We spend a lot of time pretending the world is a giant spreadsheet where every cell is predictable. It is a comforting lie, isn't it? But the thing is, most people treat risk like a static monster under the bed when it is actually more like the weather—constantly shifting, sometimes invisible, and occasionally capable of leveling the house. When we ask what are the types of risks, we aren't just looking for a list of bad things that might happen. We are looking for the structural weaknesses in the systems we rely on every single day. Systemic vulnerability is often hidden behind the veil of "business as usual" until a black swan event arrives to rip the curtain down. And honestly, it’s unclear why we keep acting surprised when these cycles repeat.

Beyond the Dictionary: Decoding the True Nature of Risk Environments

Defining risk requires more than a quick glance at a textbook because the context changes the definition entirely. In the boardroom, risk is a calculation of capital adequacy and market share protection. Yet, on the factory floor, that same word translates to occupational hazards and mechanical failure rates that could halt production for months. Which explains why a single definition never quite fits everyone. I believe we have become far too obsessed with the "quantifiable" side of things, ignoring the messy, qualitative human elements that actually drive most disasters. We see the math, but we miss the cognitive biases that make the math useless in a real crisis.

The Dichotomy Between Pure and Speculative Probability

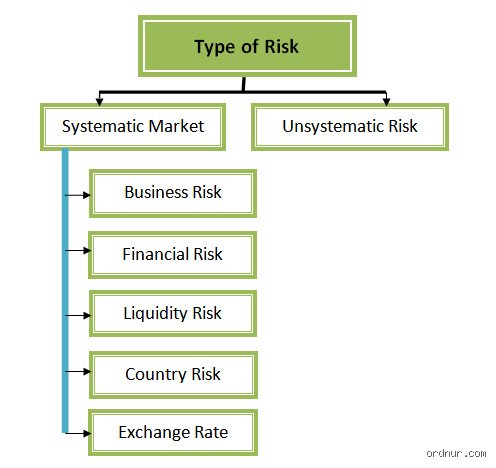

There is a sharp distinction here that people don't think about enough. Pure risks are those where the only possible outcomes are loss or no loss—think of a fire at a warehouse in Rotterdam or a data breach in a Silicon Valley startup. There is no "upside" to a fire. But then you have speculative risks, which are the lifeblood of the global economy. These involve a chance of gain or loss, such as investing in emerging market equities or launching a new software product. That changes everything. You cannot grow without embracing speculative uncertainty, but if you treat it with the same rigid fear as a pure hazard, you’ll end up stagnant. As a result: the most successful entities aren't those that avoid risk, but those that navigate the risk-reward frontier with a bit of actual courage.

Dissecting Financial Volatility and the Ghost of Market Liquidity

When most analysts discuss what are the types of risks, they lead with the money. It makes sense because money is the easiest thing to measure, even when the measurements are wrong. Financial risk is an umbrella term that covers everything from interest rate fluctuations to the terrifying possibility that your counterparty simply vanishes into thin air when the bill comes due. In 2008, the world learned a brutal lesson about credit risk and the domino effect of subprime mortgage derivatives. But have we actually moved on, or have we just moved the debt to different pockets? The issue remains that leverage is a double-edged sword that usually cuts the person holding it first.

Market Risk and the Chaos of Global Interdependence

This is the big one. Market risk—often called systematic risk—is the danger that the entire ship goes down, regardless of how well you’ve cleaned your specific cabin. It includes equity risk, currency risk, and commodity price volatility. Imagine a manufacturer in Munich that buys raw materials in USD but sells finished goods in EUR; a 10% shift in the exchange rate can wipe out an entire year’s profit margin before they’ve even opened the mail. It’s a relentless, 24-hour cycle of pressure. Is it even possible to hedge against everything? No, and trying to do so is a fool’s errand that costs more than it saves.

