Understanding PAGP and Its MLP Structure

PAGP, or Plains All American Pipeline, LP, trades on NASDAQ and pays out distributions—not dividends in the traditional sense. That word choice matters. It’s not just semantics. Because PAGP is an MLP, it avoids corporate income tax by passing profits directly to unitholders. Those profits show up as distributions, which feel like dividends but are treated very differently on your tax return. This structure is common in energy infrastructure—think pipelines, storage terminals, midstream operations. It’s designed to generate steady cash flow. And pass it through. But because of that, the IRS doesn’t see these payouts as “dividends” eligible for preferential tax rates.

The entity itself isn’t taxed at the corporate level. Instead, each unitholder is allocated a share of the partnership’s income, deductions, and credits—whether or not cash is actually distributed. This is why you get a Schedule K-1 instead of a 1099-DIV. And that’s where people don’t think about this enough: you can owe taxes even if you reinvest every dollar or worse—lose money on the unit price but still get a tax bill. That happened to some investors in 2016 when energy prices collapsed. Units dropped 40%, yet K-1s still showed taxable income. Brutal.

Why PAGP Distributions Aren’t Classified as Qualified Dividends

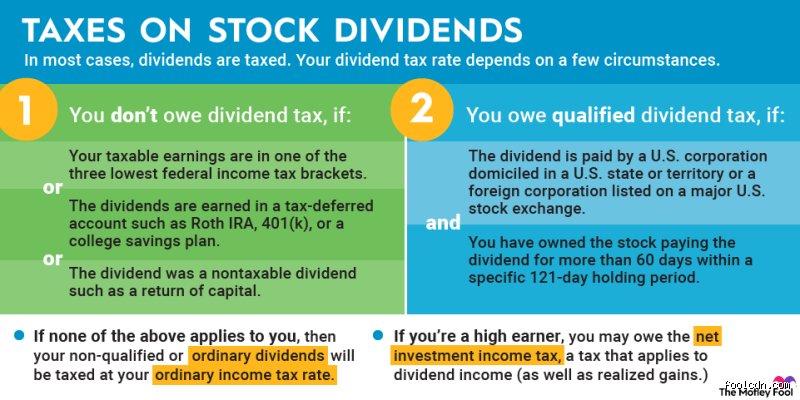

Qualified dividends—like those from Apple or JNJ—get hit with the 0%, 15%, or 20% long-term capital gains rate depending on your income bracket. PAGP? Nope. Its distributions are mostly a return of capital or ordinary income. The IRS doesn’t care how high the yield looks on your brokerage screen. What matters is the partnership’s taxable income, depreciation, and cost basis adjustments. In 2023, roughly 78% of PAGP’s distribution was classified as a return of capital, according to its final K-1 data. That means only 22% was taxable in that year—on paper. But—and that’s exactly where it gets complicated—that return of capital reduces your cost basis. So when you eventually sell, your capital gains could be much larger. Or you could hit zero basis and have ordinary income instead. Not what most retirees expect from a “dividend” stock.

The Role of Schedule K-1 in MLP Tax Reporting

You won’t find your PAGP tax details in a 1099. You’ll get a Schedule K-1, usually in March. It breaks down your share of the partnership’s income: Section 1231 gains, interest, foreign income, depletion, and more. CPAs love these forms. Said no one ever. The problem is, K-1s can arrive late, complicate state filings, and require additional calculations. If you hold PAGP in multiple states—say, you’re a Florida resident but the pipeline operates in Texas, New Mexico, and Illinois—you may owe state taxes in those jurisdictions. Even if you don’t live there. That’s right: investing in an MLP can trigger state filing requirements in up to 10 states, depending on operations. The issue remains: convenience versus yield. Is that 7% distribution worth filing in Oklahoma?

How the Tax Treatment Differs from Traditional Dividend Stocks

Let’s compare PAGP to Johnson & Johnson—two very different animals. JNJ pays a qualified dividend. You get a 1099-DIV. The IRS taxes it at your long-term gains rate. Simple. PAGP? You get a K-1. Part of the distribution is taxable now, part defers (but hits you later), and part could be tax-exempt. In 2022, about 15% of PAGP’s payout was classified as Section 754 adjustments—effectively tax-free at distribution but reducing basis. It’s a bit like getting paid in IOUs that morph into tax liability later. To give a sense of scale: if you bought 1,000 units at $15 each ($15,000 total), and over five years received $6,000 in distributions—all return of capital—your basis drops to $9,000. Sell at $18? You’re taxed on a $9,000 gain, not $3,000. Ouch.

And that’s the trap: the yield looks juicy—sometimes over 7%—but the real cost hides in basis erosion and deferred taxes. Traditional stocks don’t do this. Reinvested dividends increase your basis. MLPs do the opposite. They chip it away. Because of this, holding MLPs in taxable accounts can make sense—but only if you understand the long game. In retirement accounts? Risky. The IRS hates MLPs in IRAs. Why? Unrelated business taxable income (UBTI). If your IRA earns over $1,000 in UBTI annually, it owes taxes. Most people don’t realize this until the IRS comes knocking. So holding PAGP in an IRA might seem smart—no immediate taxes—but it could trigger a tax bill *inside* the IRA. Which explains why advisors often tell clients: keep MLPs out of retirement accounts.

