrelevance. Embrace the calculated leap or prepare to be buried by the cost of living.