The Hidden Trap of Liquidity and Cash Flow Stagnation

People confuse being wealthy with having cash. You can own a billion dollars’ worth of real estate in London, but if you can’t pay your electric bill today because no one is buying office buildings, you are experiencing liquidity risk. This specific type of risk is what kills most small businesses and quite a few large ones too. It is the gap between "we are owed money" and "we have money to spend." During the 2020 global lockdowns, we saw working capital dry up in weeks, proving that cash-to-cash cycles are the true pulse of any operation. Which explains why savvy CFOs are now hoarding "dry powder" instead of reinvesting every cent into growth.

Operational Failures: When the Internal Machinery Grinds to a Halt

Now we get into the weeds of operational risk. This isn't about the stock market; it’s about the person who forgets to update the server patches or the delivery truck that breaks down on a bridge in Istanbul. It is the risk of loss resulting from inadequate or failed internal processes, people, and systems. But here is where it gets tricky—operational risk is often endogenous, meaning it’s a monster we create ourselves through technical debt or poor corporate culture. A company might have a great balance sheet, but if their internal controls are a mess, they are essentially a house of cards waiting for a stiff breeze.

Cybersecurity and the Digital Frontier of Vulnerability

In the last decade, cyber risk has moved from a "tech problem" to the top of the enterprise risk management (ERM) priority list. We are far from the days when a simple antivirus was enough. Today, we face ransomware-as-a-service and state-sponsored espionage that can paralyze a nation's critical infrastructure in minutes. The 2021 Colonial Pipeline attack serves as a grim reminder: a single compromised password can lead to gas shortages across an entire coastline. Because our world is now built on interconnected APIs and cloud dependencies, a failure in one node can trigger a cascading failure across thousands of unrelated businesses.

The Human Factor and the Reliability of Personnel

We love to blame the machines, but human error remains the primary driver of operational disasters. This includes everything from simple mistakes to occupational fraud and "rogue trader" scenarios that have famously collapsed institutions like Barings Bank. It is also about key person risk—the terrifying reality that if your lead engineer gets a better job offer or decides to retire, twenty years of institutional knowledge walks out the door with them. Do we value succession planning enough? Probably not, because it’s boring and doesn’t show up on a quarterly earnings call, yet it is a fundamental pillar of long-term survival.

Strategic Risk: The Danger of Being Right About the Wrong Things

Strategic risk is arguably the most dangerous because it involves the high-level decisions that determine the company's trajectory over five to ten years. It’s the risk of technological obsolescence—the "Kodak moment" where you are the best in the world at something that nobody wants anymore. This is not a failure of operation; it’s a failure of vision. Market entry risks and botched mergers also fall into this bucket. If you spend $44 billion on a social media platform without a clear path to monetization, you are dancing on the edge of a strategic volcano. It’s a high-stakes game where the rules change while you’re playing.

Regulatory Shifts and the Weight of Legal Compliance

Governments have a funny way of changing the locks while you’re trying to open the door. Regulatory risk is the threat that new laws or compliance mandates will suddenly make your business model illegal or prohibitively expensive. Look at the GDPR implementation in Europe or the shifting ESG (Environmental, Social, and Governance) requirements in the United States. These aren't just paperwork; they are structural hurdles that require massive shifts in resource allocation. Companies that ignore the legislative pipeline often find themselves hit with punitive fines that make their previous profits look like pocket change. Yet, some firms still treat legal risk as an afterthought—an expensive mistake (to say the very least) in a world that is increasingly litigious and transparent.

Common pitfalls and the fallacy of the checklist

The problem is that most managers treat what are the types of risks like a grocery list rather than a shifting weather pattern. You probably think that checking off a box for operational volatility means you are safe for the quarter. It is not that simple. Many organizations fall into the trap of siloed categorization, where the IT department handles cyber threats and the finance team watches the markets, but nobody notices when a server crash triggers a margin call. Let's be clear: risk is a tangled web, not a series of neat drawers. Because these categories overlap, treating them as isolated incidents is an invitation to disaster. Correlation neglect remains the silent killer of modern enterprises. If a global pandemic hits, your supply chain disruptions and liquidity shortages happen simultaneously, not in a convenient sequence. Yet, we still see boards of directors looking at static heat maps from three months ago. Is your risk registry actually a rearview mirror in disguise? This static assessment bias leads to a false sense of security that evaporates the moment a "Black Swan" event occurs. Statistics from 2024 suggest that nearly 62% of corporate crises were preceded by internal warnings that were ignored because they did not fit into a standard reporting template.