Return of Capital: The Hidden Tax Mechanism

The bulk of PAGP’s distribution isn’t profit. It’s return of capital. In 2021, it was 82%. In 2023, 78%. That’s standard for stable MLPs. They generate cash from operations but deduct non-cash expenses like depreciation. So taxable income is low. The partnership passes through those deductions too. Which means you get income on paper that’s less than the cash you receive. The excess is return of capital. It’s not taxable now. But it’s not free money either. It’s a deferral. A tax time bomb, albeit a slow-moving one.

Here’s the math: say your annual distribution is $1.20 per unit. The K-1 says $0.25 is ordinary income, $0.05 is Section 1231 gain, and $0.90 is return of capital. You pay tax on $0.30. The $0.90 reduces your cost basis. Buy at $20? After one year, basis is $19.10. After five years of the same? $15.50. Sell at $22? Taxable gain is $6.50 per unit—$1.50 more than if it were a regular dividend stock. And because depreciation was taken, part of that gain could be recaptured at higher rates. The issue remains: investors chasing yield often ignore basis erosion until it’s too late. I find this overrated—the idea that high yield automatically means high return. Not when taxes eat half the gain.

PAGP vs Other Energy Stocks: Tax Efficiency Compared

Let’s stack PAGP against two peers: Enterprise Products Partners (EPD) and Energy Transfer (ET). All are MLPs. All issue K-1s. But their tax profiles differ. In 2023, EPD's return of capital was 67%, ET’s was 89%. PAGP’s 78% sits in the middle. EPD has more stable cash flows and lower leverage. ET has higher risk, more volatility, and—consequently—higher ROC. That said, all three avoid corporate tax. None pay qualified dividends. But EPD has a reputation for K-1 simplicity. PAGP? A bit more complex, with foreign partner allocations and environmental credits that flow through.

Now compare to ExxonMobil (XOM). XOM pays qualified dividends. 2023 rate: $3.88 per share. Qualified. Taxed at 15% or 20% if you’re in a high bracket. No K-1. No basis erosion. No state tax surprises. But yield? Around 3.5%. Half of PAGP’s. So you’re trading tax simplicity for income. And that’s exactly where your personal situation kicks in. Are you in a low tax bracket now but expect to be higher later? PAGP’s deferral helps. Are you in a high bracket? The ordinary income portion hurts. Do you hate filing multiple state returns? Avoid MLPs. But if you want yield and can handle complexity, PAGP makes sense. Honestly, it is unclear which is “better”—it depends on your tax geography and holding period.

Frequently Asked Questions

Do I Pay Taxes on PAGP Distributions Every Year?

Yes—but not on the full amount. Only the portion classified as ordinary income, interest, or gain. The return of capital part reduces your cost basis and isn’t taxed until you sell. But—and this catches people off guard—even if the distribution is 90% ROC, you still report it. And if your basis hits zero, future ROC becomes taxable immediately. So deferral isn’t permanent. It’s a delay. Data from 2015–2020 shows average annual taxable income from PAGP was $0.28 per unit, while distributions averaged $1.15. That’s 75% deferral. Not bad. But don’t assume it lasts forever.

Can I Hold PAGP in an IRA?

You can—but you shouldn’t. MLPs generate UBTI. IRA custodians don’t like it. If UBTI exceeds $1,000 per year across all MLP holdings, the IRA must file Form 990-T and pay taxes. Most investors don’t know this. They think tax-deferred means no tax ever. Wrong. The IRS still wants its cut. Some custodians block MLPs entirely. Others allow them but charge fees for 990-T filings. So while possible, it’s often more trouble than it’s worth. Use taxable accounts instead. Or invest in MLP ETFs like AMLP, which avoid UBTI by being C-corps. But—trade-off—they don’t pass through tax benefits either.

How Does the 754 Adjustment Affect My Taxes?

The Section 754 election allows the partnership to adjust your basis in the units when you sell or inherit. It’s meant to prevent double taxation. In practice, it often results in a small tax-free portion of the distribution. In 2022, PAGP’s 754 adjustment was about $0.07 per unit—effectively reducing taxable income. But it’s not a deduction. It’s a reallocation. And it only matters if the partnership makes the election (PAGP does). Most unitholders never touch this line item. But it’s there, quietly shaping your tax outcome.

The Bottom Line

PAGP dividends—distributions, really—are taxed as a mix of ordinary income, return of capital, and occasional gains. They don’t get preferential rates. They come with K-1s, basis tracking, and potential state tax landmines. But they also offer high yield and tax deferral. For the disciplined investor in a taxable account, that changes everything. For the retiree who hates tax paperwork? We’re far from it. The real question isn’t how they’re taxed—it’s whether the after-tax return justifies the hassle. In my view, PAGP makes sense only if you’re prepared for the long haul, understand basis erosion, and don’t mind March surprises from Texas. Because the yield looks great on paper. But taxes? They’re the silent co-investor. And they always get paid. Suffice to say, know what you own.