The transparency paradox

Another frequent blunder involves the obsession with quantification over qualification. We love numbers because they feel objective. However, assigning a 7.5 probability score to a reputational scandal is often just an educated guess wrapped in a fancy spreadsheet. In short, mathematical arrogance masks the messy reality of human behavior. But when you focus only on what you can measure, you become blind to the "gray rhinos" (obvious but ignored threats) charging straight at you. The issue remains that data points are historical, whereas emerging hazards are forward-looking and inherently erratic.

The hidden layer: Psychographic and Cognitive Risk

Except that we rarely talk about the internal architecture of fear within an organization. To truly understand what are the types of risks, you must look at cognitive biases like groupthink and anchoring. These are the "meta-risks" that determine how all other dangers are perceived. If your leadership team is trapped in a confirmation bias loop, no amount of sophisticated software will save the company from a bad merger. As a result: the greatest hazard is often the person sitting at the head of the conference table. (And yes, that includes you). We suggest focusing on decision-making hygiene rather than just hardware firewalls. This involves Red Teaming, where a specific group is paid to find holes in your strategy. Which explains why firms using adversarial simulation report a 40% higher resilience rate during market downturns. You cannot manage what you refuse to see, and most leaders are experts at looking away from their own fallibility. Expert advice? Stop looking for more types of risks and start looking at how your brain filters the ones you already know about. Heuristic failure is the ultimate systemic threat.

The cost of the "Safety First" myth

Ironically, being too risk-averse is a strategic peril in itself. If you avoid every speculative venture, you eventually succumb to obsolescence risk. In a world where AI integration increases productivity by an average of 34%, playing it safe is the fastest way to go bankrupt. The issue remains finding the "Goldilocks zone" of exposure where growth is possible without catastrophic failure. Strategic paralysis has claimed more companies than market fluctuations ever will.

Frequently Asked Questions

Which category of threat is most likely to cause total business failure?

While many point to financial insolvency, the data indicates that strategic risk accounts for approximately 86% of massive losses in enterprise value. This occurs when a company's fundamental business model becomes irrelevant due to technological disruption or shifting consumer preferences. It is rarely a single event but a slow erosion of competitive advantage. Unlike insurable hazards, these shifts cannot be offset by a premium. Most firms realize they are in trouble only after their market share has plummeted by 20% or more.

How often should a company update its assessment of what are the types of risks?

Annual reviews are a relic of the twentieth century and are now largely useless. Leading risk management frameworks now advocate for continuous monitoring or at least monthly tactical adjustments. The velocity of change in sectors like fintech or biotech is too high for a "set it and forget it" mentality. In fact, companies that utilize real-time data analytics for risk detection see a 25% reduction in the cost of mitigation. Waiting for the yearly board meeting to discuss geopolitical shifts is a recipe for reactive chaos.

Can all operational uncertainties be mitigated through insurance?

Absolutely not, and believing so is a dangerous misconception. Insurance covers pure risks, such as fires or physical theft, but it rarely protects against brand erosion or poor management decisions. Roughly 70% of a company's value is now tied to intangible assets like intellectual property and reputation, which are notoriously difficult to insure fully. You can buy a policy for a data breach, but you cannot buy a policy that restores customer trust once it is broken. Mitigation must be cultural and structural, not just a line item in the insurance budget.

Engaged synthesis on the future of uncertainty

Stop trying to categorize your way to safety because the universe does not respect your spreadsheets. The reality of what are the types of risks is that they are interconnected organisms that evolve faster than your compliance department can type. We must move past the infantile idea that risk is something to be "solved" or eliminated. Instead, resilience engineering must become the core competency of the modern professional. If you are not actively seeking out the fragility in your systems, you are merely waiting for the inevitable to arrive. Courage is not the absence of risk; it is the deliberate navigation of it. Accept that total certainty is a lie sold by consultants, and you will finally be ready to lead.